Adding to that even for,

Asian paints , the 2016 and 2017 YOY Sales growth was around 5% & 6% respectively.

Nestle indian - 2013,24,15 sales was 6 & 8 and -17.

Adding to that even for,

Asian paints , the 2016 and 2017 YOY Sales growth was around 5% & 6% respectively.

Nestle indian - 2013,24,15 sales was 6 & 8 and -17.

As mentioned, it’s average of last 7 years not YoY

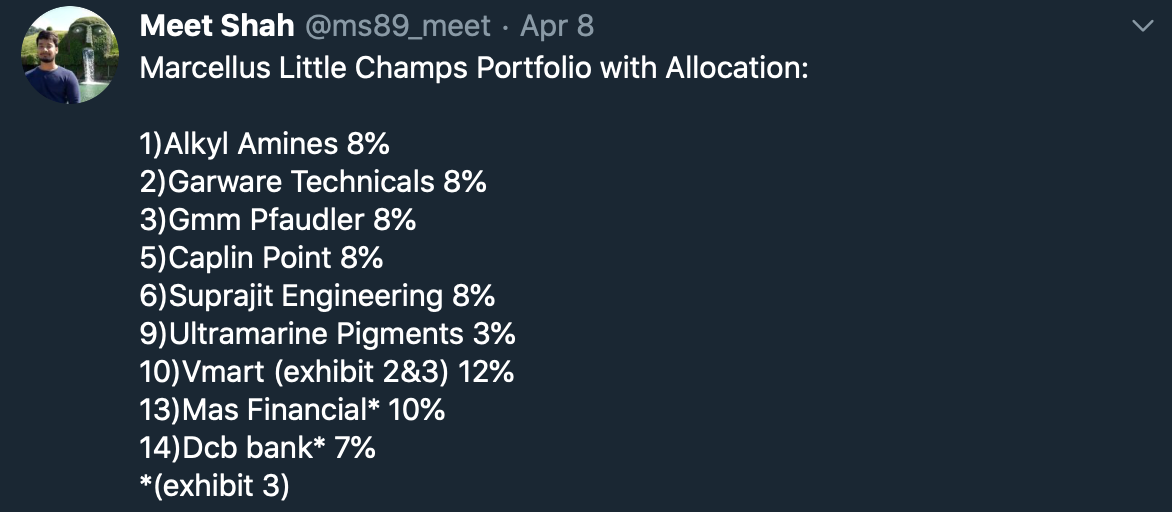

Any idea what stocks comprises Little champs portfolio ?

From what I could compile-

Alkyl amin

Garware technicals

Gmm pfaudler

Amrutanjan health care

Caplin point

Suprajit engineering

Mm forging

Ultramarine pigment

Vmart

Mas financial

Dcb bank

Cera

Folks, i’m a big fan of the-coffee-can-portfolio.pdf (487.5 KB) , i dont prefer to look daily at the charts and so on.

Do not forget to watch the below interviews its really good info there.

Also as Carl Icahn states

“ The real money that I made over the years is holding companies for 7, 8, 9 years and keeping them …… You got to buy them when nobody wants them really …. That’s the real secret …. It sounds very simple but it is very hard to do … when everybody hates it, you buy them … and then when everybody wants it, you sell it to them … And that’s what we do ”

The point seems appealing, but when we see in Indian context, where are huge corporate governance issues, it’s difficult to judge if the market is rejecting those companies because of this and something which market knows and we are missing. companies in India have lot of these problems and get wiped out in no times and no of companies are increasing at a fast pace.

Having said above, have you really identified some companies or sectors which you feel can pass this criteria?

Check the below for more details

I did some small comparisons, Caplin point and DCB looks quiet good in the current valuations.

The above are personal opinions and not stock recommendations. Not SEBI registered advisor.

Check the below stocks to start with

Portfolio 1:

3M india, CRISIL, HDFC Bank, ITC, Johnson Hitachi Controls, Nestle, P & G Hygeine, Pidelite, United Spirits.

Portfolio 2;

HDFC Bank, Kothak Bank, Bajaj Finance, P & G Hygeine, United Spirits, Kajaria, Coal India, Oberoi Reality, ITC, VST industries.

All this stocks has its own might, just do your own research.

I am sure that I will get a lot of flak for this post, so please take it with a pinch of salt ![]()

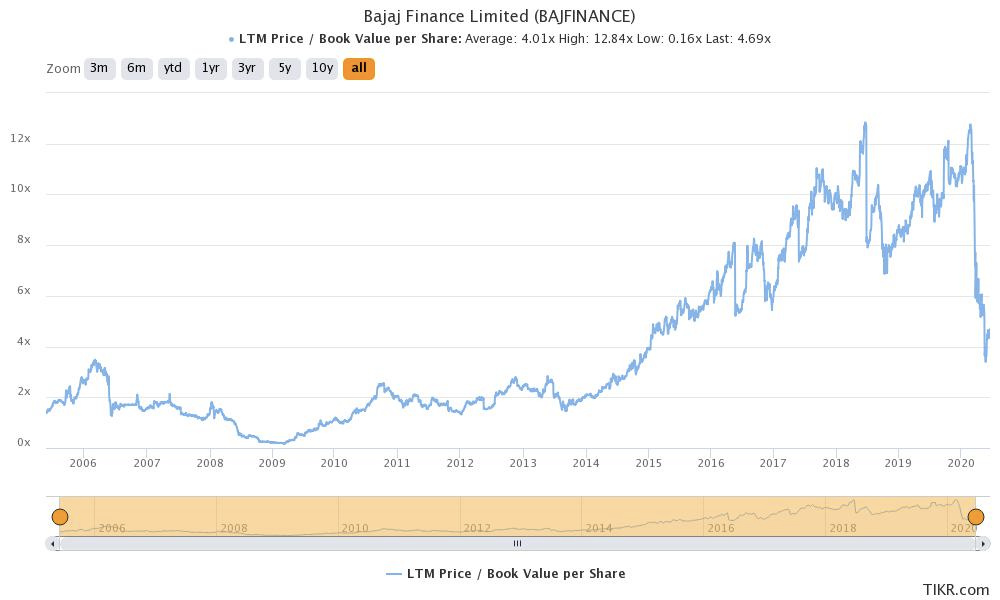

This guy thinks that lenders like Bajaj finance which have proven to be the market leader deserves a premium pricing compared to its historical P/B i.e. they should trade at a premium to their previous high of 12 times P/B. Why? Because they will be the last man standing. Lets see how this works out.

Their current P/B of 4.7x is already at a large premium to HDFC bank (which has been resilient through the last 3 economic cycles and growing their books at 18-20%).

I think HDFC Bank and Bajaj Finance are two polar opposites that can’t exist simultaneously in any serious investor’s portfolio. Premium for HDFC Bank comes from its conservative loan book as well as resilience it has shown in tough economic conditions. While Bajaj Finance gets its valuation premium because of its growth which comes from its business model of unsecured loans. Now, in the times like these, Bajaj Finance should not get any valuation premium as it has inherent weakness in business model while valuation premium for conservative lenders should go up because of their conservative approach. I think market will sure re-rate both companies(as well as similar ones) once the effects of moratorium are known. I personally think coffee can approach to investing is a sham where your whole capital can get wiped out if you don’t track your investments regularly. For every successful coffee can investor you get from west, you can meet hundreds of Indian investors who invested in “buy it, shut it, forget it” companies and had their whole VRS wiped out. While one can set parameters for coffee can investing, even Marcellus guys have to monitor their portfolio which goes against the basic idea of “Coffee can” method.

My 2 cents on this.

Pramod Gubbi said that Bajaj Finance may get higher valuation after some quarters when demand is picking up again as completion will be less when compared to pre-covid levels.

IMO, this is pretty much possible in a medium to long term. As after each crisis surviver is much stronger and prudent.

Exactly. The Marcellus view-point is that:

HDFC Bank and Bajaj Finance cater to different segments. HDFC Bank will be the #1 Banking player. Bajaj Finance will be the #1 in NBFCs

Per Coffee Can method, Bajaj Finance is a 5-10X bagger from here. We will probably see them at 15000-20000 INR in 10 years. Calculating backwards, it is a fair value today at 2600. Smart money already knows about this and that is why you see the big uptick in Bajaj Finance. Dumb money was expecting Bajaj Finance to go to 3 digits. If it were to go to 3 digits, I would buy for it to become 25% of my portfolio vs. the 5% that it is now.

Somehow, I am not able to sleep peacefully if I buy high and therefore from a ‘peaceful investing’ standpoint, look to add positions in Coffee Can stocks when they fall

Disclosure: 100 stocks held at 1900 INR each

I am very bullish on credit business in India. When we compare our country with other deveopled counties, India still has many years of a good credit growth. Thats why big mnc like amazon, apple are setting up credit business in India.

For example Bajaj Finance at present only has 3% market share in over credit of country. The efficiency (especially technology and cross selling) with which bajaj is going forward, this percentage is definitely going to increase. Most probably psu banks and over leverage nbfc are going to loose their pie.

In some respect (not overall) i find nbfc a better business than banks.

Rbi don’t interfere much about promoter holding. Nbfc can still cater some neglected categories of peoples whom bank thinks more risky.

For example bajaj has created special products for CA and doctors. In coming time we may see some health financing products.

Banks and nfbc are a leverage business, so during bad economic they always take a hit. So IMO It can be treated a good time to add in portfolio.

Disclaimer:My holdings in finance (as per weightage)-

PayPal (employee benefit)

Bajaj Finance

Sbi cards

Hdfc amc

Hdfc bank

Kotak bank

Hdfc life is in watchlist, but non invested.

Definitely.

NBFCs give low-ticket loans compared to banks. Even HDFC Bank lost money lending to Reliance Capital. Banks like IDFC First want to become retail focused banks

PSU banks lost lot of money lending to shady promoters. Most likely political pressure and corruption made them lend to these promoters. They make the common man run pillar to pillar for a housing loan and waste all the bank’s funds on useless promoters.

for a NBFC like Bajaj Finance that lends to many consumers, to lose 1000 crore, many bets of Bajaj Finance have to be bad. For a bank, one loan of 1000 crore going bad is enough. I like NBFCs that are well run like Bajaj Finance.

Great NBFCs like Bajaj Finance will grow even bigger and we are looking at 15k-20k at a minimum in Bajaj Finance in 10 years. The P/E that the market is willing to give to Bajaj Finance reflects this. If it is going to be 20K in 10 years, even 4K today is a good price to buy it at - as long as you are the type that can sleep when it goes to 2K and comes up again to 4K

Disc: Invested and will add more if Bajaj Finance falls below 2000. That is purely because I am able to sleep in peace if I buy at the lower end of the P/E for the year!

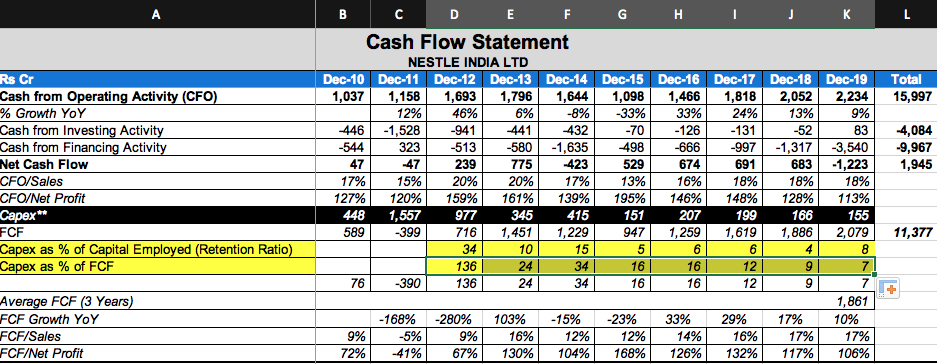

Hi - question around how to find the reinvestment rate of Coffee Can company since on a standalone basis ROCE is not of much significance (e.g. Colgate, Hawkins, etc.). I tried to do this exercise for Nestle by looking at the “Purchase of Fixed Assets” from “Cashflow from Investing Activities” and dividing that by Capital Employed (actual formula in the spreadsheet attached) . The numbers as highlighted look abysmal at ~5% from CY 15-19. Capex as a % of FCF has also been <20% the last 5 years. I am newbie and could have done something wrong while arriving at these numbers if someone could please advise. I understand that this is not a capital intensive business and has been able to grow the profits at ~20% last 3 years - is this a special situation where we can ignore the Capex, or how best to read it (“the reinvestment rate”) when investing from a Coffee Can standpoint.

Nestle India.xlsx (156.1 KB)

@A_shah - tagging you as well here in case you’ve any inputs looking at your recent posts about Nestle.

Thanks in advance

Mohit

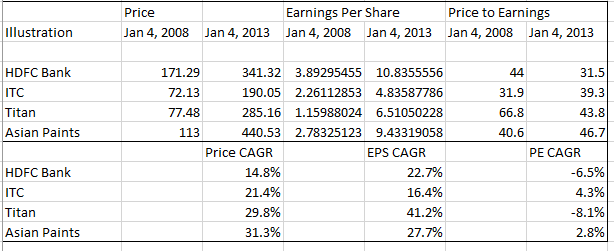

Does the starting P/E influence the returns of a Coffee Can Stock? I tried with a combination of ITC, HDFC Bank, Asian Paints and Titan from Jan 4, 2008 to Jan 4, 2013, i.e. from peak P/E to P/E 5 years later

As we see Titan that was bought at a peak P/E of 77.48 in Jan 2008 managed to give a close to 30% CAGR in price in 4 years as its earnings grew by 41% CAGR. So despite exit P/E being lower at 66.8, it still gave great results.

HDFC Bank managed 15% CAGR on the back of 22% growth in earnings.

Bulk of Asian Paints and ITC Price CAGR came from earnings growth alone. So the starting P/E is not so much of a factor over 5 years.

If the stock had been held till now, ITC has not given any improvement in price over the 7 years, but it has given dividends. So there is some return in the intervening 7 years. Asian Paints, Titan are still 4X over the 7 years; HDFC Bank 3X over the 10 years - so the overall portfolio still made a good profit. So very good thought process from Marcellus.

Only danger of these high P/E stocks is if the earnings growth does not happen, as P/E will fall. But these are champion companies and will find a way to grow back

This, I am afraid, is a biased view.

Past decade has been bull, well at least no notable bearish phase until recently.

To conclude a thesis based on recent market behavior can be fatal.

As long as earnings growth is high, share price returns will be quite decent unless valuations go out of complete whack. In case you are interested, I did a similar exercise on the valuepickr stocks (link). The main conclusion was if we pay high valuations and earnings growth turns out to be <15%, we pay a very hefty price in terms of long term decompounding of money. The best case returns is when we buy a business at reasonable or cheap valuations and business ends up delivering above average earnings growth.

I am sharing some of the snippets from Seth A. Klarman letters Dec 1995

As mentioned in your post if in 10 years Bajaj Fin will go to 20K then why not buy even at 4K? I am just trying to understand your rationale. Thanks

Disc: Not invested, not interested in either consumer loans or stock.