Didn’t follow you. Are you comparing CMS with Infosys/TCS ?

I’m not comparing them per se rather trying to figure out how much of their tech solution business overlaps with the large and midcaps listed IT giants.

For eg: CMS provides ATM software solutions, from what I (being a non-tech guy) understand this includes the algo on which the software of ATM machine works now TCS also has a similar service which they provide to the international clients as of now, but can very well be done for the domestic banks/fintechs at a cost effective rate.

Like for eg this 2013 agreement with federal bank

I understand that this may be a far fetched idea but can anyone here point out if this can potentially emerge as a threat to CMS’s tech expansion?

3 Likes

Being from a tech company similar to TCS, I would say this is a scenario thats possible but most improbable . How large is the ATM business ? Will it move the needle by any meaningful amount for bigwigs like TCS ? If not then why would they get into it ?The big corporate groups have enough muscle to outmuscle anybody if they wish but the reward have to be large enough .Also TCS ,infy etc are not in the ATM deployment business themselves…sure they can develop these softwares but they have to sell it to companies like CMS who deploy and manage ATMs or to those banks who manage their own ATMs and at least according to CMS ,their number is reducing . So it would be a dwindling market with pre- existing competitors with end to end presence .

11 Likes

While I didn’t get any response to the email queries, the mgmt has given some indication in the recent concall.

3 Likes

Although the receivables are increasing YoY (almost 27% of total assets and this percentage has increased YoY), the cash conversion cycle is -401 until March 2024. This is because the payables have increased more rapidly. As a result, CFO is healthy with CFO/PAT more than 100% and CFO/EBITDA more than 73%. One thing that caught my attention is the zero promoter holding in the company (around 6% shares are held by Rajiv Kaul as a super investor). I am trying to find the reason behind the promoters selling their stake.

PS : Studying the company. Was keen on buying it but now a bit reluctant as better opportunities might exist in the market.

The promoter was a PE fund, Barings - they will have to exit at some point given fund life constraints. No PE selling pressure overhang

3 Likes

PE has already exited completely around 3 months back. CMS Info is now a publicly held company with Rajeev Kaul owning around 6%. He converted his ESOPs to increase his stake.

2 Likes

Mr.Rajeev Kaul is a very visionary person, he did work at Microsoft.

they sold their overall stake for the company’s growth, But it did not leave the company. They have stayed with the company through public investment (6% stack) because they believe in its growth.

6 Likes

CMS Info Systems Limited Financial Highlights from Q2/H1’FY25

| Metric | Q2’FY25 (INR Crore) | H1’FY25 (INR Crore) | YoY Growth (Q2) | YoY Growth (H1) |

|---|---|---|---|---|

| Operating Income | 624.5 | 1224 | 15% | 16% |

| Operating EBITDA | 153 | 305.3 | 5% | 4% |

| Adjusted EBITDA | 163.4 | 327.3 | 4% | 6% |

| Profit After Tax (PAT) | 90.9 | 181.7 | 8% | 8% |

| Adjusted Profit After Tax (PAT) | 96.7 | 195.2 | 5% | 9% |

Key Business Segment Performance

| Segment | Q2’FY25 YoY Growth | H1’FY25 YoY Growth |

|---|---|---|

| Cash Logistics | 15% | 16% |

| Managed Services & Technology Solutions | 6% | 5% |

Noteworthy Highlights

- The company secured new order wins worth INR 200 crore in Q2’FY25, resulting in a total of INR 400 crore for H1’FY25.

- CMS Info Systems received recognition for its financial strength and governance, being awarded “Best CFO 2024 - Medium Sized Enterprise.”

- The company actively participated in industry events and forums, showcasing its thought leadership, particularly in areas like cash management and financial inclusion.

- The sources highlight growth drivers for the mid-term, including increased formalization and consumption, greater outsourcing trends, and the introduction of new solutions like AIoT Remote Monitoring.

- They also indicate a projected revenue target of INR 2,500-2,700 crore for FY25, representing a potential 20% growth.

5 Likes

CMS Info Systems Limited Earnings Call Presentation for potential negative news:

-

Subdued Consumption Impact: The presentation notes that “subdued consumption in H1’FY25 affected realizations” in the Cash Logistics segment. This suggests that lower consumer spending negatively impacted revenue in that area.

-

Order Book Execution Delays: There were delays in executing the order book, particularly with PSU Banks, during the first half of the fiscal year. The delays were attributed to testing and integration issues. This could raise concerns about the company’s ability to convert its order book into revenue promptly.

-

EBITDA and PAT Margin Contraction: While both revenue and profit increased year-over-year, there was a contraction in both EBITDA and PAT margins. This could indicate increased costs or pricing pressure impacting profitability.

3 Likes

Key Pointers from CMS Infosystems Q2 FY25 Earnings Call

Financial Performance:

- Strong Overall Growth: Despite a slower-than-expected H1 FY25, the company achieved 16% revenue growth, reaching ₹1225 crore by the half-year mark. This signifies consistent momentum even with external challenges. Q2 FY25 consolidated revenue grew by 15% to ₹624 crore.

- Segmental Performance:

- Cash Logistics: Grew 8% YoY in Q2, reaching ₹390 crore, with an EBIT margin of 25%. This segment consistently contributes a significant portion of overall revenue and is expected to grow at 10-13% in the mid-term.

- Managed Services and Technology Solutions: Showcased strong growth of 28% YoY in Q2, reaching ₹264 crore. This was driven by new order wins, though margins were affected by product mix and delayed project executions.

- Profitability: While revenue growth was robust, profit growth was comparatively slower. Factors impacting profitability include:

- Delayed Order Execution: This led to incurring costs without corresponding revenue recognition, especially in the Managed Services segment.

- Investment in Growth Initiatives: The company invested in capacity expansion, new business incubations, and talent acquisition, impacting short-term profitability.

- Product Mix: In Managed Services, the higher contribution of product revenue, which typically has lower margins, impacted the segment’s profitability.

- Working Capital: An increase in trade receivables, particularly ₹175 crore related to delayed payments for a key project, impacted working capital in H1 FY25.

Challenges and Opportunities:

- External Headwinds: H1 FY25 was impacted by external challenges like extended monsoons, an election cycle, and muted consumption, impacting both revenue and realizations.

- Order Execution Delays: Primarily due to technical integration issues with PSU banks, impacted revenue recognition and capital expenditure plans.

- Competitive Intensity: Though moderating, competitive pressures persist, particularly in the BLA sector, impacting pricing and margins.

Growth Drivers and Outlook:

- Order Book Execution: The company is intensely focused on executing its robust order book, expecting a strong Q4 FY25, laying a solid foundation for FY26.

- New Business Initiatives: Investments in new areas like IoT RMS and the bullion logistics business are showing promising results, offering potential for future growth and diversification.

- M&A Strategy: The company has a strong pipeline of potential M&A deals, focusing on expanding its offerings, scaling existing businesses, and consolidating core sectors.

- Favorable Regulatory Developments: Potential ATM interchange rate increases, PSU bank outsourcing trends, and RBI’s plans for currency chest infrastructure revamp are viewed as potential mid-term growth drivers.

- H2 FY25 Outlook: The management expressed optimism about the second half of the year, citing encouraging early festive season data, government focus on capital expenditure, and easing bank liquidity. They aim for an H2 performance better than H1 and a strong base for FY26.

Key Management Commentary:

- The company remains committed to its strategic priorities of driving revenue growth, market share gain, and margin growth.

- They are focused on investments for capacity addition, growth incubations, and M&A.

- Emphasis on improving customer satisfaction and strengthening the customer value proposition.

- The cash logistics business is expected to maintain a steady growth trajectory, with potential for 10% growth over the next five years.

- Despite challenges, the management remains confident in achieving the midpoint of their FY25 revenue guidance range (₹2500-2700 crore).

6 Likes

There has been a decrease in the number of ATMs in the country over the previous 12 months. It reduced from 219,000 to 215,000 in this period.

What is the impact on CMS?

3 Likes

If branches continue to decrease there may be negative impact. Reduced density. Reduced service points.

However, this may be temporary blip as increased compliance ATMs are being set up.

And, in the same article, it is stated banks are likely to open 2 ATM per branch. Have heard that before in CMS or some bank concalls (do not remember where). Number of bank branches today multiplied by 2 will take number above 219000/215000.

And, some banks like HDFC Bank continue to open branches.

Biased. Invested.

However, this line of business is in matured state. It is not going to grow exponentially and management has stated that as well. They are comfortable with 10-12% revenue growth for this line of business.

8 Likes

Average results from CMS Info. Flat topline growth, 7% bottom line growth. In the last con call, they had mentioned they had recognized costs for some work, without corresponding revenue. In all probability, net of that bottom line would have de-grown.

Couple of things to understand from the con call -

-

Will they hit 2600 Cr FY25 topline target they had given? Looks highly unlikely - it will need ~830 Cr revenue in Q4, ~30% Y-o-Y growth. Given the industry dynamics, highly unlikely.

-

How is the competition shaping up? After Hitachi bought Writers cash logistics business, not sure if CMS is finding it difficult to maintain/expand market share.

Disc- invested.

5 Likes

Was not aware of Hitachi’s entry

I did notice Hitachi Cash Logistic Van near my home area ATM in Bangalore.

1 Like

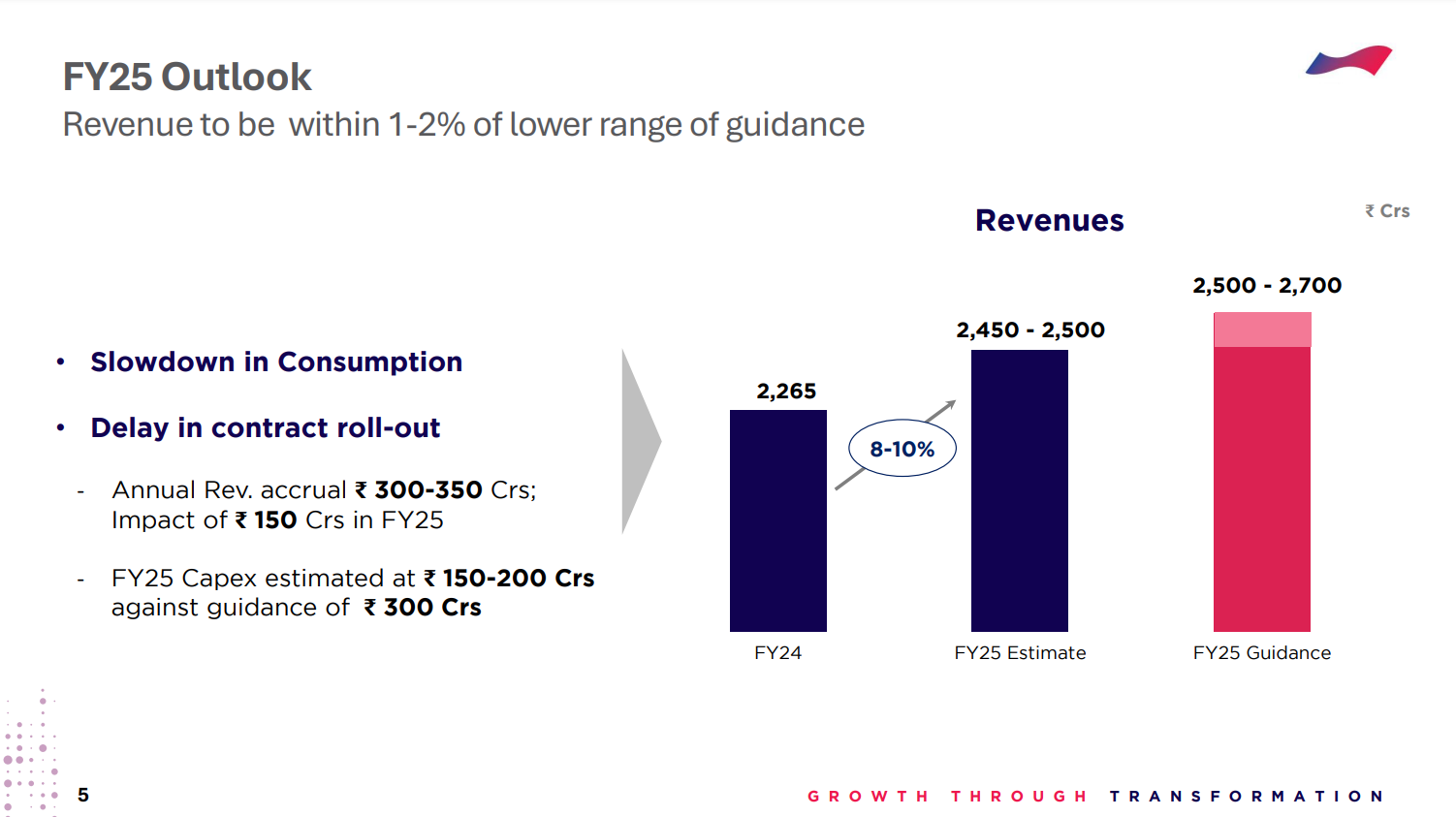

The answer to your first question is right here. If we take the lower estimate of 2450 as the total rev for the year, the yoy growth next quarter would be (±) 3%.

This means there is significant slowdown through the year. In Q1, they talked about hitting higher end of the guidance, 2700 Cr. In Q2, talked about hitting the mid-range, 2600 Cr. Now potentially they may not even hit the bottom end of the range.

They have given some reason for slowdown in investor presentation. Most of them are not in their control. Therefore, when they mention FY25 being a year of consolidation and setting stage for a strong FY26, the question is - which of these causes they mentioned for slowdown will change. This is what I would try to understand from Q3 con call.

Managed Services business, which was growing nicely did not grow in Q3. Another area to dig and find out.

2 Likes

slowdown in their cash logistics business could be understood but I assumed their managed services and tech solutions business to have a steady growth. degrowth over there is concerning.

1 Like

In the con call management explained the reason for slowdown in the managed services business. Primarily dependency on the clients and priority changes at the client as one of the major cash management players in the market is having challenges.

Right in the beginning of the call, Rajiv Kaul accepted that FY24 started with a lot of bullishness, but they faced a lot of challenges during the year. Medium term growth projection now is 14-17% (reduced from ~18% earlier, certainly competition is picking up) and they would come back with more detailed updates in their investor day in May/June.

For now I continue to hold as valuation is reasonable, good management that continues to explore new avenues of growth. If I find a better bet, may switch any time.

5 Likes

Now that AGS is out of business can we see potential re rating in CMS since around 12% of the market is up for grabs