The management has provided a very bullish view on the growth targets.

The overall tone of the concall was extremely positive

Guidance:-

Target of 1000 Crore revenue by FY25

EBIDTA margins of 20%

Positives

-

Increasing SOM in International/Domestic geographies

-

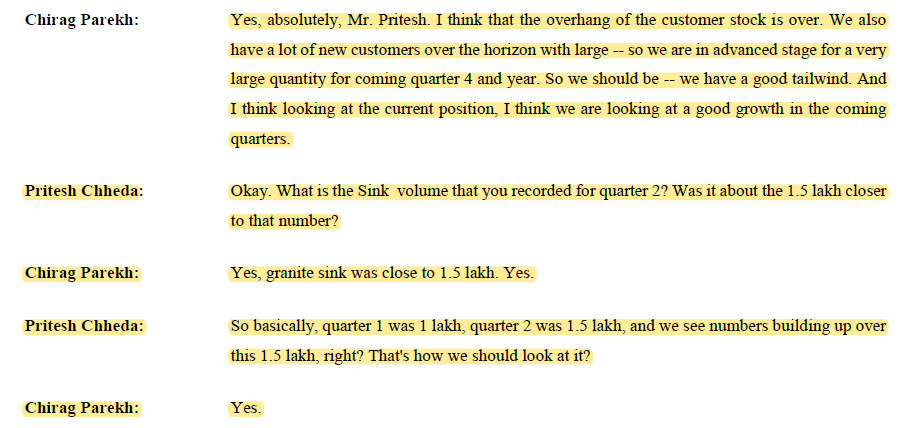

Destocking issues over with rising volumes

-

Strong Order Book for Q3 and Q4

-

Upbeat on Domestic Market w/ strong Dealer N/w

-

Strong FY23 guidance w/ performance in H2

Negatives

-

Geopolitical and Macro issues continue to be a risk

-

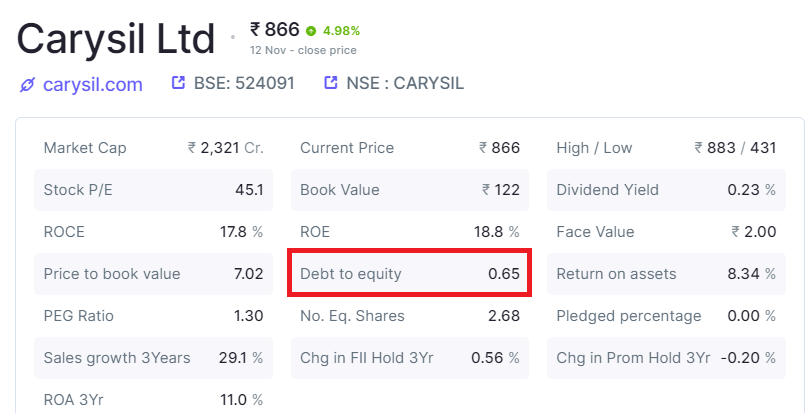

Rising Debt due to multiple acquisitions

Summary

- The management is extremely bullish on the growth propspects

- One of the few cos. to acknowledge destocking issues are over

- Better cost management gives it and edge over the competitors in EU

- Valuations a tad expensive but can be justified with expected growth in next 2 years with increasing SoM and Operating Leverage

- Rising debt is something to keep a watch on. US acquisition will reflect in B/S only from Q3.

Disc: Invested and holding