How come employee cost reduced so significantly?

how come employee cost reduced so significantly?

Assuming, Lesser bonus might be given this year compared with last year. Provident funds and other expenses are on the rising side and it confirms, there haven’t done any job cut.

In annual report itself check remuneration given to KMP. Last year it was 322.55 mn and this year it’s reduced to 187.44 mn. Executive director’s performance bonus is reduced to 4% from 10% computed on net PBT. And employee salary increase it to the tune of 10% on an average… (As per Annexure VIII of annual report)

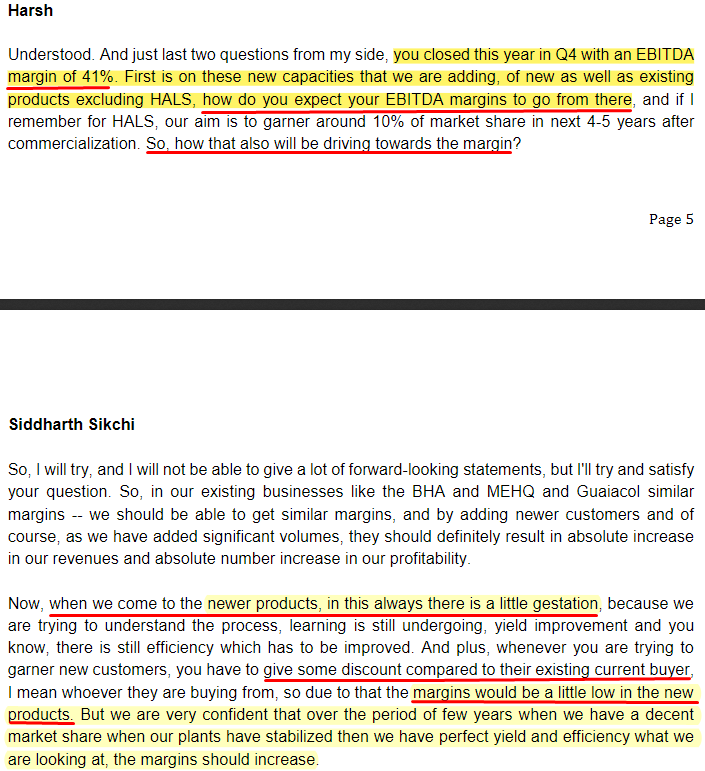

OPM is clearly expected to be at around 30%-40% as per the management.

Please also read concall Q1’22, where management explained that it takes around 3 years for proper product understanding.

Though I am not sure of what margins company would do, my understanding is that it will be a cocktail of increasing capacity of existing products as well as reduced margin in new products.

The management would try to strike a balance between Margin and Sales, but I am sure their tilt would be more toward growing Sales rather than maintaining very high Margins. So I would go with the views of @nityanandparab .

With Vinati entering the MEHQ and Guaiacol space wonder what impact it will have on margins going forward?

In my opinion, good, steady & predictable topline growth in Q1 results declared an hour ago.

RM cost pressure has increased further resulting in net profit below 30%. This needs to be waited out for how many every quarters it takes.

Hope the capex is also moving as per plan. We would get more details in the con call

As mentioned in my earlier post, the change in product mix, particularly new ones is resulting in erosion of OPM

It is of particular concern that Vinati Organics is entering in to MEHQ, Guaicol chain as a backward integration move as @AJain pointed out.

Since Vinati is world leading produce of ATBS. It is natural for Clean Sciences to ensure that MEHQ -BHA chain which comprises 60% of revenue is protected.

Has the product mix changed already in Q1 sales numbers? I thought they are yet to start production for new products (HALS etc) and this margin erosion is still primarily due to core RM inflation. Almost all companies have reported lower margins on a QoQ basis.

Also about MEHQ & Quaiacol, even though Vinati or any other company plans to add capex, there seems to be good market for that. Clean Science just increased capacity for those two products in unit 3 by 50%.

All said and done, one needs to tread cautiously when investing in companies that trade at such nose bleed valuations. This is an extremely unforgiving market and one average quarter or unfavorable news cycle (inflation, recession, RM price spike) is enough for a price beatdown citing unreasonable valuation of the stock.

Disc: currently not invested

As per Q3FY22 Concall the company has launched 2 new products TBHQ and PBQ in production(mentioned in presentation Q1FY23 as well). HAL’s production is expected from Q2FY23.

There was 4% increase in RM costs in Q1FY23. There could be 2 reasons i.e. product mix or Raw material cost increase. I remember Phenol being 50% of RM costs in Q4FY22 and Phenols price reduced by 7.4% in last 3 months

so it must be other 50% of RM used to make other products. So my logical conclusion is product mix might have changed (as mentioned in slide No. 5 Q1FY23) in favour of TBHQ and PBQ, where they will have to offer discounts to increase market share.

Anyway I would like to hear from the Management itself.

CSTL increased MEHQ production by 50% for internal consumption to BHA. Vinati is a major customer for CSTL, and both being a world leader in their sector means both are interdependent. It is fair for Vinati to backward integrate to improve their margins but for CSTL it has to find buyers for their products to maintain their market leadership.

There is no doubt that new products will start with lower margins and improve over an year or two. The management had mentioned this in almost all the con calls. I was curious if sale of new products have already started in Q1 itself as the RM inflation was expected to increase higher in Q1 (Apr to Jun) due to Ukraine war and etc. Crude prices have started falling, so RM cost pressure should subside over the next few quarters, hence the important number that I am watching is topline and capex. As long as they are able to increase revenue regularly, they can get back to better margins (or absolute profits in worst case as long as revenue keeps increasing).

Competition is there for every company. So far they have done well and this is one area to keep watching regularly.

Notes from Q1FY23 Conf Call

a. 30-40% growth possible in FY23

b. Energy prices hike in Europe may help company to sell more products to Indian and export market

c. HALS plant to start by Dec-22 and as BASF is facing issues and they have increased the prices CSTL may able to take advantage of the same

d. Vinati has only announce for MEHQ addition. Actual production may take time and it will be premature to comment on the same

e. New products are contributing 15% of revenue

f. New products will have lower margin and as they scale it will add to the bottom line

g. They were able to ship the products to China during the Apr-May lockdown as well using the different routes

Observation- FY23 can easily cross 1000Cr revenue if this runrate continues.

@AJain all specialty chemical companies like Tatva Chintan, Aether, CSTL are trading at high PE. One optionality they have is using their R&D they can come with innovative processes and eat the market share. One has to be cautious but at the same time we cannot ignore them as opportunity size can get bigger with new product launches.

Tatva Chintan after IPO was hovering at 80PE and after one year the PE compressed to 50 after FY22 results as the company posted good results in FY22. Now PE has increased due to bad Q1FY23 but as they enter into new segments like Waste Management using the SDAs it will again expand their opportunity size. The electrolyte segment last year was only contributing 1% and in Q1FY23 it has increased to 8% albeit a lower base but point here is segment revenue is increasing.

You are missing inventory aspect. All cos increased inventory post supply chain issues because no one wanted a situation of lost sales. If the prices are dropping in Q1, the effect may be seen with a lag.

Important Notes from May 2023 concall:

a. FY’24 revenues will be largely from the existing product basket, plus HALS 770 and 701 (current capacity: 15,000 tons per annum)

b. FY’25 is when HALS will start to kick in and will ramp up over the next three years.

c. It will take some time to get new customers for HALS and start meaningful revenue.

d. They are also developing some new chemicals. Some of them are into performance chemical category. Some will go into water treatment chemicals; some in pharma and remedials.

e. These new products will start contributing from mid FY’25

As per my understanding things will start to get exciting from June, 2024. Till then, they are undergoing capex and adding new clients. But, market might start discounting these numbers in share price earlier.

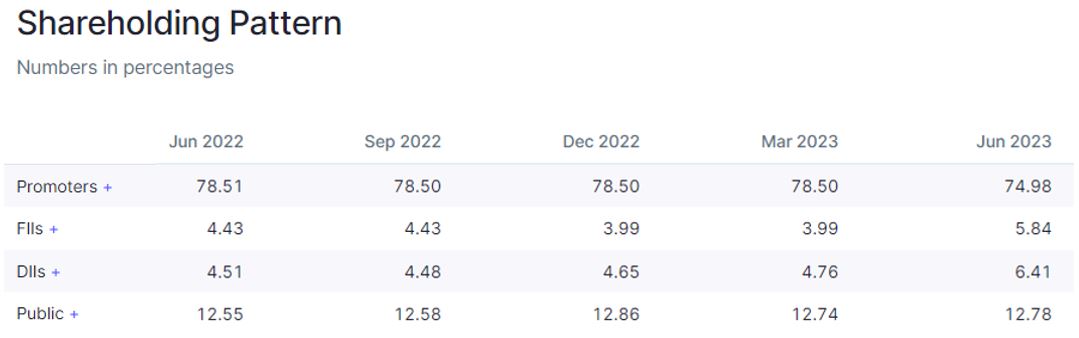

Isn’t the SEBI rule that promotor can’t hold more than 75% worrisome to investors? The real value of the stock can be manipulated if non promoter holding is so low!!!

It looks like promoters offloaded approx 3.5 % shares in May’23.

Yes, you are right. Promoters sold 3.5% in open market on 29th May. This is to meet SEBI rule of <75% holding by promoter.

Recent offload by promotors to meet the obligation of <75% holding had been absorbed by FII and DII. However there is an 0.04% increase by public.

Now the share price is at all-time low. This company is testing my patience as all other investments done very well in last 3-4 months. But I have decided to stick to basics and give the time needed for the company to perform.

Chemical stocks are in general going to test patience for another 2 to 3 quarters. One can remain invested in these stocks as they have potential to compound in long term, but than the broader market i.e other then chemical sector has already given return of 25 to 50% in last 3-4 months. If you have liquidity then there is no point liquidating your portfolio but if you are fully invested then call has to be taken on capital allocation.

Disclosure : Not holding but tracking for investment may be after 2 to 3 quarters.

Just like Tatva chintan, Clean science is another poster boy of a hot stock in a hot sector. Its IPO came precisely during chemical boom and at that time there were a lot of videos ennumerating the competitive advantages of the company. The main thing to observe here is that perceived competitive advantage of a company is of not much use if the sector itself is cyclical. In the heady days of chemical sector boom, a lot of learned people also forgot to take into account the cyclicality of the sector.

Even after a lot of correction in stock prices ( half levels to peak) and a lot of sideways movement, I find that current market cap of the company is nearly 14000 crores. Sales is less than 1000 crores as on date and net profit on an annual basis is less than 300 crores. Peak valuations were a PE of 138… And even after all this time, PE still remains above 40. At some point of time company needs to start delivering numbers, otherwise there can be downside from current levels too.

I have marked successively lower tops (bold solid red horizontal lines) and successive lower bottoms (marked in bold solid blue horizontal lines) on the charts… Typical lower top and lower bottom formation of a stock in a downtrend. Need to see when this cycle reverses.