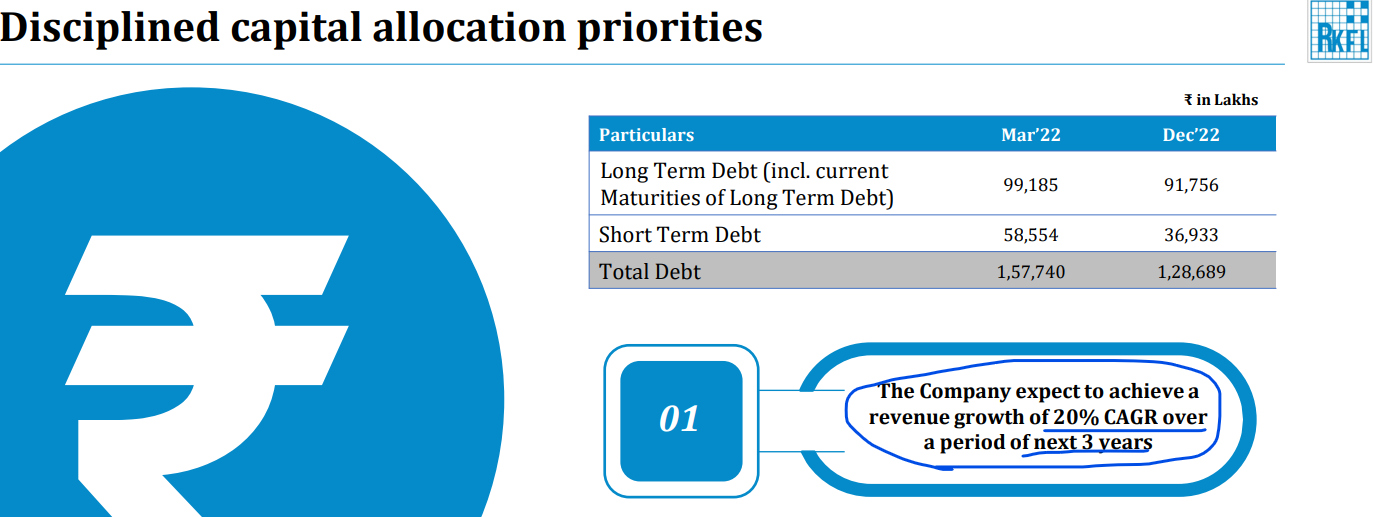

Steelcast: The company aims to reach at least Rs. 1,000 crores of sales over the next four to five years.

Right now company is doing 400 odd crores

Steelcast: The company aims to reach at least Rs. 1,000 crores of sales over the next four to five years.

Right now company is doing 400 odd crores

Poly Medicure

Reference in the below thread thanks to @Mohit_Jariwala

Carysil

Target of 1000 Crore revenue by FY25

Current revenue ~600 Crore

EBIDTA margins of 20%

Reference: Thanks to @modiankush

No point in giving such guidance if they could not predict current year growth no’s . Said something in Q1Fy24 and reduced the guidance by 20% for full year in Q2Fy24 ……

Business is not linear … So stay cautious while u get such guidance

What you said is true. They had to cut the revenues guidance sharply as their biggest customer (Bloom Enegy) is transitioning new variant of FC assembly). I still believe that they can achieve 30% CAGR revenue growth over FY23-28.

It’s a negative sign that they’ve cut down the guidance. But in past years (atleast twice), they have revised their guidance upwards and achieved it (In FY23, they commited to 45-50 % growth , later revised it to 80% and achieved it). So, the management has not always disappoint on the guidance, but they’ve over performed.

But only in future we’ll know whether they can walk the talk or not (Revenue target of 3000cr in FY28). It’s difficult to predict what will happen in future, but I believe that their guidance is supported by some facts and discussions with existing and prospective customers. Anyways, since the co is trading at higher valuation, I plan to manage my risk by position sizing. I am okay to go wrong on some positions as I will reduce my risk via diversification.

Thanks you

Praveen

It is available in their presentations and also the annual report

which variant of FC is it ?

can you offer a link to this information ?

You can check Q2 FY 24 Concall

Synergy Green

The management expects to generate a revenue/EBITDA of INR360cr/INR43cr in FY24 and

INR450cr/INR60cr in FY25. It plans to raise capacity to 100,000t by FY27, which would have the revenue potential of INR1,400–1,500cr at peak utilization levels.

Sansera Engineering and MM Forgings are small cap companies that might grow at 20-25% CAGR for the next 3-4 years

Any guidance by companies by themselves ? Would you please give the reference to the guidance ? MM Forging is going sideways for such a long time.

Should we have data which guides us on How management committed to achieving what they guide? Many management gives guidance on super high growth but not achieve it and keeps changing goal post by giving non relevant excuses.

Let’s have list of companies whose management achieved what they committed

That is my goal too. We can remove the companies from the initial list who has provided guidance, but didn’t achieve it. Since we have the list from Q1/Q2 guidance, we will have to wait for some time to see if management is doing walk the talk or not.

We can start adding companies who achieved what they committed.

Yes sure

Thanks praveen

Went through Q2 FY 24 Concall.

Page 10,13,16

I could find new variant, which is simply a higher capacity model.

I could find eletrolyser as being a new product but that is different from FC.

I think Earlier i misread your note as “new variant of technology”

So basically MTAR is a contract manufacturer …yes ?

Concall transcript.

6fa2fc84-f88c-4b43-a167-b19918f9faee.pdf (3.4 MB)

D.not invested.

Well, they don’t exactly call themselves contract manufacturers. Buy yes they are. They develop the design with their customers and try to make it cheaper and efficient with time.

And they refer to Bloom energy as partner not as customer

Thanks

Praveen

Ramkrishna Forging in its investor presentation guiding for 20% growth for next 3 years. In the same presentation, they referring to their capacities being able to fetch the revenue of ~ 5,000 Cr. FY24 revenue seems to reach between 3,800-3,900 Cr.

Radiant guiding for 20+ CAGR growth in the coming years. Their DBJ (Diamond, Bullion & Jewelry) vertical expected to show results from this qtr3 while the recent acquisition of Acemoney puts it in a different league and expected to contribute from FY25.

If what management says, then its forward PE based upon FY24 is just ~10 which is v cheap in real estate sector

My summary below

FY24:

FY25:

Beyond FY25:

Additional Factors:

Overall:

Ajmera Realty & Infra India is confident in its ability to achieve significant revenue growth in the coming years. The combination of strong existing projects, new launches, efficient execution, and favorable market conditions positions the company well to capitalize on opportunities and deliver value to its stakeholders.