Simple thesis

Company has expanded capacity by ~2.5x which based on below calculations should lead tom ~4x PAT from FY22 levels by FY25 (contingent on global demand). Applying 15/20x multiple to this PAT stock can be 3-4x of current market cap. However, there are negatives and risks as well which are highlighted below

Description

Coastal is a shrimp processor and exporter out of India. In FY22 it exported 6,218 MT of shrimps vs India shrimp export volume of 7.5 lac MT giving it an ~8% market share. Coastal had a capacity of 6,500 MT as of FY22 and post recent expansion capacity has increased ~2.5x to 20,000 MT (source: incred research). Debt to equity is at 0.7x

From AR - With shipments to the US, Europe, Canada, China, Hong Kong, and the United Arab Emirates, this Visakhapatnam-based company is one of the largest shrimp exporters from India to the US market. The company provides a variety of shrimps such as raw frozen blocks and in IQF, cooked in frozen blocks and cooked in IQF forms, and cooked in frozen blocks and cooked in IQF forms based on customer specifications

Auditors- . Bramhmayya & Co. These auditors were roped in to audit Satyam post unearthing of scam. Bankers include HDFCB so that’s good.

Related party - company does Rs8cr of sales to its US subsidiary (seacrest foods) on turnover of ~Rs400cr

Positives and quick valuation

Assuming 80% utilization on the expanded capacity of 20k MT Coastal can do volumes of 16k MT by FY25m (doesnt include Odhisha expansion). Their calculated realizations were $8.8/9.5 in FY21/22. Assuming $8.8 realizations in FY25 or Rs703 per kg or Rs703k per tonne this gives revenues of Rs1,125cr vs incred’s estimate of Rs1,300 cr in FY24. EBITDA margins over FY13-21 have averaged 9% (FY22 seems one off). Assuming slightly higher 10% margin in FY25 (can be higher given operating leverage) we get an EBITDA of Rs113cr. Assuming other income of Rs2cr (8% yield on Rs25cr cash); interest cost of Rs13cr (7% cost of debt on Rs172cr of current debt); depreciation of Rs23cr (11% depreciation of Rs200cr of gross block which includes Rs90cr of current gross block plus Rs90cr of current CWIP plus Rs20cr capex for Odisha expansion). This gives a PAT of Rs59cr and applying 15/20x on this PAT (multiples are subjective) we get a market cap of Rs878cr/1171cr which is 3/4x of current market cap of Rs295

Coastal.xlsx (10.3 KB)

cr

Looking at it another way, their asset turn (sales divided by gross block) pre covid that is from FY18-20 averaged ~8x. Post Odisha expansion gross block will be Rs200cr so 8x gives Rs1600cr of sales vs Rs460cr in FY22

Negatives

Q3FY23 and likely Q4FY23 can be bad quarters. Global shrimp prices (if you see chart below) have come off from highs of $15 till June 2022 to $11 in Oct-Dec 2022 likely as Ecuador has increased supply (see incred note). Avanti feeds also reported a 19%/37% fall in revenues and EBIT q/q in Dec 2023 qtr for their shrimp processing division. Fall for Coastal can be higher given capacity expansion

Also given lower shrimp prices and withdrawal of power subsidy by Andhra govt for non aqua zones farmers were planning to go on a crop holiday (Nov 22 article - Shrimp farmers in Andhra Pradesh mull crop holiday as prices fall - The Hindu) which would limit raw shrimp availability for players like Coastal thereby limiting volumes unless they import shrimps for processing but dont know how cost dynamics play out here

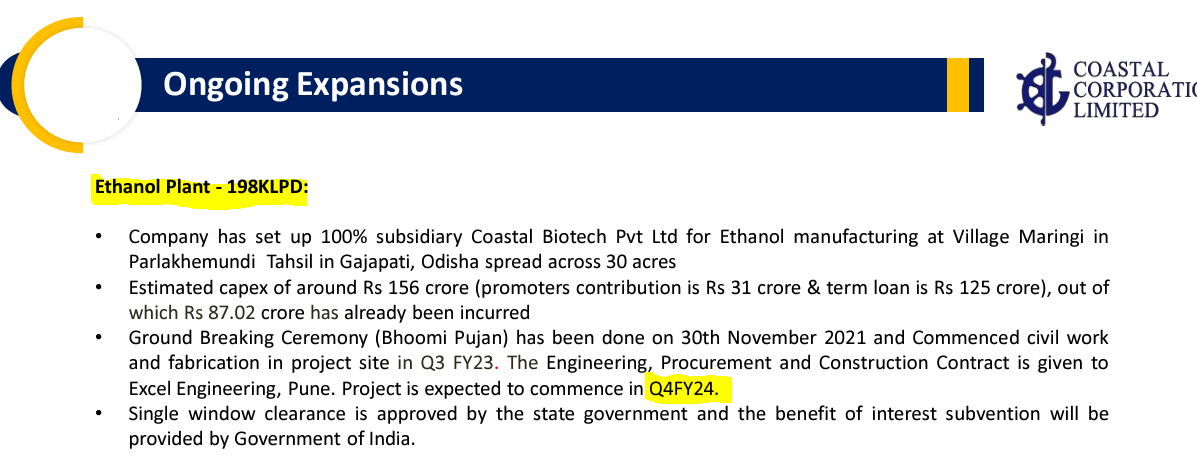

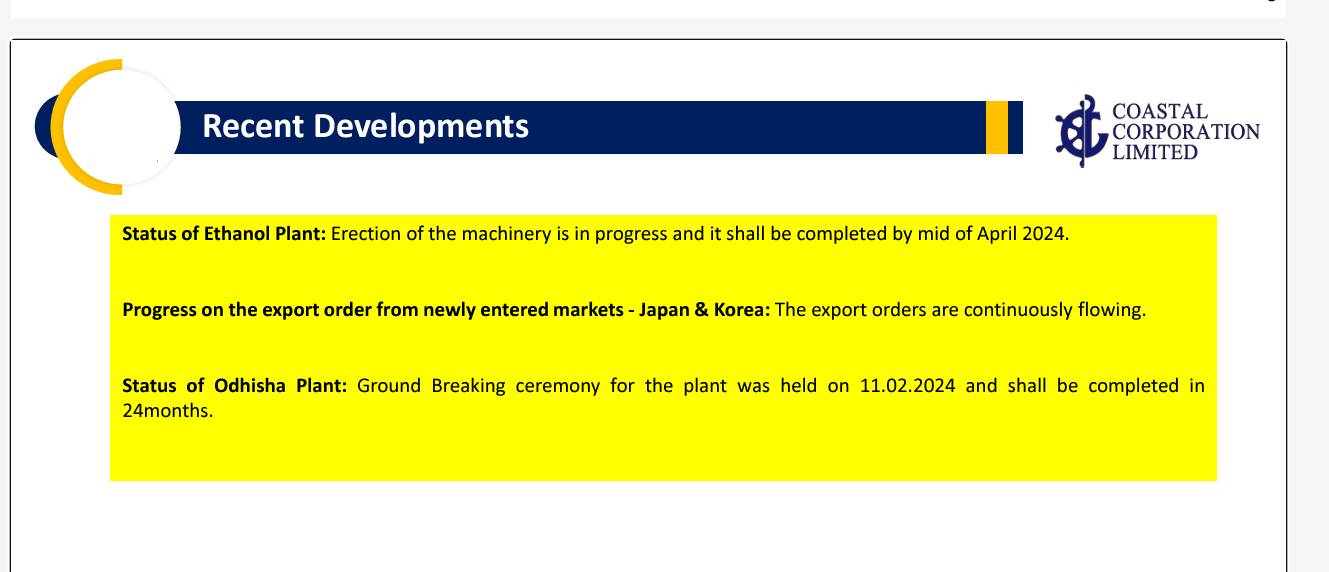

Also company is setting up an 198klpd ethanol plant via its 100% sub coastal biotech at a capex of Rs156cr (debt of Rs125cr). On the face of it raises questions as to why would the company take on so much debt and venture into a completely separate line of business. Ethanol capex and associated revenues have not been factored into my numbers above. Incred

Crisil has termed the company has “issuer not cooperating”

CFO to EBITDA cumulatively over last 10 years has been 43%

Would be great if others who have an interest in the name can also share their insights and thoughts on valuation and nos. or any other positives or risks. Also, how can we track industry/shrimp price on real time basis?

Overall they have expanded capacity significantly however industry is going through a very rough patch and hence near term can be very painful.

Incred Research Services Pvt Ltd CTW@IN Coastal Corp Ltd_06Jun22.pdf (346.9 KB)

Incred Research Services Pvt Ltd CTW@IN Coastal Corp. Ltd_27Nov22.pdf (304.7 KB)