It’s creating a negative bias towards the method , however it has be read and ignored too, not every company from the list will fly through the roof , seems Basu writing is only interested to criticise and ignore the good part.there will be laggards who will eventually need to be thrown out , remaining companies if outperform then they take care of such laggards, it’s true for any investment philosophy

1 Like

Yes you are correct and infact money life themselves run advisory services hence conflict of interest is there.

Following-up on my last post where I have highlighted the merits of Coffee Can style of investing - I definitely did not expect that within 6 weeks the Coffee Can style of investing will get such a massive test with the fastest decline into bear market territory in the history of financial markets. So now we can really test some of what Saurabh Mukherjea and his team at Marcellus keep going on about.

What I also did not expect is that some people are so quick to jump to negative conclusions about the Coffee Can method - sales talk, lot of bad companies identified, etc. etc.

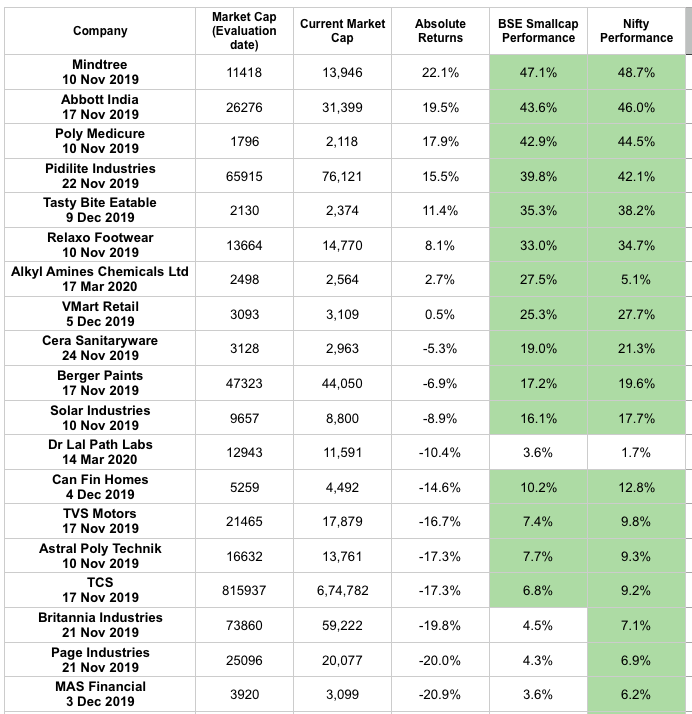

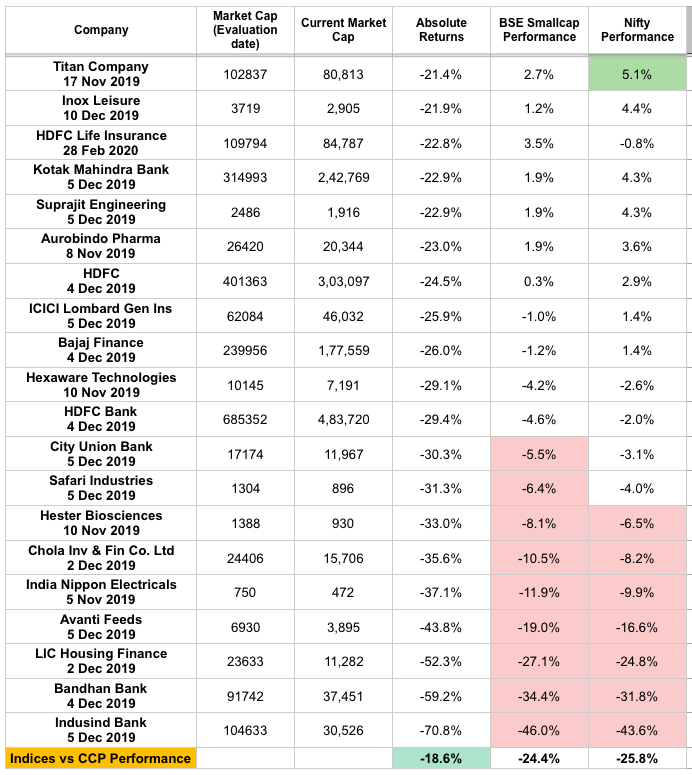

Okay so before I go-on any further, let me first share the performance of Coffee Can style of companies as of 20th March closing prices identified through Saurabh’s book Coffee Can Investing (In my post last month - there were no Financials and I’ve added those (like HDFC Bank, Indusind, etc.) as well here as per the Coffee Can criteria.) :

Legend for reading this table:

- Market Cap (evaluation date) - Ex: Market cap of Mindtree on 10 Nov 2019 was 11418 cr

- Current Market Cap - as of 20 Mar 2020

- Absolute returns column - provides stock returns from the evaluation date till 20 Mar

- BSE Smallcap Performance - This table actually provides a view on out performance / under performance of the stock since the evaluation date of the stock compared with BSE Smallcap index

- Nifty Performance - This table actually provides a view on out performance / under performance of the stock since the evaluation date of the stock compared with Nifty 50 index

- Green cells - If the outperformance of the stock is more than 5% compared with BSE Small Cap / Nifty 50 index (19 companies outperformed Nifty by more than 5%)

- Red cells - If the underperformance of the stock is more than 5% compared with BSE Small Cap / Nifty 50 index (7 companies underperformed Nifty by more than 5%)

Again this is a very short period of performance (4-5 months) before jumping to any big conclusions, however let me share what I’ve noticed so far:

- The CCP has outperformed both Nifty and Smallcap index so far (CCP -18.6% vs Nifty -25.8% vs Smallcap -24.4%)

- I’ve been doing a daily tracking of the CCP performance over the past 2 weeks which has seen the maximum turmoil in the markets - from global Covid related market crash to Yes Bank uncertainty to distrust in all Indian financials (see Indusind’s performance above) - the CCP has outperformed both Nifty/Smallcap indices significantly and never fallen as much / more than these indices at an aggregate level for even a single day (feel free to go ahead and verify this yourselves).

As someone with no formal education in finance having spent 6-7 years in the market and yet to come across any other person/book which so easily separates the wheat from the chauff (brings down 5000+ listed companies to 100-150 researchable list for CCP) and if this CCP style of investing enables me to outperform major Indian indices over a long period of time (yet to be seen with my own eyes but all the proof of the puddings are available in Saurabh’s book) without having to spend significant amount time tracking the markets, why shouldn’t I fall head over heels for that kind of an approach!

However, if someone reading this is such an expert that they can time bull / bear markets precisely or have such companies in their PF which are actually giving positive returns in this kind of a market mayhem, then I can only tip my hat to you for being an exceptionally good economist / stock picker. I don’t have such competence and dare I say 99% of investors have it either.

10 Likes

This correction has given a chance to deploy cash into compounders and high quality businesses today. How long and how much worse this could get for humans and the economy is anybody’s guess

I like to consider one pharma company as signs do point towards that sector coming back to the market fancy. And due to lack of understanding I cannot really identify a business. I do understand that it is a lottery for many due to approval of fresh drugs etc:. A basket approach would make sense in this case or one could venture through a sectorial mutual fund.

I have a basic understanding of the industry. I have been trying to read and understand the space during this lockdown.

Divi’s lab is obviously a favorite of many (incl. marcellus). And as per my limited understanding of the industry I want to consider mainly contract research and manufacturing services companies or CRAMS as they are called.

These CRAMS companies tend to have a moat due to cost of production obviously and backward integration but most importantly trust of clients or big pharma.

Often investors tend to underestimate stickiness of customers to businesses. CRAMS businesses are entrusted with access to IP of large pharma players for making the API (active pharmaceutical ingredient). An API is basically the active ingredient that causes the effect of the pill.

Simple example would be, in a painkiller the ingredient that actually relieves the pain. A small portion of this active ingredient has a strong effect so actually only a tiny amount is inserted into the said drug. This could vary of course. And usually you will find the name of the API and amount at the back of the drug. Paracetomol is an API for crocin or calpol (made by gsk). Usually size of the pill will be the same but you can have varying amounts of API like a 100mg pill or a 500mg pill. (This is a rather raw understanding from me please give me inputs if I’m wrong).

These API’s have to manufactured through a certain process. While costs have to be kept low, the quality cannot be compromised on. A CRAMS company will actually have some R&D on improving such processes for the manufacturing of these API’s.

There is a sort of value chain for these API’s. You have the lower end that is bulk generics and chemicals then there is some specialized chemicals and on the upper end is NCE.

NCE is a new New Chemical Entity that is brought by an R&D big pharma firm. It is in its first or initial stages and after due trials and going through the requisite phases might translate into a cure and a drug.

It is among the early stages of a drug development. NCE is like a high risk phase as no one knows if the drug will succeed or not. Usually volumes would be low during the initial phases of NCE CRAMS and then as the drug progresses through its phases there would be a rather meaningful jump in volumes. However, there is risk of failure for the big pharma company and failure in the later stages of the drug is far more costly then a failure in the early stages.

CRAMS companies actually help offset this investment by taking on NCE CRAMS, custom synthesis, R&D of process for ramp-up and so on. Margins are higher but volumes might be lower for CRAMS companies engaging in this aspect of the industry.

A side note: we are not talking about generic drug companies here. A generic drug company actually formulates a generic version of the drug after the exclusivity period for that drug is over. An example would be, Calpol is a paracetemol. A generic version of Calpol could be made and launched under a new name or under its generic name itself like paracetomol. Now to do this, one has to actually go through some level of R&D (not to the extent of the original IP holder so to speak), trials and then seek the requisite approvals. An example of such a company would be Sunpharma. (again please correct me anywhere that I’m wrong)

Coming to Divi’s

Divi’s is more into Bulk and Generic CRAMS of API’s. So essentially they do not actually manufacture end products for the customer, rather a supplier to the big pharma companies. So even the FDA issue they could solve rather quickly. This is also testament to their quality of product and process. Being a supplier to Big pharma also significantly decreases the chances of FDA issues in the future for them. Apparently Divi’s spent 50cr during the FDA issue and have not only looked at the immediate issues but also looked forward and made investments in anticipation of future regulatory guidelines.

Divi’s are actually market leaders in producing important API’s for painkillers and cough drugs. Some 70% of the API’s for painkillers in the world are made by Divi’s! it is a monopoly in this space along with cough syrup API. Naproxen (api for painkillers) came first and then they took market share away very quickly for dextromethorphan (api for cough) from a dutch leader called DSM.

Over time, Divi’s also ended up winning contracts for custom synthesis (high margin business apparently). If an API cannot be made or it is impractical or unviable to be made readily in house by the CRAMS company then in such a case a “custom” or specialized solution is needed.

It is where a molecule or API or whatever is to be made exclusively for the customer at a certain scale. It can be a very small run or a mid scale run. The CRAMS company may have to come out with its own way and method of synthesising the product. And if it breaches a certain scale then it shifts into a large scale contract manufacturing system.

This actually falls under NCE CRAMS or early stages of the drug. As explained earlier in the post. Overtime this business has grown into a very large pie (between 40-50%) of Divi’s revenues I believe. This sort of service involves high levels of trust as early stage IP’s and research have to be shared with the CRAMS company. Of course legal binding is there but there is a high level of trust in this case let alone the quality of the product that comes out. NCE CRAMS is where the higher margins come from.

If the company is competing with big pharma on some level through generic drugs of their own etc: logically no big pharma will ask for CRAMS from them.

Essentially a generic drug player would actually challenge a patent by reverse engineering a drug to produce a generic version of it. If they won they would get a period of exclusivity for it, resulting in abnormal profits during that time. Of course there is uncertainty on the approvals, if the challenge would be won etc: It is basically launching a new drug with low R&D costs as bulk of the testing, R&D, marketing of the cure has already been done by the big pharma company.

But this would mean challenging and competing with the big pharma companies, the actual clients of a CRAMS business. The CRAMS Business revolves around IP trust to a large extent in my limited understanding. Divi’s is a pure play CRAMS business and does not enter formulations etc: at all.

Divi’s is a fully backward integrated company. With big Capex coming on board in the near future.

The market is big and they are leaders globally. They can keep deploying capital at high rates. It will very tough for competitors to set up and compete with them due to their backward integration and cost effecienies along with scale and trust.

They can essentially enter an API and snatch market share rapidly due to their strength as a company.

Relocation from China. Big companies will take steps to further diversify supply now. A weak rupee should logically help but I do not know how they hedge their forex, contracts etc:

This business seems to have a very strong moat that can only keep getting stronger as it expands and keeps integrating itself. There is no question about the pharma market in general and its longetivity as an industry. It is highly regulated and expensive to enter let alone compete.

I do not know what to make of the valuations and I request forum members to give their insights on Divi’s as a compounder business and from a valuation perspective.

21 Likes

https://marcellus.in/video/impact-of-ongoing-events/

From Marcellus a webinar on current events and then the outlook I guess…

1 Like

Quite possible as I’ve a similar observation… Add to it a La Opala and Kajaria Ceramics as well

Hi All. So Asian Paints has been a consistent inclusion in the Coffee Can method as well as Marcellus’s Consistent Compounders Portfolio. While the Co and indeed the stock have done very well over the past few years, i couldn’t help but notice the sizable promoter pledges on Asian Paints. Currently, about 12% of the promoter holding (promoters own 52%) is pledged i.e. ~6%+ of the Co’s total is pledged. Given the stability & pedigree of the business, this isn’t necessarily a risk right now but just wondering why pledges are relatively high and what are the promoters using these funds for? I also saw that the pledged portion used to be as high as 22% about a decade back, so its definitely come down which is a positive but just curious to know the end use of these funds, etc. if anyone has any insight into this. Ideally, you want to see zero/negligible promoter pledges along with a debt free / net cash co.

Thanks.

2 Likes

Hi it’s good for a newcomer in market to look for such investing methods buy you have to monitor your portfolio closely and if something is wrong better to bell out and look for better opportunities

Welcome antokdavis. I am also pretty new to investing and couldn’t agree with you more.

My philosophy is similar to yours and unfortunately as the prices were high across the board, recently I had bought slightly lower quality companies whose valuations appeared cheap Eg: Edelweiss, PNB housing, Manappuram etc. In the recent sell-off I lost big time.

My friend buys only “high quality compounders” and was heavily indexed on Avenue Supermart, HUL, HDFC Bank etc. He lost much less and he is looking to add more of these now as they have also corrected

I think now it might give us an opportunity to have the best of both worlds i.e. quality at reasonable valuations (if you have more free cash to invest that is + market continues to tank some more)

1 Like

The way I think about it is there are 3 risks -

- Business risk

- Valuation risk

- Management risk

For “quality” companies generally 1 & 3 are less. Hence to adjust the risk / reward equation, market values it highly and PE increases (to what we think is irrational). Also many investors / investment companies will have red lines on business and management risk which will rule out most companies leaving them with only few “high quality” companies to invest into. SIPs also flow to these companies only from people blindly doing it. (Another point is that for us it is easy to quantify valuation risk but not so easy to quantify the other two risks). If enough people continue to believe in the same story, the stock can stay at the high PE level (irrational) for many years.

I agree with you and will not touch Titan or Dmart still. However HDFC Bank I feel has fallen into my range now. I do not know the bottom of any share. However it is a bet of probability. To me the risk / reward for “quality compounders” has become much better since the recent fall and the risk / reward of smaller companies has become worse (as I fear some might even go bankrupt). Hence mentioned it.

1 Like

The fact that you are safe with quality and all is one of the biggest myths going on since decades. And whatever is in trend is called as quality. 5 years ago, both Asian Paints and Page Industries were called as quality and how such companies always deserve premium. Now in the past 3 years, both the “business” have underperformed. However, shares of Page have corrected by more than 50% from top while Asian Paints have withhold. So Asian Paints is “quality” while Page has been now demoted from that pedestal, even though business wise both have underperformed compared to their high valuations.

The advantage which these kind of “experts” always posses is since all they talk about it are companies which are recent winners, so recent trends is always on their side. And thus it is easy for newbies to get trapped in their ideas.

4 Likes

I had the same pain and TBH, same as your points, it worked for me to recover some loss. But now, i stopped listening to all the recommendations, news and noises and spending worthy time on learning the company performances. I restricted my PF to 5 companies and I am satisfied with the focus. We should always do our own homework and be prepared to face the market. My method is “Study the company as such you are offered to buy its whole assets”

I think there are two-three constructs which have been mixed together to present the Coffee Can Investing. Let me explain how I look at Coffee Can Investing:

Point #1. Buy for long-long term i.e. “Whatever set of stocks” you decide to buy, forget about them for next 10-15 years i.e. don’t take any action (buy/sell) for any reason and “Stand by them”. The idea is that though some of them will die (underperform), the others will rise up so much that they will very well compensate for under-performers.

Point #2. Helping on finding the “Whatever set of stocks” i.e. what stocks to buy so that it is easier to follow buy and forget strategy for more than a decade. Here Saurabh Mukherjea jumps in to give a filter:

2A. He suggest a simple two variable screener: High ROCE/ROE (>15%) and High Revenue (>10%), every year for last 10 years.

2B. He prefers to ignore the Valuation of the stocks in point #2A (he has explained it in his book the reason of it in detail, but summary is the #2A stocks will grow enough so that any current high stock price will rise further).

Point #1 is the essence of Coffee Can investing i.e. once you buy, stick to the stocks (yes, even if they die or if they become super-expensive). Point #2 is just a way to operationlize the initial buying. We can device our own Point #2, with adding more variable, reduce variable, make valuation aspects (whatever your prefer P/E, P/BV, PEG, DCF etc.) part of the screener.

I think Coffee Can investing using above two points is very helpful for a passive investor (an engineer/doctor/salesperson etc.) whose main profession is not investing but would like to gain from wonderful businesses available (listed) to buy. That is every economic participants have to wear an Investor hat every once in a while. And if they have to do it in stocks then Points #1 and #2 together would have a higher chances of favorable returns, without doing 100s of hours of research. This is very much akin to buying real estate (flat/house/land) by engineer/doctor/salesperson. There also this person is not supposed to be a full time real estate expert (flips flats every now and then) but since he has money he has to invest somewhere for returns, and society in general suggest a real estate.

For an active investor, like the folks on valuepickr firm, we love to research business, their books, their growth prospects, their long term economic prospects , their “reasonable” price to buy a share. We love to stay awake in night to analyse them, brainstorm with friends etc. i.e. every year we spend 50-100x more time/effort than a usual engineer/doctor/salesperson for making an investment decision.

(By active investor, I don’t mean we trade often. I just mean we spend 100s of more hours every year on analysing a business than a normal folk who doesn’t want to or couldn’t spend this much time/effort, but still wants to be a player in India’s business growth.)

Hence, for such a layman investor to participate in country’s Business growth story, 3 options are reasonable:

- Equity mutual funds

- ETF

- Coffee Can investing

This thread proposes that third Option is supposedly the best passive investing method amongst these 3 options.

For more “into the game” folks, we can have our own game play and can very well ignore the above options (or keep them a small part of our portfolio).

10 Likes

Problem is that it is tough to follow Coffee Can investing unless you are dead or have a saint like mentality. Even quality names go through temporary trouble and it is very common for people to move out of the scripts during those bad times. Back-testing at least gives you the perspective about what happened in those bad times compared to the broader market.

Personally, I would love to follow Coffee Can investing, but I know I still don’t have saint like mentality.

However, I try to stick with quality. Quality investing is not about high PE investing. I mean, Quality companies trade at high PE, but reverse isn’t true.

For example, IRCTC, Affle, IndiaMart etc. all trade at high valuations but they still don’t qualify as quality simply because one important filter of quality is consistency of performance over long listed history: how they’ve allocated capital, how they’ve honored minority shareholders, how they’ve managed the company operations, how they’ve performed w.r.t guidance given etc. So, Quality companies include a LOT of qualitative filters which needs time to build.

Another important parameter of quality is how the companies’ products fare w.r.t its industry, i.e. How under-penetrated those are, How better the company is doing to ensure quicker penetration, How insulated the demand of the companies’ products are during economic downswing etc.

Quality companies do go through prolonged rough phases.

HUL indeed went through ~ 10 years long time correction. And, if you study HUL of that period, you will know how they were facing issues in competing with agile homegrown FMCG players like Marico, Dabur, Godrej etc. Not many companies come out of that difficult phase. HUL has since reoriented their strategy to focus on premium products where the competition is less and started doing well. In the retrospect, it is easy to say that HUL recovered because of quality but when you are in the midst of it, it is easy to assume that it had lost quality, & it was somewhat true indeed. Coffee Can investors could’ve held HUL through that phase but quality-focused active investors were right in selling it during that period. They can always get in after the performance becomes steady again.

ITC was a quality compounder because (i) Legal Cigarette was much under-penetrated compared to illegal Cigarettes, (ii) Taxation was less strict & (iii) Size of ITC was appropriate to grow despite the Taxation trouble. But, size has become the main constraint for ITC now. They can no longer grow without other verticals firing. So, they did a prolonged Capex and is waiting for that investment to bear fruit, mainly in the FMCG. I fear that it will take significant time for ITC to start growing again as (i) size is a constraint again, (ii) Brand building takes very long in FMCG (Most prominent brands in FMCG are nearly 50 years old.). So, ITC, in all probability will go through prolonged time correction, and will get re-rated if it shows growth again.

Actually, here is the dilemma of claiming a company as quality. One may call ITC as low-quality business now, or could’ve called HUL a low-quality business during the noughties. But, I believe that in the context of Coffee Can investing, quality is much more about the gene or culture of a company. You got to put faith in a company that has lasted & is growing for ~100 years.

Also, coffee can investors must diversity to protect themselves against temporary/prolonged slowdown in one or more scripts. Quality focused active investors can afford to own a concentrated portfolio, as they will bail out if the temporary/prolonged slowdown is visualized in a script. I am not a supporter of Marcellus but I believe they sold Marico because it is now entering a prolonged slowdown phase, and Marcellus is an actively managed PMS.

Regardless, I enjoy all the opposition of Coffee Can / Quality investing. It at-least ensures that not everyone will follow the same investment style. In fact, one anecdote states that not many actually follow this style:

2 Likes

Marico is still a coffee can candidate. But, may not be a candidate for active quality investing which that PMS follows. It is perhaps a contrarian bet at present like ITC.

FYI, coffee can approach for me is never what Mr. Mukherjea describes, but the approach of buying and holding of quality companies forever, disregarding underperforming phases.

Active quality investing on the other hand invests in quality companies which are assumed to perform well in the near to medium term (< 10 years).

Mr. Mukherjea’s version of coffee can investing is buying the companies which pass the filter and hold at-least 10 years. So even if one has bought Marico 6 months back based on the filter, he is supposed to hold that for 9.5 years more.

Financials don’t pass the CCP filter. Probably, Axis Bank & HDFC Bank was ever part of the portfolio.

1 Like

I dont know what exactly your definition of coffee can investing is , but from what you have written, i feel you have certainly different idea from layman like me

Lesser mortals like me who arent wise and smart understand it like construct a portfolio of “good quality” companies and sit over it for atleast a decade

Saurabh has a simple formula of 15% ROCE and 10 % earnings growth in each of preceding 10 years.

Nowhere its written that you cant apply additional filters like valuation (i like debt free and MNC). And you can have whole together different filters. To each one his own.

I havent read so far anywhere that coffee can means buying only High PE companies. Its just that the companies which make the cut in Saurabhs filter tend to have high PE. And if you are not comfortable with valuations then dont buy. Its that simple.

There is difference between quality company and High PE Stock, Quality might or might not have high PE but not all high PE stocks are coffee can contender. And here quality can have different meaning or filters both quantitative and qualitative

And even the proponents of coffee can are certainly mindfull of valuation, for eg i am still likely to prefer VST industries over pidililite.Vst currently is at mouthwatering valuation of 4% dividend yield and in times like this you get HDFC bank and kotak at decent valuation.

So can we agree on defination is that you buy good companies (defined on your whatever parameter) and sit over it?

I have seen people who have shut off their porfolios (they dont know they are doing coffee can investing and neither do they care whats the name) like my uncle and few senior investor have grown exponentially rich. All they did was they bought and held on, come whatever may.

This investors are smarter then most of us because they know that they dont know (Major emphasis on they know that they dont know ) and easiest thing to do is to buy and hold then reading buffett, munger, soros, Fisher and lynch and macros and picking holes in some theories. They knew that having their own ideas of world and market is waste of time.

i know a senior investor who has never sold a single share in his life (even when he knew that this stock is going to 0 , he had simple principle -only buy and never sell) and as a result his portfolio consist of Motherson Sumi from IPO and MRF and likes. How many can show such discipline and adherence ? Zero

Many talk about Warren Buffett at the drop of their hat as if they have decoded him and there is nothing great about him, just if one were to have the 10% of patience he brings to table. He is holding on Sees candy from 1972, held washington post for 3 decades, holding on Coca Cola and GEICO, wells fargo and American express for around 3 decade so on and so forth.

Warren Buffett endorses coffee can when he says

When we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever

If you read Unusual Billionaires of Saurabh , then each of his Coffee Can portfolio has beaten index by a good margin.

Mate, If i were to say , rather then picking holes in some theories, it would be better to do what on likes and let other do what they like. To each one his own. There are many ways to make money from being passive investor to microcap investing to trading derivatives. Each one does what he does because that suits him temperamentally and its for that reason we have market.

5 Likes

Hi antokdavis,

Thanks for bringing two other possible instruments, Real estate and FD in discussion. It helps to do a relative analysis of why stocks and not the alternatives (opportunity cost).

What is an investment - it is the process of sacrificing current consumption to afford more consumption in future.

What is saving - it is the process of maintaining the same consumption in future.

Purchasing power gets eroded with inflation.

Savings and investments are related with a minor difference. Savings try to safeguard the purchasing power, without the downward risk or upward reward, while Investment try to increase the purchasing power, but carries risk (chance of loss).

Hence the Investment game is an endeavour of getting higher real return (post inflation & taxation) while overcoming risks. And all of the investing community try to play this game with their own strategy and tactics. Some become successful and others fail. Even those who become successful, not all their bets go right all the time and they shrug and move on to their next bet. What matters is that mojority of the bets should come right (and not necessarily all bets), and the bets which go wrong shouldn’t wipe the overall wealth (purchasing power).

There is no guaranteed scheme as such in Investment. What matters is risk adjusted returns, and that is also probabilistic as risk adjusted return may also not fructify (as it was still highly probabilistic/likely but not 100% guaranteed).

Saving instruments:

Best instrument for Saving in US are TIPS (Treasury Inflation-Protected Securities). We don’t have an equivalent in India but FD’s in general gives Inflation plus 1-2% return, which after tax is more or less equal to Inflation.

So FDs over a long term are actually not Investment but closer to Savings.

Same goes with Gold, which has been a fantastic hedge against Inflation (over centuries).

Real estate - It is an investment with its own set of issues and rewards. Issues include less-liquidity (try selling a house within 1 day/week), maintenance, registration/stamp duty charges, tenant unavailability etc. Rewards includes inflation adjusted small return, supportive government schemes (80C, Section 24, no capital gain if reinvested etc.), ownership and societal pride (for some it matters)

You mentioned that “who bought real estate have lost quite a bit of money”

This is true, but for a small period of last few years. Do an analysis of 20, 30, 50 years and you will see investors have made an inflated adjusted return. So it has not been a “bad investment” though the real long term return might be in tune of 4-10%.

It is important to get own conviction. A person has full right to stay invested in gold, or FD or Real Estate if he is not comfortable with Coffee Can method or even an ETF (wherein he can believe that all businesses are fraud and will go bust and a welfare happy state without crook businessman will be soon emerge).

Passive investor can have a leap of faith that most of the businesses will flourish and he can participate in the wealth creation.

How: ETF, Mutual Fund or Coffee Can (with slightly direct stock exposure).

Now if Businesses fail and communism comes, all the above go to gutter. But if things continue normal as we see, he could get good return without headache of following markets/companies/trends and spend that saved time on improving his job skills, hobbies, more family time, social service. Time is a very scare and limited source and what better if your wealth grows without much demand on your time

For me personally, Businesses are not full-proof and many die but successful ones keep on expanding and I love to analyse which are likely to grow and which one will go bust. And I will be putting my money on my conclusions, knowing fully that I may go wrong and will accept the loss with humility.

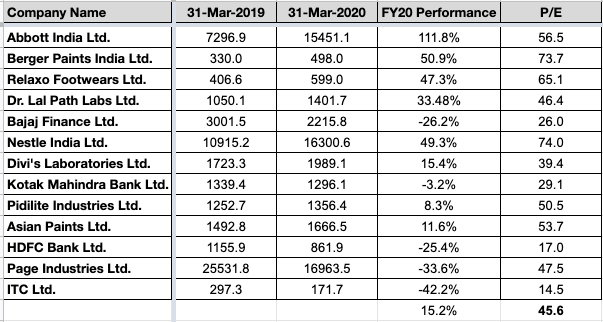

Latest newsletter from Marcellus team highlighting the stupendous outperformance of CCP vs the Nifty in FY20

Marcellus CCP +7.6%

Nifty 50 -25%

Outperformance 32.6% (STAGGERING)

Based on the publicly available info - this is what I believe should be the current CCP holdings. Have tried to calculate what has been the FY20 performance of these holdings assuming equal weight holdings in the beginning of FY20. Marcellus CCP being an actively managed PMS - has different weights allocated and also has had some churn in FY20, have publicly revealed exiting Marico around Q3FY20 and entering Divi’s Labs. That is why the FY20 performance number below is different to what they’ve shared.

The two numbers at the bottom are based on equal weight portfolio-

FY20 Performance +15.2%

Average Portfolio TTM P/E - 45.6

Number of key takeaways for me from this:

-

4 out of the 13 companies have performed similar or worse than the Nifty with >25% downside

-

Getting even 60-70% picks right in a portfolio can enable significant outperformance vs the market - 30% is massive by all means and regards, do not expect this over a period of time

-

Even Marcellus CCP does not appear perfect - as borne out by numbers above, equal weight portfolio of above 13 companies would have given them double the returns in FY20 (in no way a criticism - just an observation and IMO they’re damn close to being perfect, trust me!)

-

The Average TTM P/E of this CCP is 45.6 vs Nifty current P/E of 16-18x and this portfolio is absolutely smashing the Nifty - please read, re-read and again re-read this point!

@antokdavis - Sincere request to you to please read this newsletter and all the associated newsletters hyperlinked in it, before cluttering this thread with anymore mumbo jumbo lacked by an adequate understanding of Coffee Can approach to investing. Quite a few others have already tried to explain this above to you without much success it seems. With each and every subsequent post, the quality of this thread is getting further diluted.

24 Likes

This thread is getting extremely cluttered without posts which add zero value. Please go through the entire thread to see if certain points have been covered before.

I will be deleting posts which do not add any value going forward. Repeat offenders will be suspended.

13 Likes

Very valid point covered in this report why paint companies are better compared to FMCG in terms of reinvestment returns and pricing power.

Disc - Adding Berger paint in this market fall.

3 Likes