Any update on ethanol plant commission?

In Jun’24 results, no sign of ethonol numbers.

For Coastal Corp, the freight is by air or by ship?

Recently the freight costs have been reduced.

By ship only, it takes more than 30days for transist.

I heard in some concalls that US freight cost was not much impacted in the past few quarters due to containers unavailability.

Thanks. Last I checked in my circle, the freight has substantially reduced.

Anybody has AGM notes and update on ethanol unit.

Current distillery market is very fragile due to high grain prices

Ethanol plan to start production in Feb 2025

Update on ethanol plant status

Management is guiding for only 500 Cr top line in FY25, which is ~15% growth.

I looking for any margins improvement in Q3 & Q4 so that over all margins of FY25 can be at least 9%.

If we compare with Apex frozen then coastal corp margins are better in the previous 2 quarters due to better geographical mix (As they have added Japan to their portfolio).

I am expecting ethanol plant margins also near to 5% only in the current environment.

2 Likes

what is the impact of the ethanol plant coming live in next 2 quarters , seems to be a good incremental gain once utilizations come , does anyone know how much realizations can they see on this plant going live

We can expect at least 500 Cr revenue at full utilization levels.

In the current environment, we may expect margins> 10% as maize price is cooled off and FCI rice is also available for grain based ethanol manufacturer’s at a subsidized rate.

FY26 could be ~1000 Cr revenue with 7-9% margins.

1 Like

https://www.bseindia.com/xml-data/corpfiling/AttachLive/dce746b4-2cdf-4095-b7b8-50d0d3244344.pdf

results are out

AGM Notes:

Ethanol biz: revenue start reflecting in Q2 numbers, plant is running at 90% capacity utilization levels. Raw material is FCI rice & Maize.

Shrimp biz: US customers are ready to absorb 50% Tariff and shipments to USA are going on without any interruption. There will be no impact on business due to tariffs.

Apex frozen also confirmed that all US customers are ready to absorb 25% Tariff and few customers are ready to absorb 50% tariff also.

Over all i am expecting good numbers in Q2 ~250Cr top line with margins similar to Q1.

3 Likes

What interests me is that shrimp waste can be used in production of ethanol. However, the company does not yet use this method due to less ethanol yield from this method. The price for shrimp based ethanol (not sure if I’m terming it right) is also higher than rice and maize based ethanol. But I hope in future this may slowly be achievable. If shrimp waste ends up in the production of ethanol (a long shot right now), it can be very beneficial for coastal corporation’s margin profile.

Disc: Studying the stock. Not a recommendation for buy/sell.

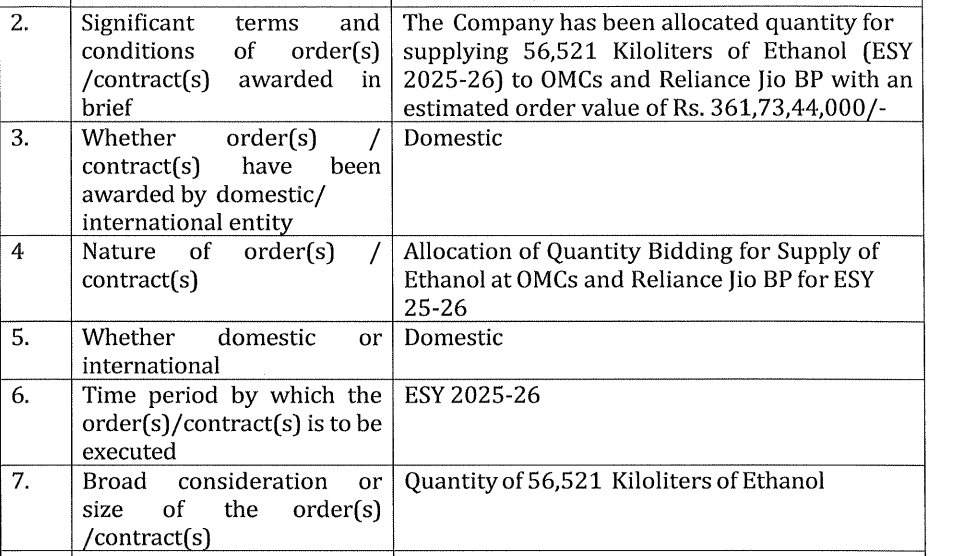

Company has been allocated quantity for

supplying 56,52L Kiloliters of Ethanol (ESY

2025-26) to OMCs and Reliance f io BP with an estimated order value of Rs. 361,73,44,000

2 Likes