I found a post by India Independent Insight on CMS. I couldn’t find any irregularities while studying this business. Management responded to queries about unbilled revenues on the recent concall. Has anyone come across a clue about aggressive revenue recognition / revenue overstatement as indicated in the table of content of this III report?

1 Like

2 Likes

Technology is the edge for such company. Will resignation of CTO have any negative impact on CMS Info System ?

He joined CMS Info System before three years from Adiya Birla Group (CMS Info Systems on LinkedIn: #cashmanagement #technology #cto) …during these three years, innovation was the key driver at CMS info

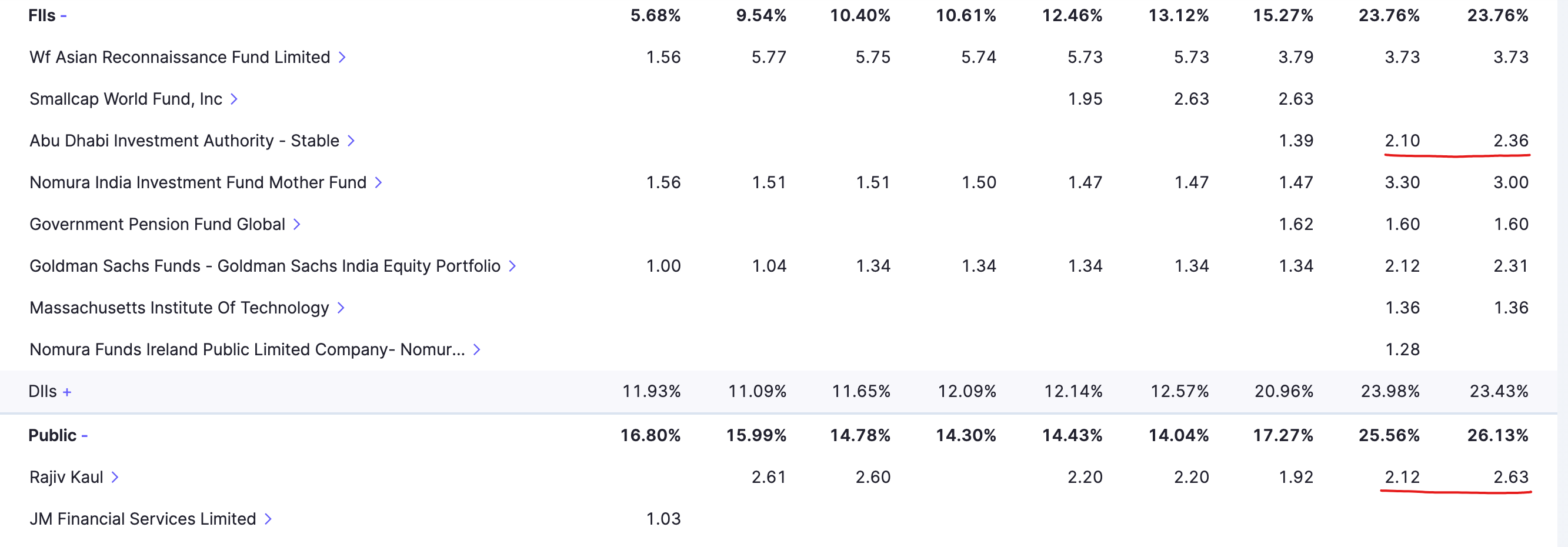

Noting some key trades from Dec qtr

- Vivek Kaul (CEO) has increased his shareholding by .5%.

- Abu Dhabi Investment Authority’s SH up by .26%

- ICICI MF decreased by 2.05%

ICICI MF SALE - 483E74A6_29A4_41B8_A04A_5DE4DA803B3D_110353.pdf (bseindia.com)

Disclaimer: SEBI Registered. Invested in family and client accounts. Views biased

2 Likes

I am closely tracking this company, some good MFs (PPFAS, SBI) also invested and have decent allocation, still not figuring out why the market is not giving value to this company,although Promoter as well as Financials are very good.

One concern that i think is - Trend of increasing UPI(Govt Push as well).

Disc - Not invested but tracking like a hawk eye for Price Volume actions.

1 Like

Just add on, recently CMS published this article on 3rd Jan 2024:

Key points:

- CMS Info Systems analyzed 11 consumer-facing sectors in organized retail for H1 FY24.

- Retail consumption in B2C sectors saw a robust annual increase of 9.3% in the key 11 sectors during April–September 2023.

- FMCG and e-commerce sectors experienced significant annual growth of 26.2% and 19.4%, respectively, in Q2-FY24.

- Aviation and Hospitality sectors witnessed annual growth of 29.7% and 12.8% in Q2-FY24, driven by events like the Cricket World Cup.

- The jewelry sector rebounded with an annual growth of 7.1%, recovering from a 4.6% decline in Q2-FY23, possibly due to increased spending during the wedding season.

- The large format retail sector saw an annual increase of 7.8% in Q2-FY24, influenced by rising incomes, urbanization, and changing consumer preferences.

- SURU (semi-urban and rural) outpaced metro cities in consumption growth, with the fastest growth of 9.2% YoY in H1 FY24.

- CMS Cash Index™ (CCI) is highlighted as a powerful indicator, showing a surge in retail consumption parallel to the 7.6% GDP growth in Q2-FY24.

- Expectations of stronger consumption growth in Q3-FY24, especially in FMCG, e-commerce, and aviation sectors, supported by macroeconomic indicators.

3 Likes

Check Brink’s. It is a global player with operations in 50 countries and one of largest US players. It is valued at just 3.5 B USD. CMS is India only play and already valued at 0.7 B USD.

1 Like

I see as an opportunity. Other players with poor financials will choke and CMS might be able to grab that opportunity and increase market share.

Let’s wait and watch.

Also CMS is moving towards digital solutions.

2 Likes

I don’t know why the market is not giving valuation to this company.

Pros-

Good Mgmt,

Leader in their sector,

Back to back good results(slight dip in margins in Q3)

Cons-

Increasing cashless system in the economy

UPI trend increasing.

Anybody who is tracking this company can elaborate why the market is not giving value to this company?

2 Likes

Listing down some quick pointers

- Anecdotal thinking: Cash vs UPI. Cash may eventually decline, but it still is salient in T2/3/4 and low-mid income strata. Cash in circulation is showing no signs of degrowth. Even after withdrawal of high denom. Rs. 2000 notes, CIC has grown by 4%! The volume of ATM withdrawals is growing too, albeit at a slower pace than pre-covid. CMS’ business model is anyway not dependent on volumes of cash handled. If cash in the system declines, the velocity might increase and counter-intuitively offer more business to CMS. Their pricing model is per-trip/visit based.

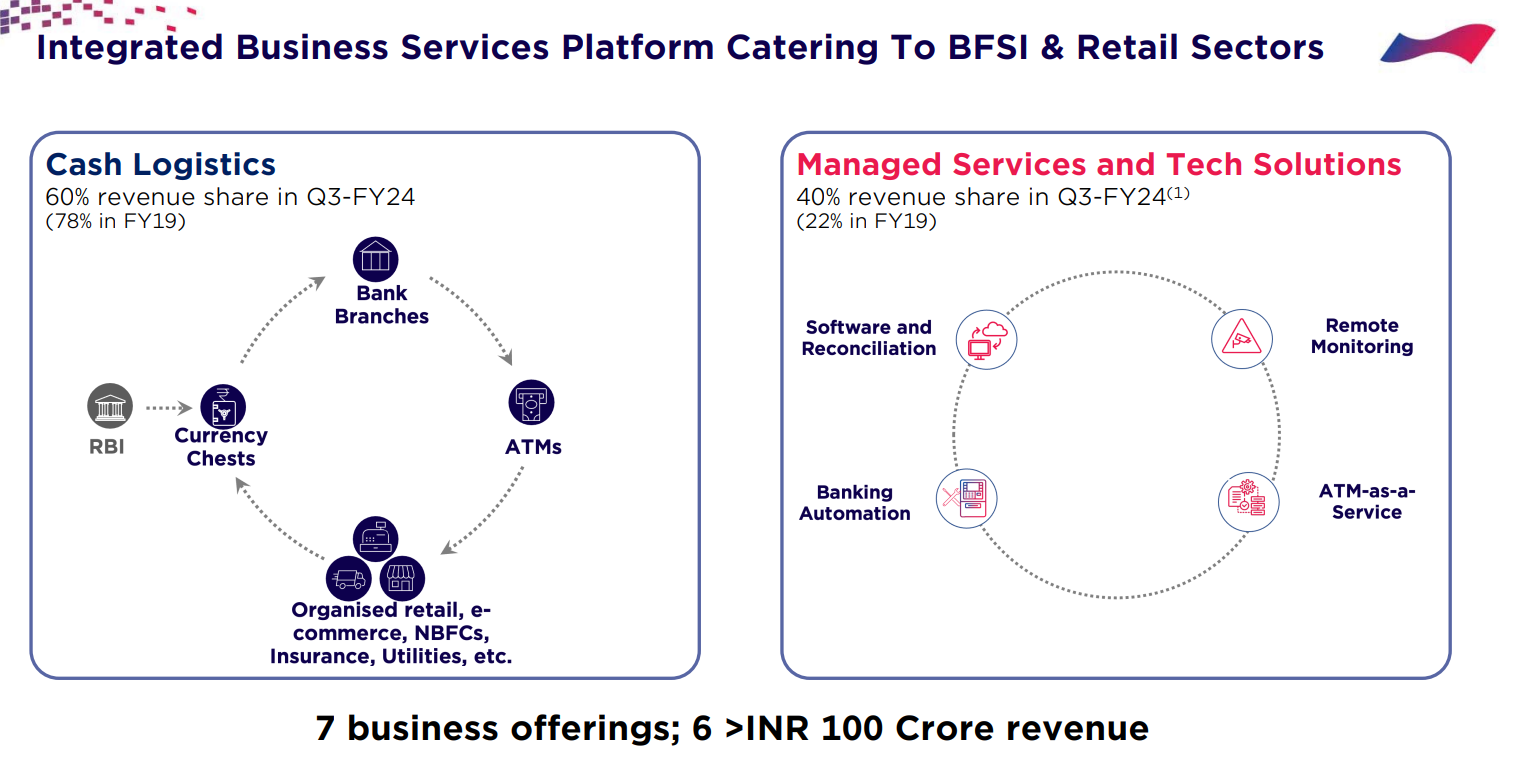

- My hypothesis, with limited evidence: the Market sees this as a pure cash logistics company. IMO, its a B2B Business services firm with declining dependence on cash mgmt (managed services now form 40%). Moreover, formalization of retail serves a long runway for growth in cash mgmt business. Some evidence is seen in their healthy return metrics. A pure logistics company may not enjoy such healthy return ratios without a strong tailwind.

- Headwinds: ATM additions may not pan out as projected/anticipated by the market in 2020-21. Some concerns related to the banking sector growth.

Do read their investor day presentation and concall. I’m sure you’ll find more reasons, e.g. binary thinking, consolidating industry, UPI growth post covid, poor financials of most peers etc.

Disclaimer: SEBI-registered. This is not an investment advice. Holding significant quantities in family + client accounts.

8 Likes

See there may be two possible reasons for this : 1) Promoter PE Firm has been selling its stake time and again as they will be completely exiting due to fulfillment of their investment objective. This has affected investor sentiment and increased supply time & again. 2) Due to digital push of the government, many investors are not keen.

Having said that, I think this is a very good company which will become a major banking technology services provider. The first concern is short term and second concern will have not impact due to huge indian cash market and company increasing focus on tech solutions to banks.

Dis : Made good returns and still invested.

3 Likes

I think that the banks will not have to refill the ATMs as frequently if cash withdrawn declines. Banks shouldn’t really reduce the cash they put in an ATM. Also, the value of ATMs to a bank will decline if their end customers aren’t using them as often.

Their managed services are also centered around ATMs. I am not doubting growth for coming 1 or 2 years as they have yet to gain the market share of ATMs under their surveillance.

The low valuations of this company are possibly due to low terminal value.

disc: Not invested, yet.

3 Likes

CMS publishes their CMS cash index report each year.

- Cash is still king and growing.

- Cash withdrawal through UPI is also coming up across ATMs.

- Fun fact, cash withdrawal was highest in Karnataka in 2023, which is so highly unlikely given Bangalore being its capital.

- My native is a town, although there are QR available in shops, but I can see people still don’t use it as such. People still rely mostly on cash. I have done this scuttlebutt in many such shops in my town.

- I am quite convinced, cash isn’t going anywhere , atleast next 5 years we are good.

Disc: Totally biased, no recommendations, holding in my top 10.

3 Likes

Poor result from Radiant Cash

8% revenue growth YOY compared to, eps degrowth 33%. YOY.

2 Likes

thanks for this image. Out of the 4 offering in “Managed Services”, please can share which once has more revenue? Which one can grow faster? How to get this information.

Thanks,

Harsha

2 Likes

Now promoter’s holding = zero

Complete sell at 370.05 per share through bulk deals

Buyers are

I think now company is purely professionally managed company. Having good people on board and execution will decide growth of the company!

3 Likes

Yeah this was about to happen, already it was mentioned in concall

Rajiv Kaul increasing stake in Dec 23 itself shows strength in company

Disc: holding n biased

1 Like

I have a slitghly different view on Zero Promotor holding and Professionals only running the firm. I feel with less skin in the game, during bad times, these professionals will start jumping the ship or go for other greener pastures. Is their enough ESOP to ensure that they fight it out when things are down for the company. Imagine if Paytm has Zero Promotor holding today, will it stand any chance to survive against the regulator onslaught!!

Also we would need to monitor the professionals don’t end up giving too much ESOPs to themselves, diluting the other shareholders…

Is the stake increase of Rajiv Kaul happening through ESOPs or market purchase.

Though in this regards i do appreciate the current ESOP policy of CMS Infosystem; hope it stays this ways…

2 Likes