Hey, concorde current pe ratio is 90 and peg is around 0.87, is it still worth holding in this valuation, if company grow earrings by 40% as guided

1 Like

Read last concall, projections are 5x in 2-3 years , base fy25

link is broken, it doesn’t go to the pdf

So current valuation is justified according to you if management continue to achieve all it’s guided numbers??

Do the projections with 24-25% ebitda as kavach will have higher margins as its indigeniously made. Give PE multiple as to what EMS sector small cap companies are commanding like Aimtron and more conservatively keep PEG < 1.

There is no doubt that valuations look stretched. At the same time, it’s worth noting that markets have punished overvalued stories in the last few months. However, Concord has remained relatively resilient.

In my personal view, it’s a combination of the following factors:

- Management has guided for base level 40% to 50% growth. However, 5x in 24 to 36 months (from FY25) looks achievable. The high-growth trajectory is one factor.

- Markets look for management that delivers on the guidance. Concord has a history of beating the guidance. They under promise and over deliver. Given the track record, there is a valuation premium. Further, 5x in 24 to 36 months might also be a conservative number.

- Concord has several growth triggers. DPWCS is already playing out and big order inflow will continue over the next 12 to 24 months. Kavach is on the horizon and will have a multiplier impact on the order book. Fusion Electronics is in the building stage and considering the focus of the government on the PCB segment, it’s likely to be a value creator.

Overall, I would not be surprised if Concord corrects from current levels. However, if order inflow remains robust and growth exceeds expectations, the valuation premium can sustain and continue to surprise investors.

2 Likes

Yes you are right, so if this valuation remains same overvalued and company continue to give 40% earning growth then will share price can go up ?

or due to valuation its hard to gain returns even if company gives good earning growth?

Whats your view?

Most money is made by PE rerating + PAT growth. For a company at 87x TTM PE, not much headroom for PE rerating. But one can still make money from such investments if the growth continues. If company grows bottom line at 50% and PE remains same, you make 50% CAGR on your investment. If company grows bottom line at 50% but PE derates to 40. You don’t make any money in near term but still make money in long term. Instead of asking can I make return at current valuations, you should be asking if current valuations are sustainable or not. Factor in the case in your thesis where growth doesn’t come and PE derates. It’s all probability and no one is certain of the growth. If the management was 100% sure of 50% growth for next couple of years, they would be buying their own stocks everyday from the market. I would personally take debt and buy shares if I was 100% certain. So it’s sane to not take guidance on face value and build your own thesis around future growth, current valuations, potential upside and downside protection.

Disclaimer: Not Invested & Haven’t studied the business. Just my 2 cents on valuations.

9 Likes

That’s right, but i always has question in my mind why HNI’s and pms are investing in this high levels, and they already have stake in company but still they are again participating in Preferential allotment and investing heavily in this high valuation, they can’t see this overvaluation? Yes they can see still they are investing good amount, what’s the reason? What they are seeing beyond the valuations?

The answer lies in expectation of returns & investment horizon. Not everyone invests to make 50% CAGR returns in 2 years. Some are satisfied with even 15% CAGR returns over 5 years in base case as long as capital is protected.

At current valuation of 88 PE, if a PMS wants to make 15% CAGR return for the next 5 years with an exit PE of 40. The earnings need to grow at ~34% CAGR for next 5 years. Which is lower than even the lower end guidance of the promoters. Maybe the PMS are confident that they can achieve Average of 34% CAGR growth for next 5 years.

Another point to check is allocation, do you know the % allocation of HNI’s and PMS in Concord? Maybe for them it is just 1% of the portfolio and even if it corrects by 50% it won’t put a dent on their portfolio.

3 Likes

As a good example, you can look at PTC Industries and the valuation it has commanded in the last five years.

Of course, there will be other examples where a stock has traded at premium valuations and there has been a significant downgrade.

For Concord, my personal view is that the premium exists for multiple strong reasons.

1 Like

Quite right but with kavach orders and strict execution timelines of kavach order(most are 12-18 months max), i am expecting it to grow with 70-80% CAGR in next 2-3 years both for Sales and PAT.

MY EXPECTATIONS considering total orderbook + Kavach deadlines + bidding pipelines.

200-210 cr sale FY26

340-350 cr sale FY27

580-590 cr sale FY28

Bottom line will expand more as of operating leverage + their kavach is more indegenized as management claims and more cheaper so more margins in it.

That is why i am holding at premium valuations. Lets see how new big order comes and execution goes.

2 Likes

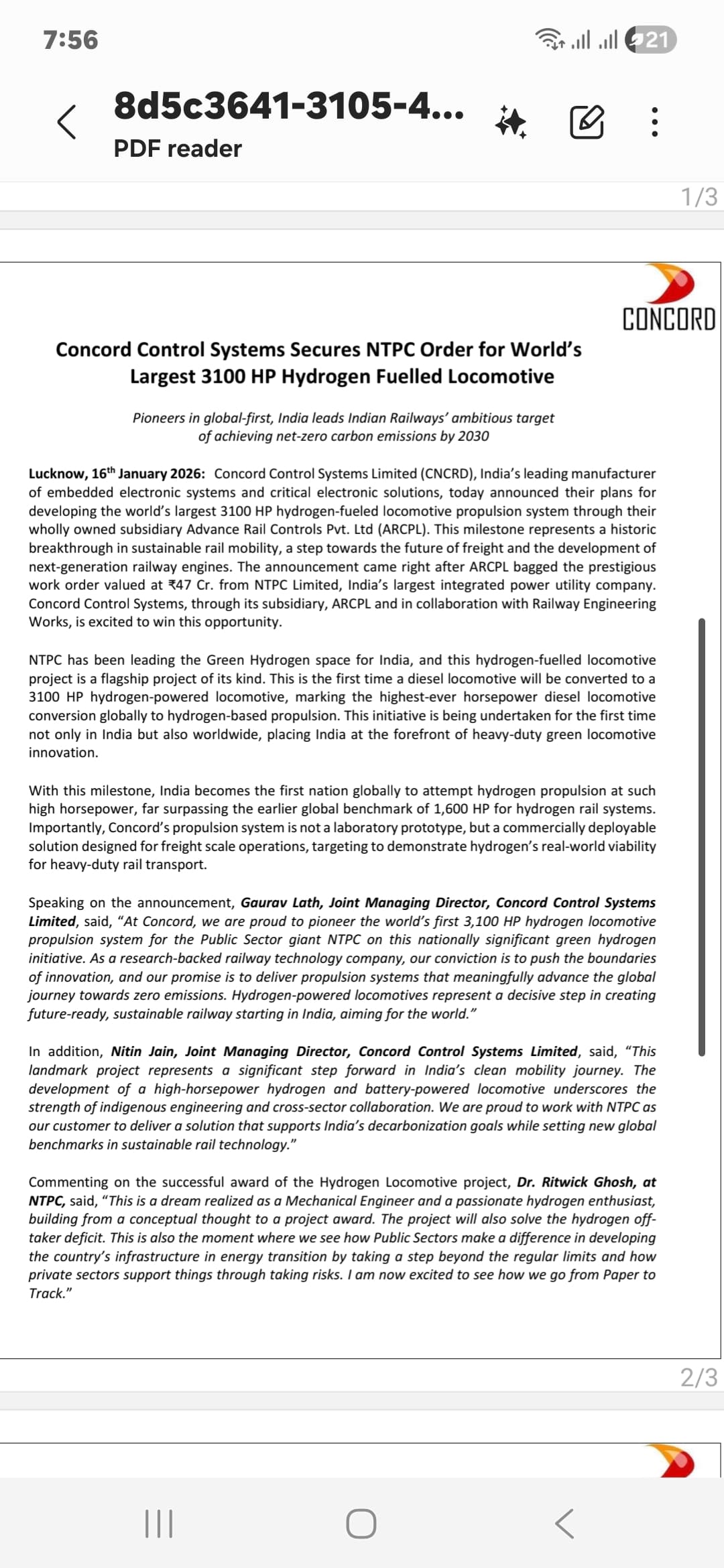

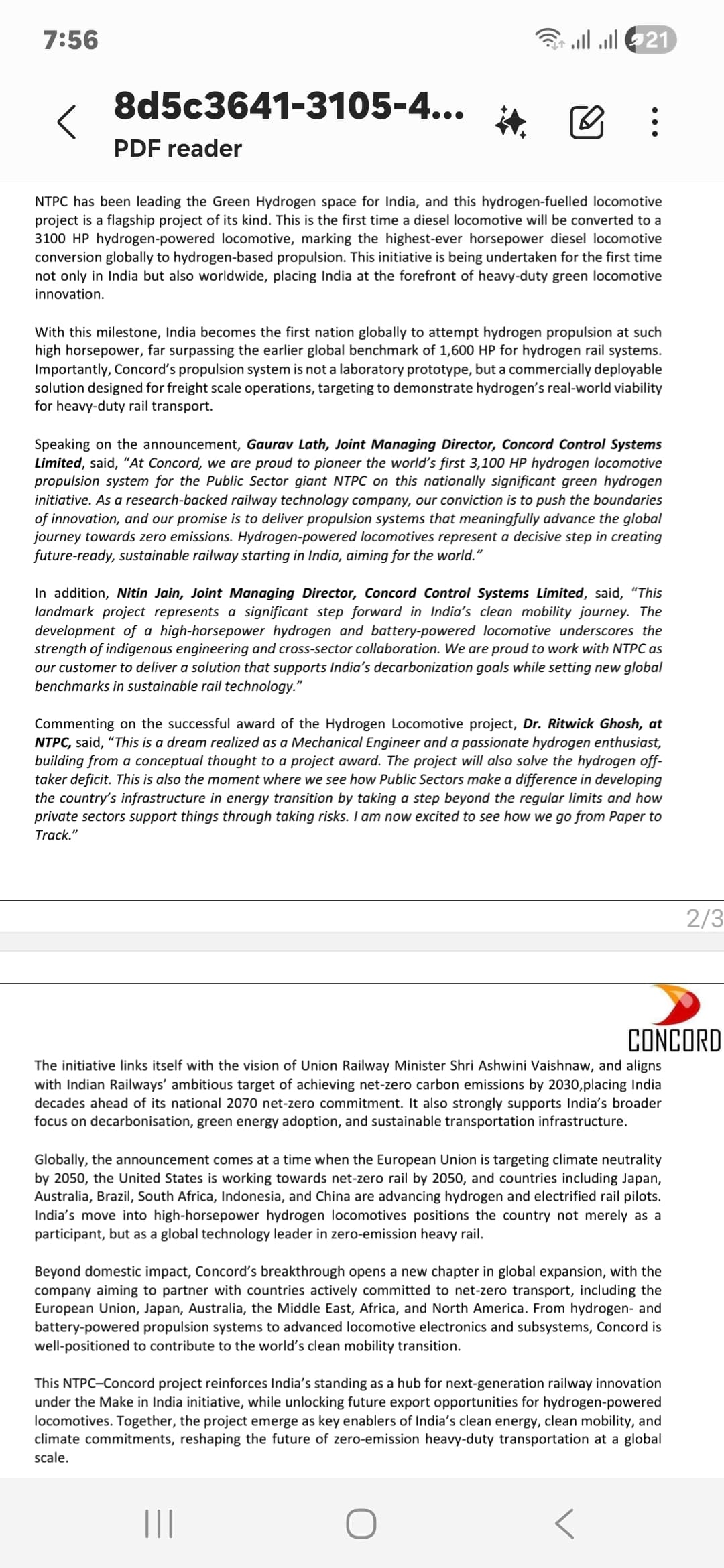

Great Insight, concord made india’s first zero emission locomotive engine, so do you have any guess or idea or forecast when Indian Railways can give order to Concord to manufacture zero emission locomotive in bulk?

Does railway really need that type of perticular locomotive which is made by Concord?

They made india’s first zero emission propulsion locomotive it’s really big innovation, but still they’re not getting bulk order from government

Can u throw some light on it?

1 Like

Check out 16 and 17th page of H1 result concall. In reply to Mr Anurag, Promoter Gaurav lath has given answer.

I have asked this question also in a later concall, there in Gaurav said Export could be a bigger opportunity in this segment. He categorically said concord fy26 growth is by DPWCS then fy27 it would be by Kavach and Fy28 they are expecting big execution in diesel to battery tech as they developed for locomotives. Even with hydrogen they are developing a tech.

Does Concord’s acquired company Fusion Electronics will also get benefit from ECMS push??? Fusion is in niche railway EMS , flex pcb and box building only for railway

3 Likes

One big order received

Concord.pdf (629.5 KB)

Fusion was not in railways EMS. fusion was in auto ems. It got closed and now Concord acquired it and will use its facility for backward integration as they have lot of electronic works related to railways, be DPWCS , Kavach, etc.

1 Like