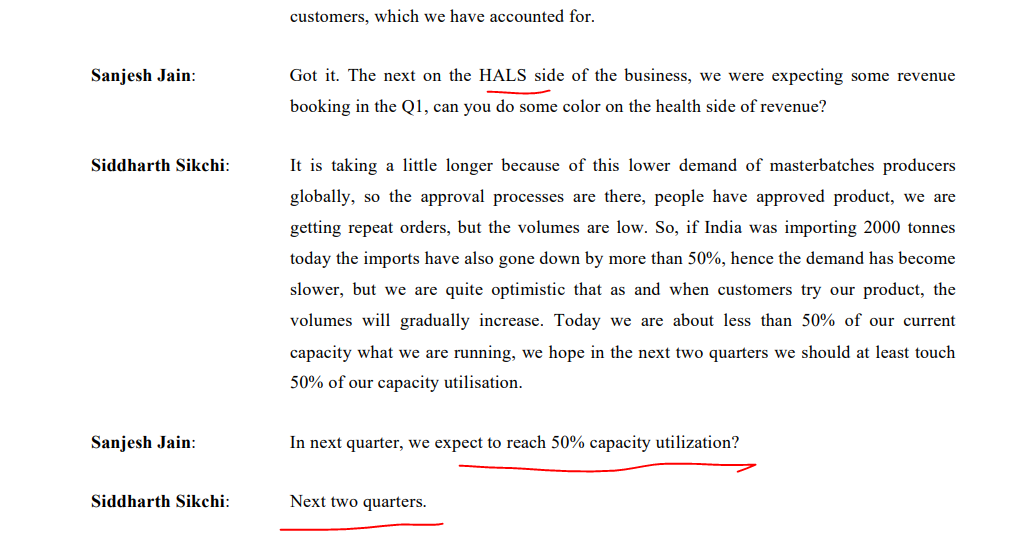

Does anyone know what is Qtrly revenue guidance for HALS for the 701 and 7710 that is expected to reach 50% utilization in next 2 Qtrs?

I understand there are more HALS products getting launched in December that is also targeting export market. any revenue guidance given for that?

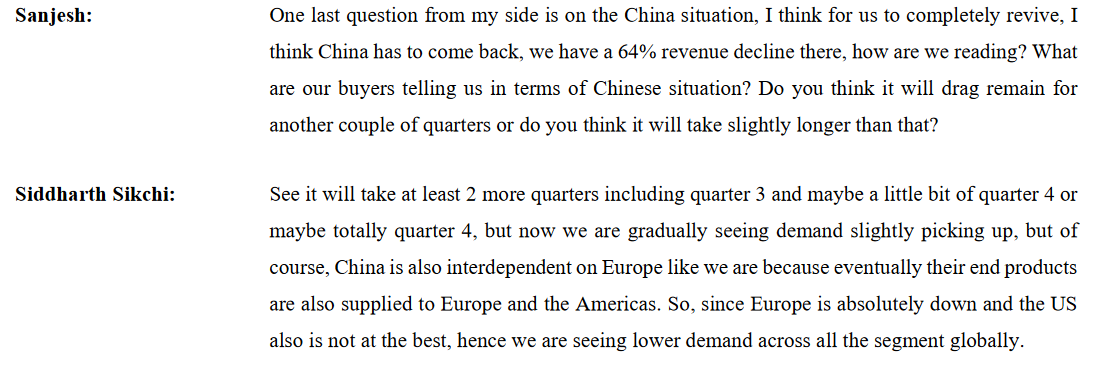

Deflation in China. Will it impact chemical industry in India ? If so someone explain it.

Main product of Clean science is MEHQ, Guiicol. While searching I found that another listed company name - Camlin FIne science also makes MEHQ, Guiicol & other specialty chemicals. Clean science is considered as catalyst maker so in simple terms, process to make MEHQ & Guiicol by clean science & this Camlin Fine science is different?

Does Clean science have a competitive cost advantage over such other makers?

Also just read that this Camlin fine science has temporarily stopped their Diphenol plant in Italy citing very poor demand & high RM pricing. Does this diphenol comes in picture in anyway for clean science ? If anyone has idea about it, can throw more light on it.

2 Likes

Clean science product MEHQ & other product by catalyst route with more clean process and claim to have much cost advantage over others.

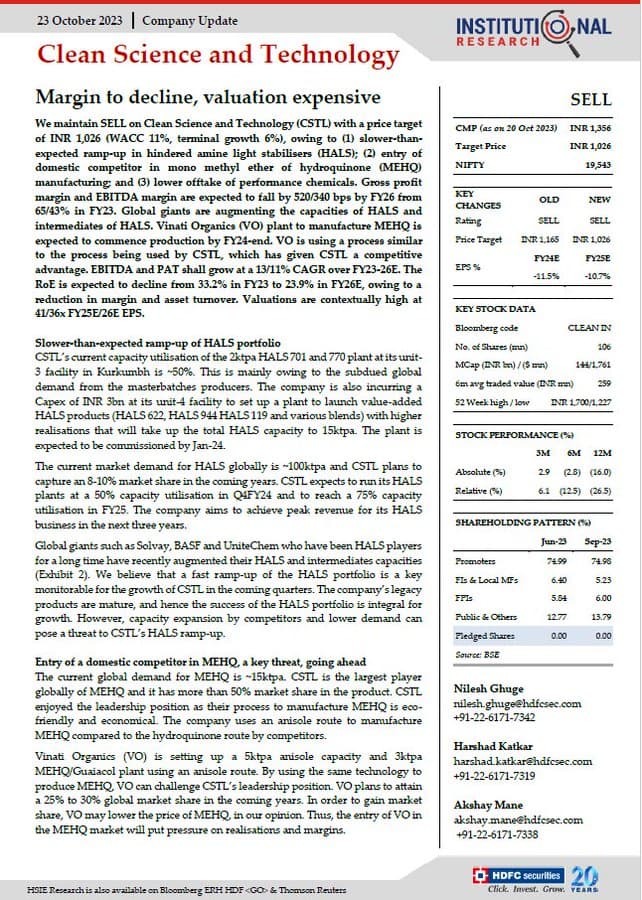

They are the largest manufacturer of the world (in terms of manufacturing capacities) and accounted for 55% of the global capacity. Other competitors in the industry include Solvay and Camlin Fine Science. they had got supply order from BASF for 3 years which they are trying from last 10 years

1 Like

If I recall correctly, they manufacture MEHQ via the vapor phase technology, which substantially improves their gross margin (~70%) vs other companies manufacturing the same product. This is one of the reason why they have cost leadership across MEHQ & its derivatives.

2 Likes

Clean Science and Technology acquired additional 11,70,572 shares in Clean Fine-Chem Limited, the company announced through an exchange filing. The company bought additional shares for a premium of Rs 588 aggregating to Rs 70,00,02,056 (70Cr).

CSTL subscribed to the additional equity shares as it is in process of setting up a manufacturing facility for its speciality chemical business. The additional capital will be used for funding its green field projects.

Corporate filing of the same

Discl: Not holding, tracking.

1 Like

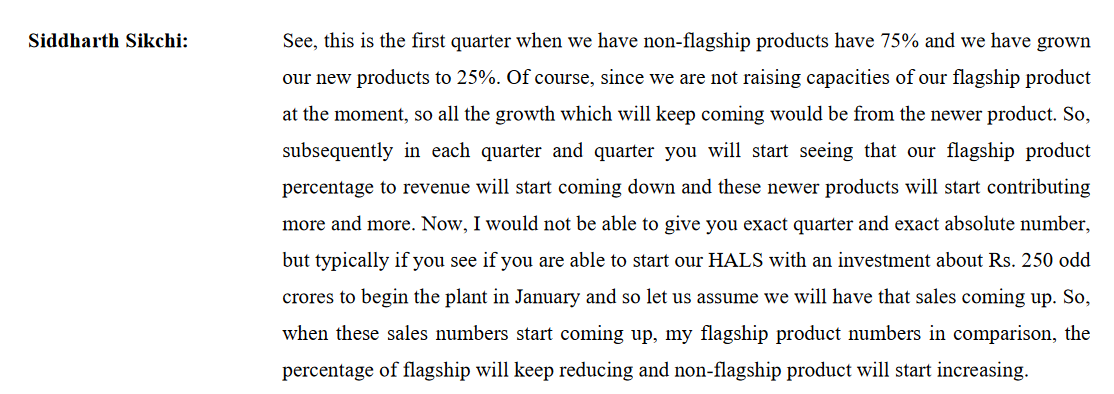

Does anyone did calculations that HALS series will contribute how much cr. revenue when completely rolled out in FY25 or FY26?

I just wanted to understand the recent 2 capex which they are doing 1) Increased MEHQ capacity by 50% & these HALS series will contribute how much in top line? Say FY23 they did 936cr. in topline, what can we expect by FY25 due to these 2 capex ?

Total capex for HALS in unit 3 and unit 4 - 2ktpa and 15 ktpa. Total 17ktpa. HALS price - 8$ to 10$. This can create revenue of 1000Cr to 1300Cr. But this will take time for realisation, let’s see how the execution will turn out

1 Like

How u came to figure of 1000cr.? Sorry for noob question.

10$ means 800rs. Take 15k capacity. That means 1.2 cr.

Also these 15ktpa capacity means per month capacity of 15k/12 ? or 15k/month capacity?

Yes I know it all depends on capacity utilization, demand, execution etc. but just wanted to know what can we expect in next 2-3 yrs. from HALS series.

Edit: Doubt got clarified after reading this. Thanks.

As of recent Concall updates, HALS currently is at the capacity of 2000 MTPA, and Clean Fino CAPEX will add another 15000 MTPA. So, the total capacity will go up to 17000 MTPA.

At average realization of $8-$10/Kg and with 100% capacity utilization, the figures reach upto: 17k * 8 * 1000 (for KGs) = $136 Mn i.e. 1110 Cr.

But, the chemical market has been in a bad phase for the past 6 months. So, either realization might not be up to the expectation or utilization will not be that higher. While HALS is an import substitute product and hence demand will not be a problem according to me, the issue is realizations. Will need to observe every quarter to make a conclusive decision.

Regards,

Not Invested

2 Likes

It is kilo ton per annum. Kilo (10^3) and ton (10^3)

1 Like

2 Likes

Management also told in previous concalls that margin will be comparatively low for newer products. They need to compromise on margin to grow. HALS ramp up we can know in this quarter concall.

Vinati is entering in MEHQ is definitely worrisome. If they can produce MEHQ by same low cost method of anisone vapour as clean science then definitely clean have to give up pricing power & volume. Does anyone knows, Vinati is going to produce MEHQ for self requirement (I think currently Vinati needs MEHQ & they procure it from clean science) or for both - self consumption & selling in market?

Market is anticipating all these risks that’s why price is half from top. All depends on how much margin contraction due to new products & whether vinati is able to produce low cost MEHQ or not.

6 Likes

In my personal opinion, the Management had a cautious tone in the recent Concall w/ some positives and negatives going forward.

Some notes from the Q2’FY2024 Concall by Management:-

Positives

Product Mix Change:-

This is reflected in improved margins this quarter and will help in product diversification going forward.

New Customer Acquisition for HALS:-

This volume should be reflected in the upcoming quarters for Clean Science

Potential Mean Reversion Play:-

Strategic Capex(30Cr) with Large Revenue(100Cr):-

Negatives

Destocking Pressure to continue:-

This should continue for a couple of quarters

Demand Environment continues to be weak:-

Under performance of Performance Chemical Segment:-

Summary:-

- The valuations of the company continue to be a bit elevated.

- It is a debt free organization with all the planned CAPEX to be funded from internal accruals.

- The overhang of management bringing the stake <75% is done and FII have increased the stake over last 2 quarters in the company.

- Demand environment and destocking situation will potentially result in some headwinds in coming couple of quarters.

15 Likes

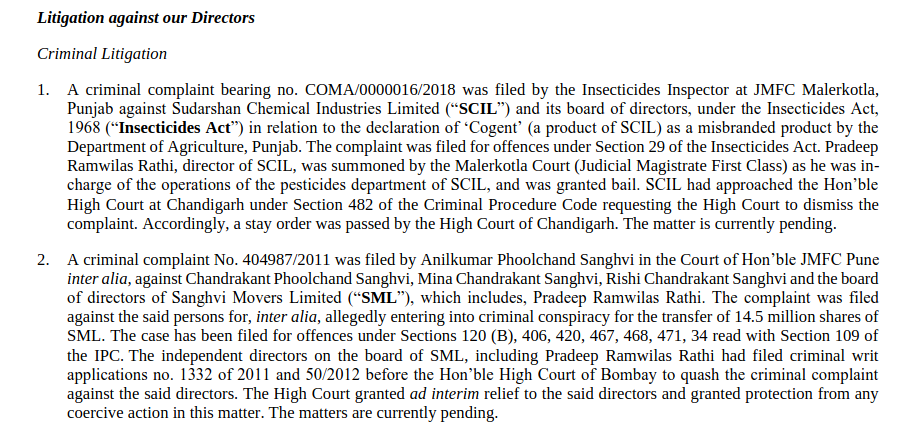

I was going through the DHRP of the company. As mentioned at the start of the thread, there are some criminal litigation against the company and against one of the director.

Two FIRs are against the company in 2016.

And two complaints are against one of the director, one was in 2011 and second was in 2018. In 2011 complaint, there seems to be corporate governance issue as the allegation is of criminal conspiracy for the transfer of 14.5 million shares.

All four cases are pending as per DHRP. Does any members know the current status of these litigation or whether company has given any update?

Disclosure: Not invested.

4 Likes

key takeaways from Clean Science and Technology Limited’s (CSTL) investor presentation

Financial Highlights

- Revenue: FY 2024 saw a volume-led growth in revenue, with Q4 FY24 recording INR 225 Crore, marking a 16% sequential increase from Q3 FY24.

- EBITDA Margins: Remained robust throughout the year, with Q4 FY24 at 44.4%, slightly down from 49.1% in Q4 FY23.

- Profit After Tax (PAT): For Q4 FY24 stood at INR 74.8 Crore, a 20% increase from Q3 FY24, though there was an 8% decrease year-over-year.

- CAPEX: The company invested approximately INR 235 Crores during FY2024, including INR 215 Crores in a subsidiary.

Business Performance

- Clean Fino-Chem Limited (CFCL): Commercialized in March.

- Dividend: A final dividend of INR 3 per share has been recommended by the board.

- Revenue Mix: Notable increase in revenue share from newer products, especially in the domestic market.

- Geographical Revenue: Americas and Europe maintained steady revenue shares, with an improvement in China’s share in H2 FY2024.

Operational Efficiency

- CAPEX Utilization: Focused on commercializing new products, with significant investments in subsidiary CFCL.

- Asset Turnover: Demonstrated efficient use of assets with a healthy cash balance despite the largest capex in the last two years.

Market Position

- Global Presence: CSTL serves over 500 customers across 30+ countries.

- Product Leadership: Holds the largest capacity globally for flagship products like MEHQ and BHA.

- Innovation: Continuous R&D led to the commercialization of new products like HALS 770 and 701.

Sustainability Commitments

- Renewable Energy: 17.4 MW of solar capacity, with renewable energy accounting for 55% of power consumption.

- Environmental Goals: Aiming to plant over 11,000 trees in the next three years and reduced fresh water consumption by 14%.

9 Likes

CLEAN SCIENCE AND TECHNOLOGY LIMITED Concall Summary Date: 15 May 2024

FINANCIAL HIGHLIGHTS

The YoY increase in revenue from operations was primarily led by volume growth.

The EBITDA declined by 6% YoY to ₹99 crore from ₹105 crore in Q4 FY23.

On a QoQ basis, the revenue from operations grew by 16% on account of a 23% increase in volume growth which was partly offset by a 7% decline in price realization.

During the quarter, the EBITDA increased by 14% QoQ and the EBITDA margin stood at 44.4%.

The net profit grew by 20% QoQ to ₹75 crores led by a better product mix and the benefit of operating leverage.

BUSINESS PERFORMANCE

Segment-wise revenue contribution was: Performance chemicals ~67%, Pharma & Agro Intermediates at ~19%, and FMCG (fast-moving consumer goods) chemicals at ~14%.

During the quarter, the revenue contribution from principal products was 76% as compared to 84% during the same period last year.

The capacity utilization stood at 70% for performance chemicals, ~70% for Pharma & Agro Intermediates, and ~75% for the FMCG segment.

The performance chemicals segment profile diversified by adding new HALS (Hindered Amine Light Stabilizers) 770 and HALS 701. However, the price realization impacted the growth during the year.

During the year, the pharma and agro segment reported de-growth primarily due to Guaiacol, which recovered in the year’s second half. The DCC (Dicyclohexyl Carbodiimide) product contributed positively to the growth during the period.

The FMCG segment contributed positively to the growth during the year.

The company’s new product segment, i.e., HALS 770 and 701 continued to report sequential volume growth with sales increased by 40% on a lower base.

In FY24, the new products, i.e., PBQ (Para Benzoquinone), TBHQ (Tertiary-butyl hydroquinone), and HALS contribution was 23% from 18.5% in FY23.

During the year, the company incurred capital expenditure of ₹235 crore. Of this, ₹216 crore was invested in the subsidiary Clean Fino-Chem Limited (CFCL).

During March 2024, the company commenced production at Clean Fino-Chem Limited.

HALS 701 is majorly used in water treatment. The major market for the same is out of India. The company has started trial orders and commercial shipments to its customers. It expects to reach ~1,000 tonnes per annum of volume in the next 3-5 months.

For HALS 770, currently ~50% of the Indian market is supplied by the company. In the next 3-4 months, the company expects this to increase to ~60%-65%. The company is giving a price discount of 2.5%-3% on this product compared to its competitors. In the export market, the company is shipping material to Europe and the Middle East. It is in discussion with customers and distributors in North America.

Europe region is the bigger market for HALS products.

FUTURE OUTLOOK

The company is on track to commercialize the capacity for pharma intermediate by Q3 FY25. The capex for the same was ~₹30 crore.

The management expects the volume growth for FY25 would be mainly from new products and capacity ramp-up of new pharma intermediate.

In the HALS series, the company expects sales of ~3,000 tonnes per annum by year end with majority sales of HALS 770.

The company expects to launch HALS 622 and HALS 944 in the next 3-4 weeks. It would further launch HALS 119 and 2020, which would be largely towards exports.

9 Likes

Pretty neat work. What do you think about making it live online in Google Sheets or Microsoft SharePoint so that we can subscribe to live updates, and also possibly make updates

6 Likes

Hello

I’m still refining the structure of this tracker. It would be great to collaborate on a trial version—let me know if you’re interested!

Aadhar

2 Likes

Hello everyone.

I see there has not been any deep discussion for clean science on VP forum.

Let me start adding my view and then would like to connect with you all for a discussion.

Industry:

- Industry has faced enough headwinds as of now - realization and demand has been the big concerns

- From the latest concalls of many chemical companies, one thing is clear to me that volume has started growing

- On the realization front, it is still not turning up, but management said they won’t go below this pricing for their products - hence that part also looks pretty much stable from here.

Clean Science:

- The company enjoys one of the highest margins in the industry

- The chemical company produce mostly goes to build up another products, hence big companies are their customers

- Company is the only non-chinese player entering into many products - management said foreign customers don’t even know that Indian companies can make this kind of products

Don’t want to go so much into the business discussion, but this is the state of the company as per me:

-

On the business front, volume growth is expected, with flat or improving realization going forward.

-

Company’s flagship products are at 70-75% utilization, which is optimal, and hence incremental volume growth is expected from new products lines - HALS series, TBHQ and DCC, along with new Pharma capacity.

-

Margins are more or less sustained, and won’t improve from here - supposed to be flat.

-

Efficiency rations have degraded, mostly due to the lower demands - they should improve

With all these, the company would be very attractive if would have available at decent valuation - which is not the case.

To create wealth of investors from this valuation, the new products line must be killer and should generate very high revenue growth with high efficiency.

Views are welcomed, 9510274855 - Meet is my number for good discussion.

Thanks.

7 Likes