@deevee

Hi Deepak

Have been great fan of your’s. I do follow you on both Value Pickr and twitter and do take notice of what comes from you with great attention.

Let me put some of my view on Coffee Can

This thread was started as one of the method and I am sure there are many ways to heaven (or stock market success)

Off late This method is under attack for variety of reasons,

1- Marcellus

2 -High PE Critics

The Style has nothing to do with Marcellus PMS and it never was All in one method that included Valuation.

A simple Filer of 15% ROCE and 10% of Revenue Growth in each of 10 precedeng year and hold them for another decade - yes that’s it

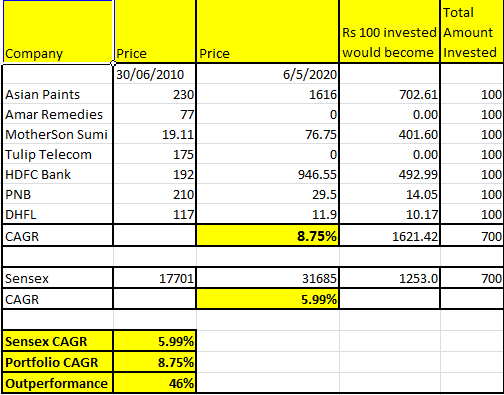

So I just went and picked up what the the porfolio as thrown in 2010 iteration from Unusual Billionaires Book turned out, No hindsight Bias as well

The 2010 iteration completes decade somewhere next month and lets see what we get

Total 7 Companies gets picked up

2 gets delisted - Tulip Telecom and Amar Remedies

2 BFSI Companies get blown up - PNB and DHFL

Only 3 left - mind you 57% of the pick bites the dust and this has to be the most unluckiest Portfolio picked up ever

Yet the Portfolio outperforms Sensex by whopping 46% , Sensex changes its composition twice every year and comes up with best 30 companies

Ofcourse 8.75 % CAGR is nothing to write about but with some tweaks I cant see why a decent portfolio with few additional filters cant outperform index even better.

If any Dumb Guy rode the portfolio then he actually made the smart decision. He won despite Corona, IL&FS , GDP slowing Down and more so Corporate Misgovernance in 4 out of his 7 stocks

He saves the frictional churning cost, saves taxes, Management Feea nd time. He does away with the need to keep up with all news and Annual reports and Concalls (It can be remunerative in very few cases and major emphasis on very few)

I have seen guys who can write thesis and thesis on “Value Investing” and compute “Intrinsic Value” to decimals having results nothing to speak about (No reference to any person in particular because there are just too many) and here a portfolio on AutoPilot crushes Index and so far all the iteration have outperformed the index so far

I rest my case. I respect all opinions and no matter what i’ll continue following your thoughts on both forum

Disclosure: No connection with Marcellus