Hi all.

Company Overview:

Concord Control System (Screener Link: Concord Control Systems Ltd share price | About Concord Control | Key Insights - Screener ) is an electrical machinery manufacturer, which includes clientele like Indian Railway, Larsen & Toubro, Tata Projects, Sterling and Wilson among others.

Their product range includes Vehicular Coupler, Emergency Lighting System, Brushless DC carriage fan, Exhaust fans, Cable Jackets, Bellows etc. and products required in electrification of coaches and Broad-Gauge network of Indian Railways like: Battery Charger 200 AH, Battery Charger 40 AH, Tensile Testing

Machine. They are approved vendor by Research Design and Standards Organisation (“RDSO”) to

manufacture and supply these products for the Indian Railways.

They are currently developing several new products and are in process of developing product prototype of Control and Relay Panels and has received Capacity cum Capability Assessment certificate for the same from RDSO.

The company recently acquired Advanced Rail Controls Private Limited (ARC) which has been working in various niche areas of rolling stock technology. The company focuses on developing high end embedded control solutions for rail domain and is peerless in its spectrum of working.

Currently the company has two manufacturing units situated at Lucknow, Uttar Pradesh with total size measuring to over 1880 sq. mtrs with a well-equipped laboratory & modern technology along with R&D units.

Financials:

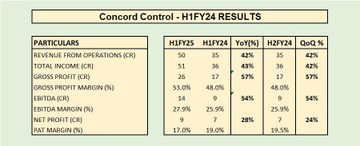

The total revenue of the company stands at 6660 Cr in FY 24 compared to 4960 Cr in FY 23 while the profit stands at 1304 Cr in 2024 compared to 544 Cr in 2023.

The company has been growing at an astounding TTM CAGR of 139% and 79% over 5 years and a 5 year ROE of 48%. Their OPM stands at a very decent 26%

Market Cap is 640 Cr with a PE of 49 and BV of 77. CMP stands at 1071.

Strengths: - Key Trigger

The company started its operations in the year

2011 when we got approval to manufacture and

supply battery charger in traction system of railway

electrification. Your company further expanded its

business in manufacturing products fitted in

coaches of Indian Railways in the year 2013 and got

approved for Emergency Light Unit which is one of

the most critical items of rolling stock application in

coaches of Indian Railways for passenger safety.

Emergency Light Unit switches on automatically in

case of power failure or in case of accidents.

Thereafter in the year 2014 we successfully

received RDSO approval for manufacturing and

supply of Tensile Load Testing Machine for Porcelain

& Composite Insulators before installation electrical

lines. Eventually our company got approval to

Supply Brushless Dc Carriage Fans to Indian railways

when it changed its technology of fans from normal

DC to Brushless DC

The above excerpt from the company AR demonstrates its ambition and ability to handle more responsibilities while expanding in a financially adept way.

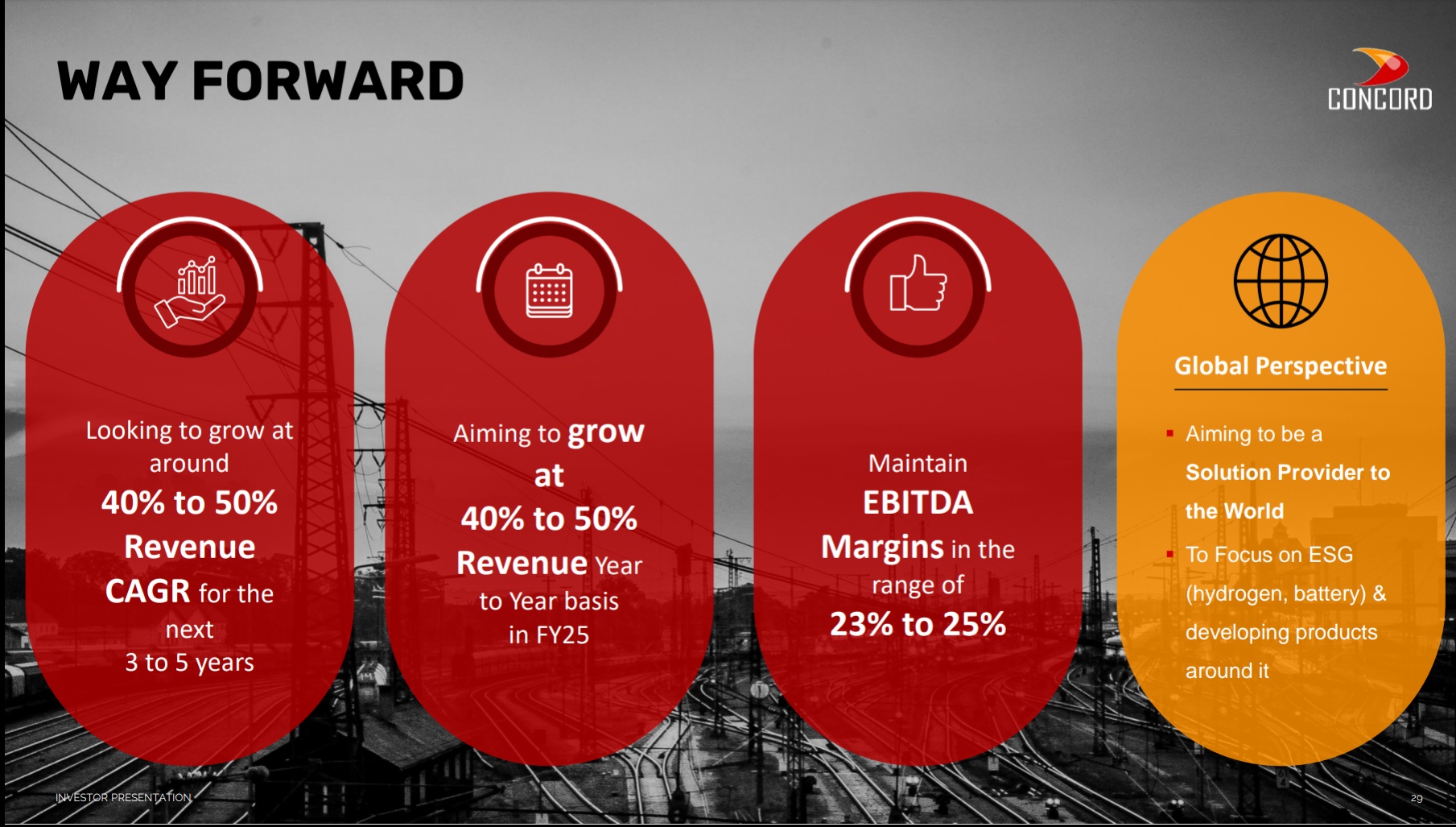

This coupled with Govt led PLI schemes for indigenous mechanical parts is another key growth driver for CCS.

The company also harbors ambition to breach the export market and secure further lucrative contracts.

The company is headed by Nitin Jain and Gaurav Lath. While Nithin Jain comes from a mechanical engineering background, Gaurav Lath has an entrepreneurial streak, engaged in few other companies as well.

Both hold 35% each of the equity in the company which signals healthy skin in the game and one of the promoters has recently purchased more shares in the company as well, which all signals a positive outlook for me.

The company has a high moat with regulation led barrier of entry.

Risks:

My main concern with this company is there not being much information being available online. (no concalls)

EDIT: While this quite a concern, i’m still comfortable to invest into this counter keeping in mind that the company deals with established players like IR, L&T, Tata etc. The fact that the company has been operational since 2011 and hold their ties signals a decently seasoned enterprise in my eyes.

The company is purely a railway based play with 100% concentration, so whenever the railways story comes to an end so will the green patch for this company.

As IR is its main client, any negative change in order book size would also negatively affect the company.

From their Annual Report:

Competitive forces could prevent the Company from achieving its

goal on account of declining revenues or margins.

Mitigation: The Company focuses on superior quality

service and affordability. The Company knows its

competitors and its customers and with differentiated

services and marketing strategies mitigates this risk

to a greater extent.

Disc: Invested, biased. Might add more on correction.