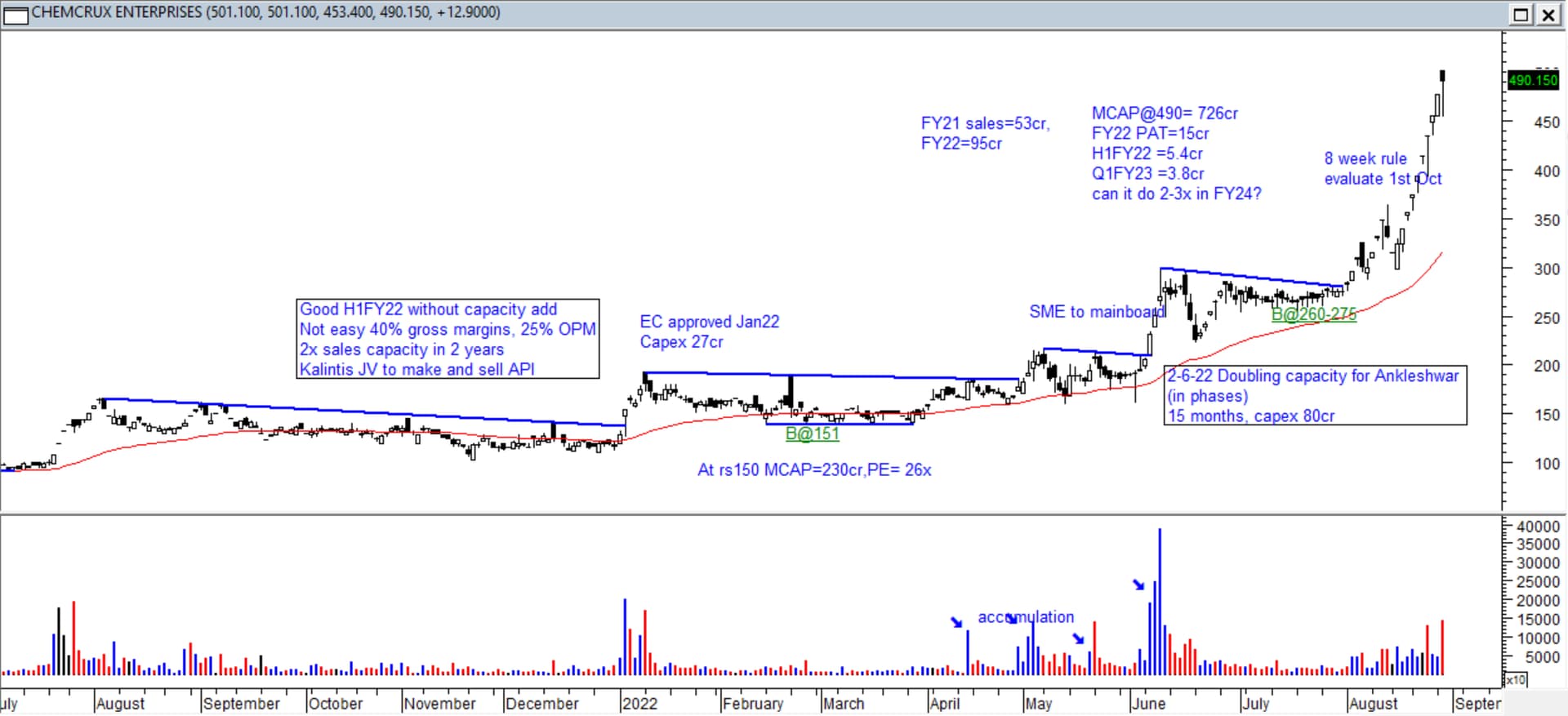

As per this 2 June release “The Expansion plan is expected to be completed over a period of 15 months & would require an approximate investment upto Rs.80 Cr.” I was under the impression that this doubling of capacity was initially proposed for 27cr investment (Source). Does anyone have an understanding on this?

@ayushmit any comments? Is this a greenfield or brownfield? Is it additional expansion?

The market seems to be rewarding the stocks of the companies that showed good results during the pandemic—Chemcrux is one of them. However, there seems to be something more going on.

Any idea why the stock has run up so much in the last few weeks? Is this a long-term re-rating of the stock or is the market predicting higher revenue in the next quarters (due to capacity expansion or something else)?

These kind of moves happen only when there is someone with insider information or general lollapalooza effect.

There is nothing that great about this business to trade at 50 PE.

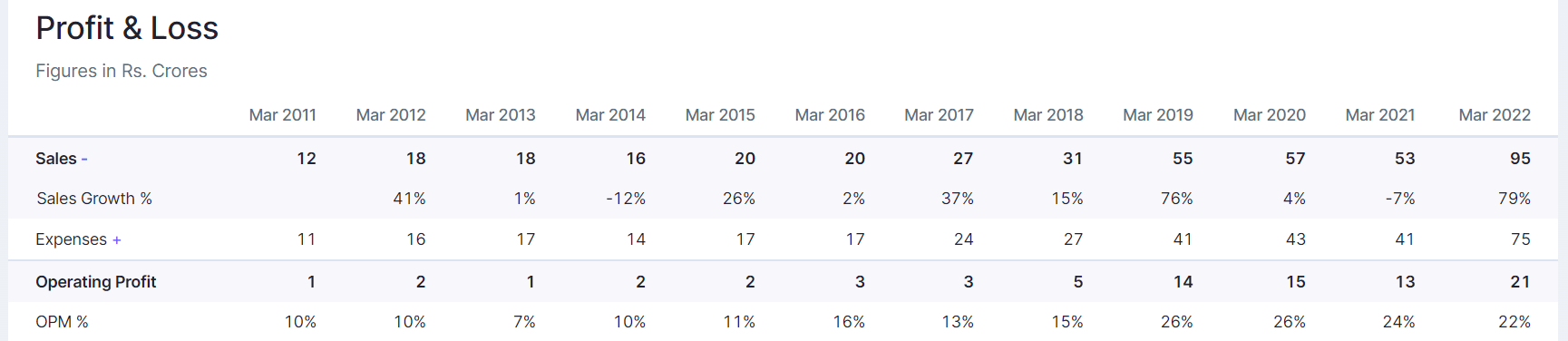

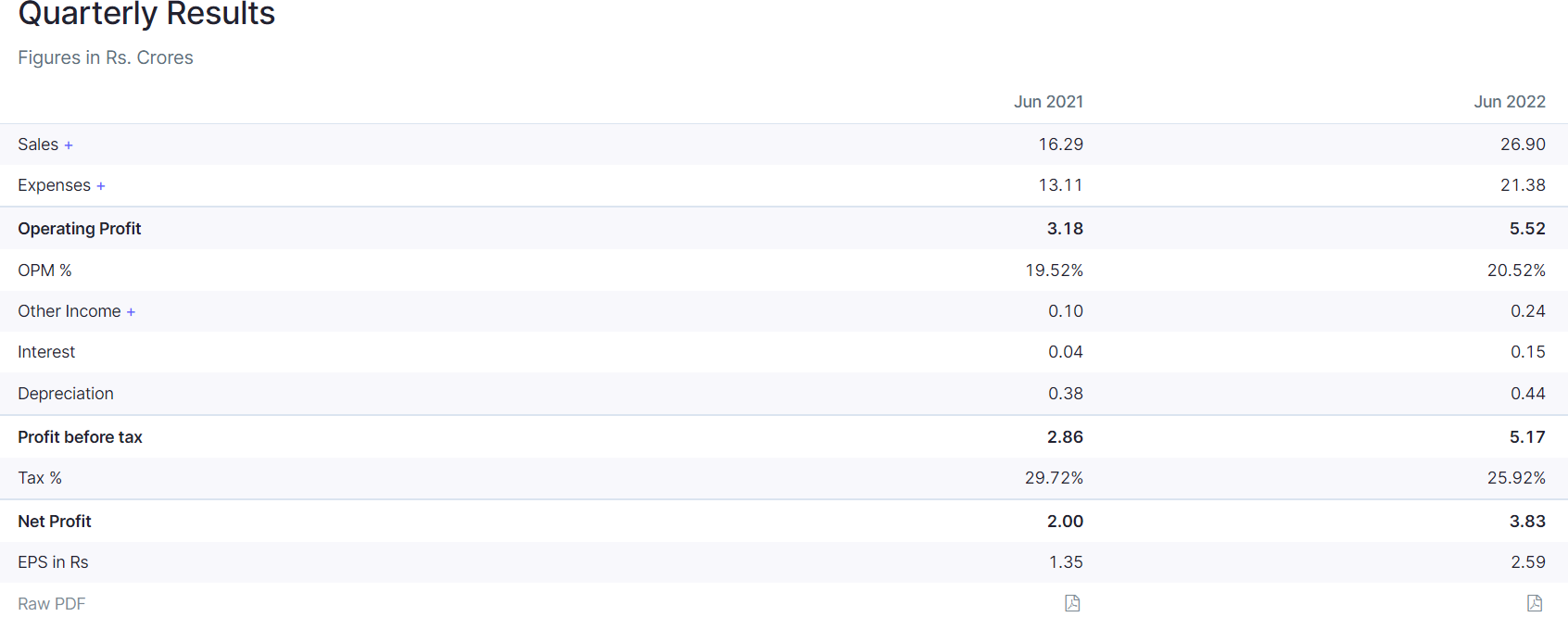

I think Chemcrux had posted a very good performance. The company was on a flat revenue for last 3 years and look at the jump in FY22. They did almost 27cr in Q1 vs 16.3 cr yoy. So even without the new capacity they have been able to post this good performance. We should also keep in mind that many chemical cos margins have come off sharply, some have barely posted profits.

Here is a guy who posted great numbers and managed very well on margins. Its still early days but if they can keep at it, the new capacity will take CY 2025 numbers in another orbit. A company with 100 odd cr annual revenue is planning a capex of 80cr. That is a large number for a brownfield capacity. I feel it is checking all boxes for a big winner. Valuations are not cheap after the sharp move from 270 to 470. Theoretically, a 50 PE on TTM basis is 25PE 1 year fwd if they can double the profits. Need to get more details from the management about the capex surprise of 80cr vs 27cr earlier.

Hi, @pikrohit, nice write-up on the facts.

In the proposal submitted to the Environmental Board ( ECB/SEA/SEAC) for validation in 2018 and 2019, the amount mentioned in the proposal are (estimates) ballpark figures.

The figures do change in reality.

Thank you

Yes many companies have mentioned increases in project costs due to increase in steel and other prices. But the max increase is of the order of 20-30%. In this case its almost 3x. There has to be a major change in plans for this large change.

Hi,

Greetings for the day.

The AGM was online and the management seemed quite confident about the future with their opening remarks stating that Quality, reliability, and consistency in their approach made it to where they are now.

The expansion of the plant is in line and would be completed by F.Y. 23-24 with 40crores including civil constructions and erections etc.

If found feasible another 40crores of effluent treatment systems making it a ZLD unit.

These would be internal accruals majorly and debt would be closely monitored.

Separate warehouse construction has been completed to cater to the expansion.

The management is looking forward to cost reduction processes in chemistries and other areas so as to increase the bottom line.

The joint venture Kalichem would be operational by F.Y. 23-24 which the company seeks to benefit from the existing and from new opportunities.

These were the opening remarks by the management followed by questions from the shareholders but not much luck this time I got cut off after 25minutes into the AGM.

I would request others who have attended to take it forward.

Thank you and my apologies.

Hi,

The attached file shows the application (page80) R&D product list (page81) with their approximate recurring cost per annum for pollution control measures(page 98).

The R&D products are to be made at 100gm/day constituting 200+ products at 0.3 MT/Month per product of sampling. 380th meeting(VC) 14032022 chemcrux.pdf (252.5 KB)

Taking the opportunity to upload Meghmani finechem’s status on the approval of their recently announced products of benzoic acid and its derivatives with a market of 300cr. Minutes_1093rd_SEIAA_Meeting Meghamani fine chem.pdf (344.1 KB)

The application is withdrawn and the reasons are best known to them.As per data on the website

(page 40) details of withdrawal has been mentioned. SEAC Minutes of the 510VCTH I Meghmani.pdf (2.1 MB)

Not to offend anybody, had to share as I have been following it for competitive analysis.

Would be taking it down if anybody finds it non-relative.

Thanks

Here are the notes from the AGM ( notes may be rough but this is the synopsis).

Girish Shah spoke in his opening remarks that

The expanded capacity has doubled and will cater to orders coming from existing clients and new clients.

China is becoming very aggressive and getting market share is becoming tough.

Multiple factors hampering growth at the moment.( Logistics cost, Purchase cost, Geopolitical issues).In the A.R. Exports dropped to 18% and domestic sales were 82% shows the impact of the above factors on sales.

The joint venture Kalichem would be operational in the second half of the year which would be catering to API, Intermediates and the existing range.

The company kept adding new clients and introduced new products which is mentioned on their website, but no formal business yet from these products.

The promoters remain unfazed of the future that things would change, benefetting the company with better prices, both from purchasing of raw materials and selling prices of products.

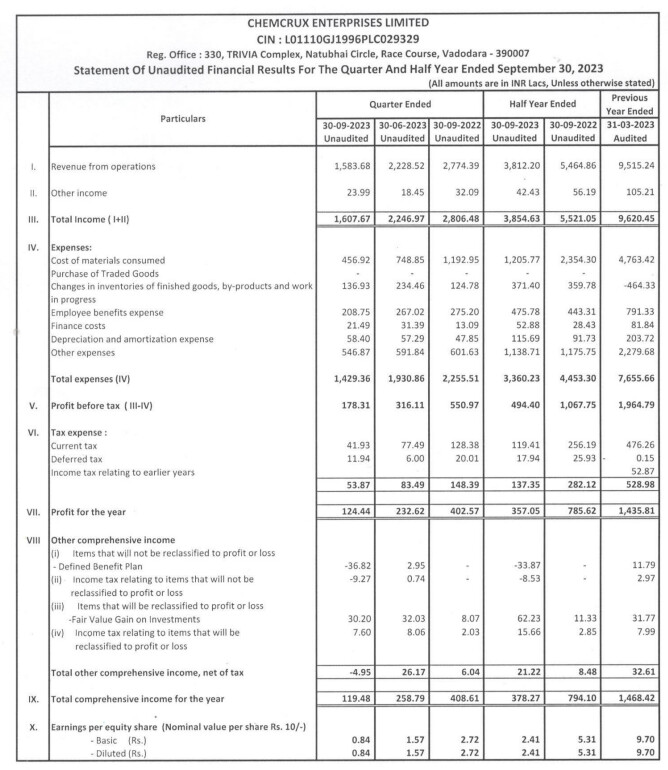

The short term position of the company is too hard to derive at a growth rate for the factors stated above. F.Y.25 remains tough as the visibility has not improved with the existing conditions and as you all can see that the profit has taken a big hit.

Kalichem expects 50% capacity utilization in the coming year and no expectations on the profits though.

The company enjoys a high good will among their customers in the domestic market and has the necessary certifications needed to qualify to be a vendor.

Recent certifications was from EVOVARDIS awarded Chemcrux with a “Committed” certifications.

Steam purchases would be cut down by 30% (ball park) as the generation of steam would start from October 2024.

Anyone tracking this stock? The company has come down from 450 to 100 rupees.

Anyone who could suggest what to do to track this company? Have been holding shares from 280 rupees avg cost.