Thats a typical reply. Personal aspiration. Would have been better if he would have upfront taken the question instead of rounding it off.

Well recent triggers are Kavach orders. So i am waiting for that as thats biggest opportunity for now. Diesel to Electric is 2-3 years far. Exports very far. So next year growth trigger is big execution of Kavach orders. So now wait is to see how it goes as railways will declare 9000 cr kavach tenders in coming 2 month time. Need see how much Progota gets. If 300-400 crore of orders they get then thesis is very much on. Hoping so. Invested and waiting.

1 Like

Just wanted understand, from where do you get this Rs. 9000 crores of kavach tenders information from

I have seen the 3 tenders current floating as kavach theme based investors shared on public platforms like Twitter, whatsapp groups. The total is around 9200 cr

So far a well deserved 10% knock off in the stock due to negative sentiment created by the promoter sell off. The market cap loss is much more than the 30cr worth shares sell off. When the broader markets are weak, the timing of sell off could get worse.

Can someone please tell how much Concord has paid to acquire 46% stake in Progota? I am unable to find credible sources for this information.

Non credible sources say that:

- In 2023 Concord acquired 26% stake in Progota for Rs 4.5 Cr Link

- In 2025 Concord acquired a further 20% stake (bringing the total to 46%) for Rs 12 Cr. Link

There is NO company announcement or credible source which can confirm these numbers. So please don’t assume them to be true.

But if they are indeed true, then it makes me wonder why a company which is aiming for a slice of the KAVACH pie, which is humongous, willing to let go off a significant stake (46% currently and potential a majority stake in the near future) at such a crucial juncture when the KAVACH orders are about to take off?

I understand that a small company like Progota (FY23 topline of Rs 8 lakh and FY24 topline of Rs 24 lakh) would need a lot of capital for targeting KAVACH v4.0 approval and also to setup infra for manufacturing. But still letting go off 46% stake is quite unbelievable. This means that the promoters of Progota are not able to command a high valuation, which they should be able to given the large KAVACH opportunity. Something is not adding up here.

1 Like

Progota is company owned by the Nitin Jain and Gaurav Lath himself, so they are just acquiring it and still they will have 54% ownership.. Small/Micro caps always has such issue of related party transaction..

2 Likes

7.73% in progota has been acquired at 5.17 cr through share swap. alloted to Mr. Krishan Kumar Agarwal

1 Like

You mean to say that shares of Concord were allocated to Mr Krishan Kumar in exchange of 7.73% in Progota?

Yes and also big loan Concord has given to Progota earlier so they command full control over progota.

1 Like

Copy paste done by company to all. Promoter sell was bulk deal so may be 2 buyers. So how liquidity increases from that. This cover up will not help company.

Any idea when the current kavach tenders results will be out ?

1 Like

Yes, bcz all have been asking the same question I guess??

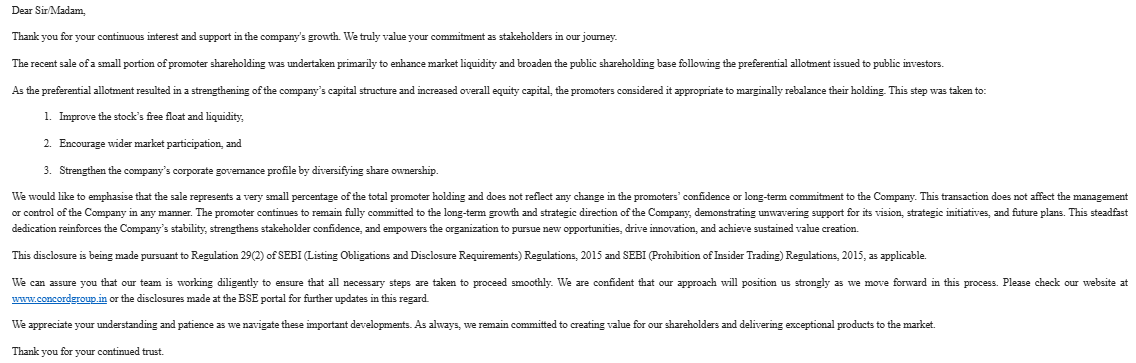

I mentioned before and I would say again that the stake sale is entirely a personal decision. All they need to do is provide a proper disclosure to the exchange (which they did). They are not liable to answer that question. I am surprised that they are kind enough to reply.

I am not backing the promoters. It’s just a simple thing. They are not bound to answer personal decisions.

On Kavach, I believe that the order wins will come within the next 30 to 45 days. If you consider the market sentiment, all stocks are bleeding. I am not worried with the current correction. And the stake sale will not impact long term sentiments if the business development remains positive. It’s worth reminding investors that promoters still hold well in excess of 60% of the business.

1 Like

Agree, absolutely a personal decision. But timing is wrong as per my understanding. Secondly the email reply given by company mentions to provide liquidity, again this is wrong, it was bulk deal, 2 buyers 2 sellers so where is the issue of increasing liquidity.

Better would have been to simply say personal decision that is all. Such wrong clarification of liquidity was not required.

Though i consider this action and reaction as negative I am still holding all and waiting for Kavach tenders decision and then will take a call. Kavach is very big opportunity. If Progota gets 400-500cr orders to be fulfilled in 12-18 months that would be quite big considering the current base

I don’t see anything wrong in their email communication. It was a cumulative statement to say preferential allotment and promoter sale would improve the liquidity.

Sameer ji, how cumulatively preferential allotment and promoter selling will increase liquidity ?

Preferential allotments are made to 3 persons and promoter selling as of bulk deal to 2 persons. So total 5 new person added as shareholders and for sure they would not sell these shares for 10-15% gain. So these shares will not come to table of buy and sell any sooner so liquidity will not change practically.

Yes theoretically we can say more number of shares as of preferential and more shares away from promoters to public will increase liquidity but practical scenario is not that as i previously mentioned.

I was reading this article today, I hope this is a positive news for railway stocks?

1 Like

Yes railway budget is expected to increase by 10% and major portion goes to rolling stock n safety

1 Like