As per screener, in Paytm, promoter has zero holding !

Other few examples of companies having zero promoters holding are -

2 Likes

If you see the list, i am comfortable holding large firms with zero promotor holding since any issues at these firms will impact so many ppl, that even govt will step in to stop it from going to zero; case in point back in 2009 when Satyam Fiasco unfolded, govt made sure the firm survived albeit with new management of Mahindras. The same can not be said of all the new age firms with less history and resources employed.

As for Paytm, even if the official records show Promotor holding as nill; we all know VSS has much more than just the skin in this firm… One way to look at this is how much of the Top Honchos personnel wealth is tied to the stock.

1 Like

IMO, they should have given more clarity in this regard.

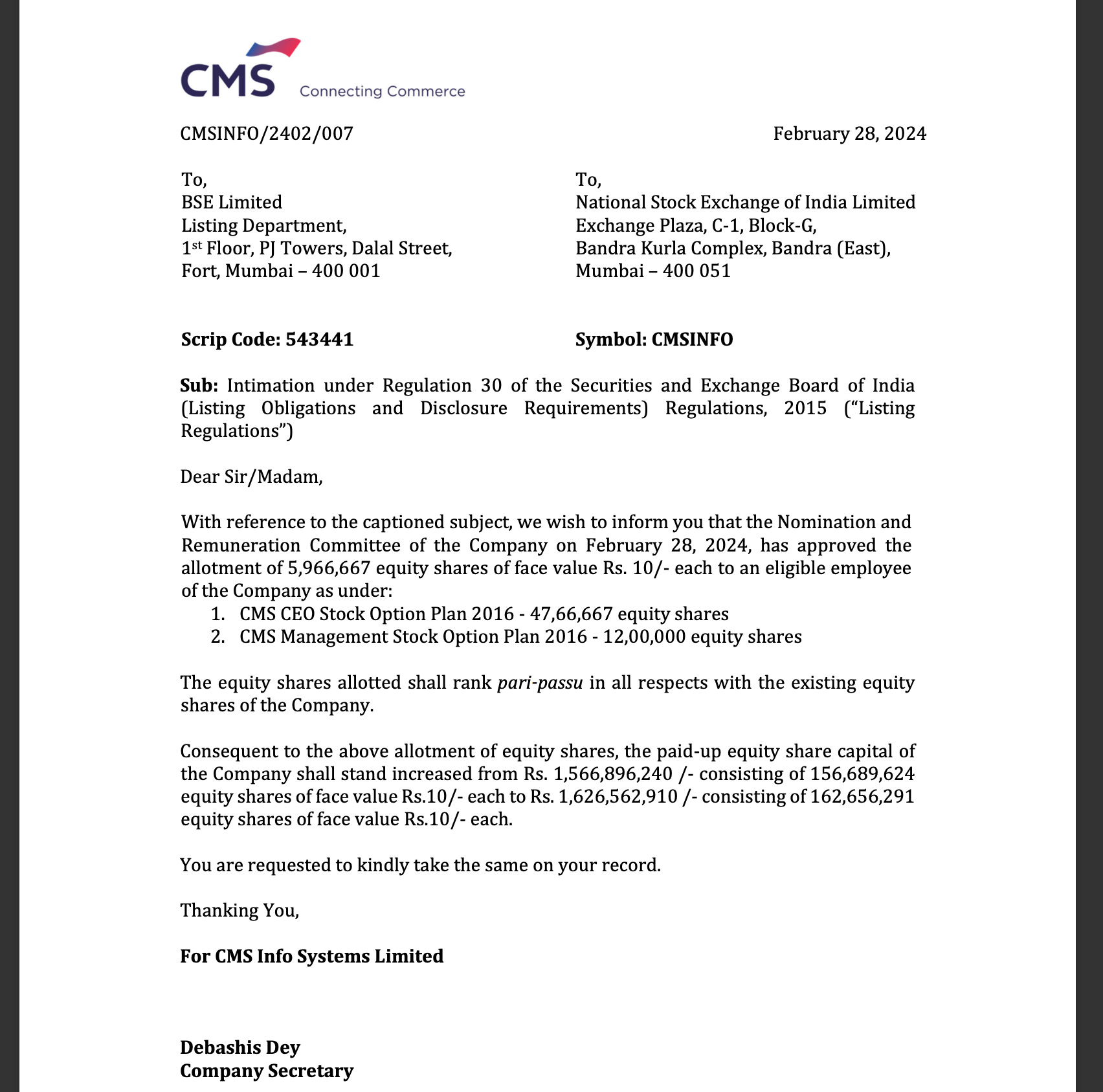

As of today, he has 1.01 Cr shares, which means he bought another 60 lakh shares. Of this, the shares allotted through ESOP is 48 lakh (must have been at some discount).

I have emailed the IR seeking clarity on this.

| # shares (crore) | % breakup | ||||

|---|---|---|---|---|---|

| 31-Dec-23 | 29-Feb-24 | 31-Dec-23 | 29-Feb-24 | ||

| Sion | 4.18 | - | 26.7% | 0.0% | |

| Rajiv Kaul | 0.41 | 1.01 | 2.6% | 6.2% | |

| Others | 11.08 | 15.26 | 70.7% | 93.8% | |

| 15.67 | 16.27 | 100% | 100% |

Link

Disc: Invested in family & Client accounts. SEBI-registered.

6 Likes

An older article from Dec 2023 ( posting just for reference)

2 Likes

Rajiv kaul increased stake via esop.

https://twitter.com/Nigel__DSouza/status/1764532141906391471?t=mAGMOD60TDTALAt77egkDQ&s=19

2 Likes

CMS has added some marquee investors when Sion exited.

| Name | Avg. Price | Quantity |

|---|---|---|

| NORGES BANK ON ACCOUNT OF THE GOVERNMENT PENSION FUND GLOBAL | 386.33 | 21,84,806 |

| ELIMATH ADVISORS PRIVATE LIMITED | 378.82 | 8,50,000 |

| MORGAN STANLEY ASIA SINGAPORE PTE | 370.05 | 8,69,145 |

| IIFL SECURITIES LIMITED ERROR ACCOUNT | 370.05 | 12,16,050 |

| MATHEW CYRIAC | 370.67 | 12,82,000 |

| SANATAN FINANCIAL ADVISORY SERVICES PRIVATE LIMITED | 375.50 | 10,00,000 |

| THINK INDIA OPPORTUNITIES MASTER FUND LP | 370.05 | 13,81,667 |

| WF ASIAN RECONNAISSANCE FUND LTD | 370.05 | 26,25,167 |

| INDIA ACORN ICAV | 370.05 | 10,39,700 |

| ABU DHABI INVESTMENT AUTHORITY - WAY | 370.05 | 8,46,560 |

| NOMURA FUNDS IRELAND PUBLIC LTD COINDIA EQUITY FUND | 370.05 | 43,10,617 |

| AIG GLOBAL INVESTMENT CORPORATION (ASIA) A/C AIG GLOBAL FUNDS-AIG INDIA EQ | 370.05 | 12,50,000 |

| ICICI PRUDENTIAL MUTUAL FUND | 370.05 | 15,00,000 |

| ICICI PRUDENTIAL MUTUAL FUND | 370.05 | 12,16,947 |

| ICICI PRUDENTIAL MUTUAL FUND | 370.05 | 9,46,514 |

| ICICI PRUDENTIAL MUTUAL FUND | 370.05 | 19,47,116 |

| KOTAK MAHINDRA MUTUAL FUND A/C - KOTAK SMALL CAP FUND | 370.05 | 36,25,712 |

| GRAVITON RESEARCH CAPITAL LLP | 385.99 | 8,36,705 |

| SOCIETE GENERALE | 370.05 | 7,90,833 |

However, the stock has limited visibility amongst the broader analyst community. The presence of such investors which should hopefully improve visibility in the coming quarters.

5 Likes

Hi All, Quick question:

Securitrans India Pvt. Ltd., a wholly owned subsidiary of CMS Info Systems Limited received GST Tax order confirming original demand of Service tax pertaining to the period of October 2016 to March 2017 and April to June 2017 and imposing penalty.

Since it mentions original order for a dated period, i don’t think this should lead to any impairment now or in future. Obviously the firm will contest but even if it looses, still there should not be any impairments; the amount (19.33Cr) would have already been set asides in the books, right?

Some additional, useful PR

business-india-cms.pdf (394.5 KB)

6 Likes

2 new service lines are being incubated with marquee customers. Along with the card business, these can contribute to growing topline.

7 Likes

A couple of things that are concerning to me that I could not understand:

- Receivables have been growing up very rapidly: ~Rs 600Cr (by Sep 2023) vs Rs 450 Cr (March 2023). For a ~ Rs 1600 cr book value that is 40%. Why is this?

- Why does the company have such high bad receivables (see screenshot)? Doesn’t the company get paid by banks? Is this because money gets stolen in transit?

Can someone provide some insights here?

1 Like

How do you read receivables as 600 crores and 450 crores in September and March 2023? Numbers are in millions, not in cores.

I did not attach a screenshot for receivables. Here is one from the annual report.

Net Receivables were 500Cr on march 2022, 526Cr on march 2023 and 604Cr on Sep 2023

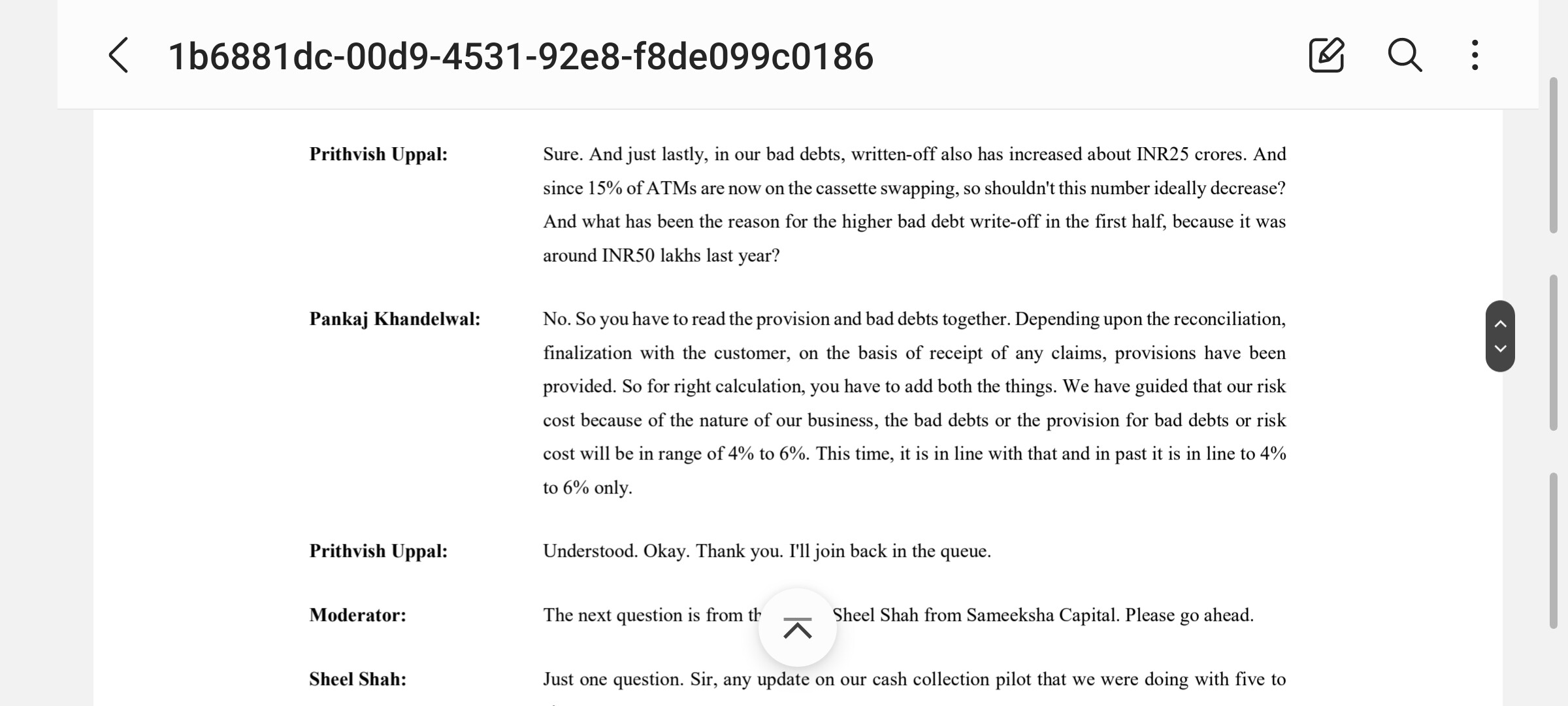

The company allocated 93Cr provision for loss from receivables in 2022 and 132 Cr in 2023

1 Like

Good point. Worth asking in the concall

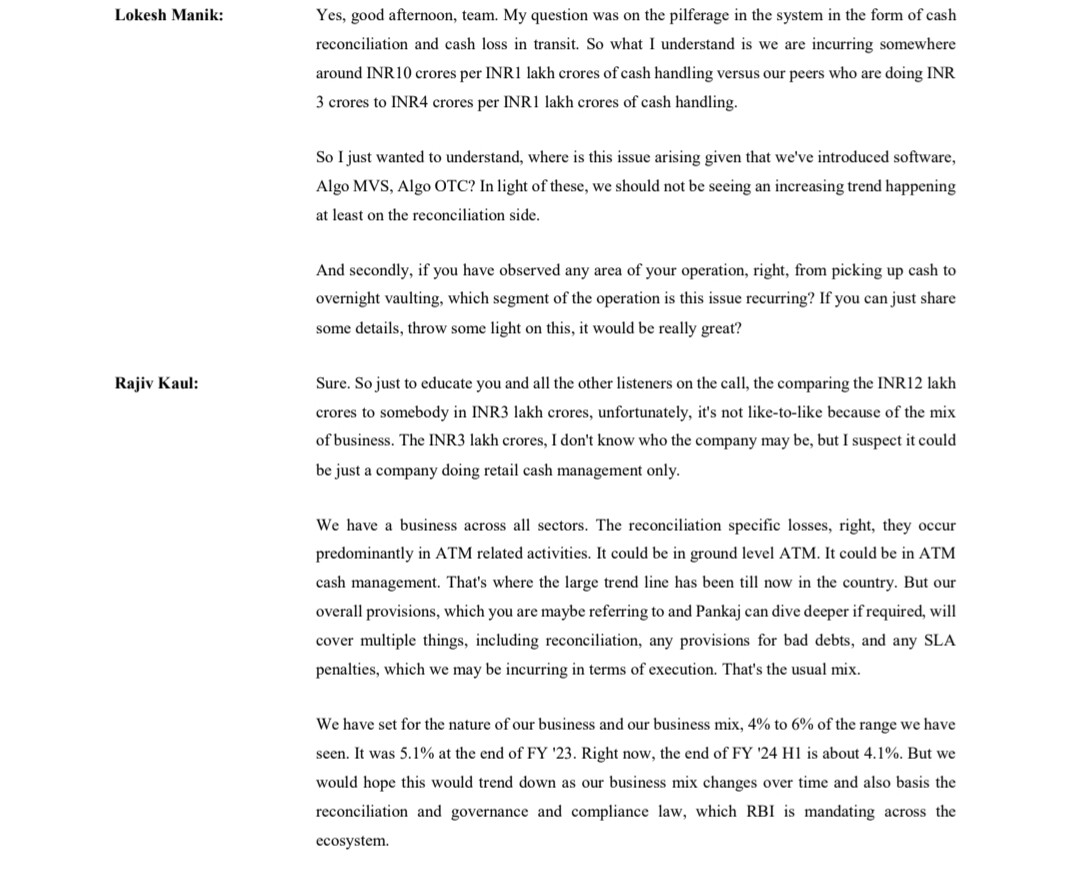

Thanks @Debojit_Kangsa_Banik - its clear the write off due to pilferage in cash movement.

What is your sense of the receivables? Is there a comparable with any other company?

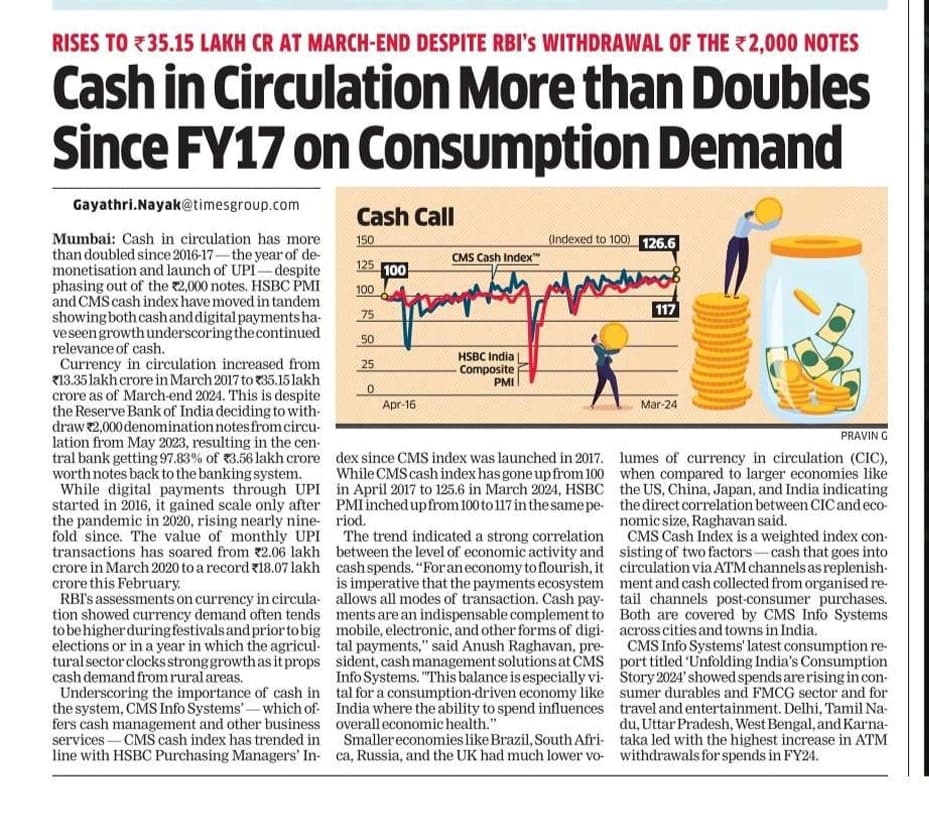

I am currently studying CMS Infosystems. Good to see this thread on Valuepickr. The answers that the management gives to the question concerning threats to their Business Model i.e., the Impact of a higher adoption rate of digital currency/UPI are listed below:

- First of all, the Cash Logistic Business is a B2B business and their revenue model is not directly correlated to the volume of ATM Transactions, rather their revenues are directly correlated to the no. of touchpoints.

- It is in the business plan of Banks to add more and more branches to enhance their physical distribution (to improve CASA & Loan growth). Historically, for every branch, 2 ATMS are being added. So, an increase in ATMs will increase CMS’s Cash logistic business.

- To put down the growth in no. of ATMs, in 2021, there were around 225,000 ATMs & it is projected to grow at 6.5% to 365,000 ATMs by 2027. One more data point that they mentioned in one of their Investor meet was that currently 60% of ATMs are being outsourced by banks, rest 40% are managed by Banks, themselves. This split was 50%-%50% between self-maintained & Outsourced a year back. They said that banks are trying to focus primarily on their core business and outsourcing other things. This 40% ratio will even drop further and thus will increase the market size.

- The future market size of the Cash logistics business (FY 2027) is projected to be 8000 Cr. Considering their 45% odd market share, this creates a turnover of Rs. 3600 Cr from the cash logistics business alone from Rs. 1300 Cr in FY 2023. This will be a growth of 29% CAGR.

- Furthur, they said that RBI had issued a circular/data, wherein it stated that Cash and digital currency will co-exist in the future. As a testimony to it, they said in one state of the USA, a law has been passed for the vendors not to refuse payment in cash, signifying the co-existence of both modes of currencies

These were some answers that management gave to the question of the future of the cash logistics business. Another thing that I have seen from my personal experience is that even though I am going the majority time for cashless transactions, i.e., using UPI for small payments for Auto, Cabs, Grocery, Street Foods, etc., these recipients (vendors) do not use UPI for making their payments or in their their expenditure. Rather, what they do is, withdraw cash from their account and use it in their discretionary spending. So, what trend is becoming evident is that earlier, people like you and me used to transact in cash with such vendors for our discretionary spending by withdrawing surplus from our banks (Which means we used to do activity in ATM), v/s now, people like you and me pay through UPI for Discretionary Spending and these vendors are getting money in their bank so they go to ATM to withdraw money from ATM.

The management also said that even after the UPI Transactions touched new highs in our country, but the ATM transactions have remained steady at similar levels. This means that the Set of People using ATM Services is changing but not the level of activity. Although I don’t have the numbers to back this analogy, I do get some conviction after thinking in this way. Any Logical arguments will be positively accepted.

Their AIoT Business & Managed Services business are growing at a good pace their share of revenue to total revenue is also increasing. I believe the biggest moat that this company has is its DISTRIBUTION NETWORK. The pace at which they are growing their newly launched AIoT Business (from 0 to 400-500 Crs in 3 years) is backed by their distribution strength. Leveraging their distribution, they can build a large business from here on.

The other side of me also acknowledges the fact that the management is also looking to diversify from the cash logistics business and reduce revenue share from this segment. They too acknowledge the risk of digital currency in their Annual Report & DRHP.

In a news article shared on VP & other public platforms, I read that they are piloting Gold Logistics & related services also. I couldn’t find any official news for this. If anyone has anything on this part, please share.

Disclosure: I started Studying recently. Not invested currently.

13 Likes

Cash is here to stay in India, irrespective of what ever the advanced digital we go. We don’t data points to prove it . I will give you a layman perspective.

I purchased a land in Hyd 6 months back. The price of the land was Rs 75 lakh but it was registered only for $35 Lakhs. We had paid balance of 40 Lakhs in cash. This kind of situation is not going to change in India. India still accounts for large number of black money transactions and cash is always a king.

Invested at current level and I’m a long term investor.

5 Likes

The results are in and as expected we are looking at a solid QoQ growth and an equally solid YoY.

The ebitda is up 16.6% YoY, consistent PAT margin at 16% YoY, QoQ Revenue stood at whooping 25% and YoY at 18.3%.

Coming on segment wise the tech solution business seems to be the growth engine here with 35% YoY growth in revenue.

Biggest YoY growth in revenue segment wise came from card services at 47.4% YoY followed by ATM managed services at 30.2% on the flip side the cash mgmt services grew at 11.1% YoY. Looks like the company is now changing its focus from a atm management business to a more actively managed software and tech business.

Can anyone here point out how much of the company’s tech related business overlaps with what large cap tech giants like TCS, Infosys provides to Indian banks or is it completely different?

4 Likes