So, I started tracking it recently. As of today, it is on upper circuit at 143. It has risen 43% in last 3 trading session. Could be a potential reversal.

Why I am tracking it ? - I recently concluded reading prasenjit Paul’s book where he as discussed about this as one of his multibaggers and reasons for the same. I guess his price point was somewhere in 70s when he bought it in 2018. It was written in 2022. This stock made a high of Rs. 500 in Sep 2022 and since then have been on a continuous decline and made a recent low at Rs. 100. The reason is declining fundamentals which is obvious from a high-level look. However, the interesting part is that neither Prasenjit nor the promotors sold a single share in these last 3 years. That tells me that these are probably temporary setbacks company might be facing and both of them expects a reversal. I tried finding more information on this but unfortunately, couldn’t find much as to why the fundamentals declined. On a high level, from some sources, I concluded that it was due to capex in expansion and competition from China.

What is the right price point - I feel this stock has already made the bottom of 100 and it might not go below that in expectation of a better Q4 results due to new capacity expansion showing results. However, I was cautious to not enter now and is waiting for Q4 results. If they deliver good Q4 results, I am taking my position then.

However, the question is, what if it rises another 40% until then ? Yes, that is a possibility, but I guess I am learning to be patient for the right time to enter and not jump suddenly.

The recent 40% rise is, in my opinion due to the sentiment that Trumps recent tarrifs impact China more than India so this would turn favorable to specialty chemical industry of India and thus Chemcrux will also benefit.

I am expecting that the stock should consolidate at these new levels until Q4 results and take a direction from there.

Happy to hear thoughts from others.

1 Like

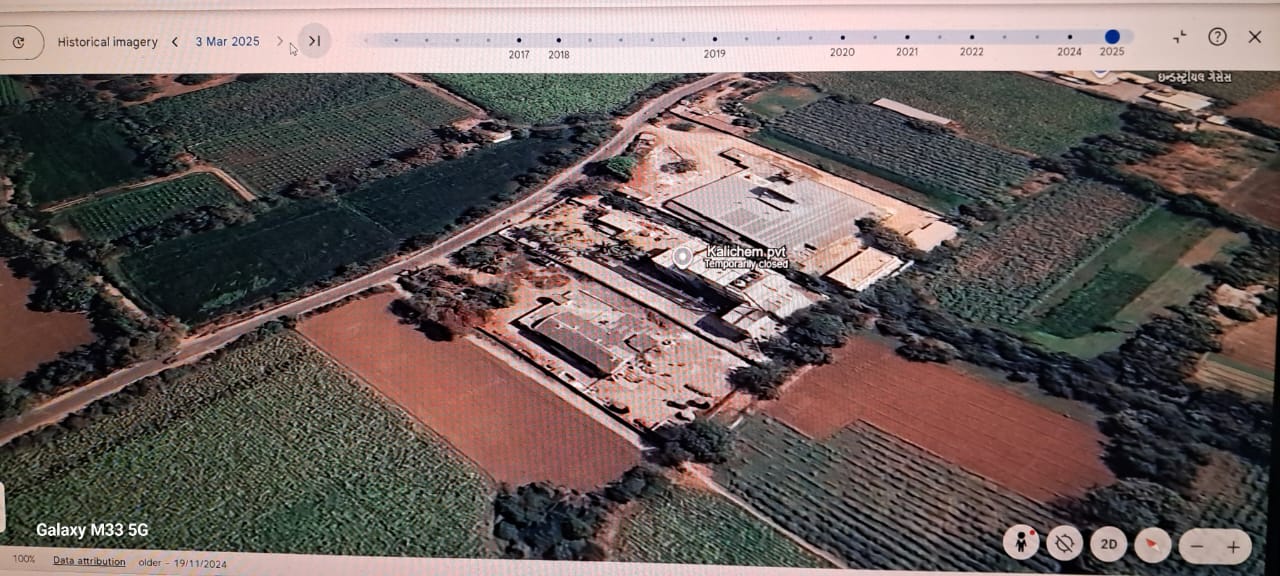

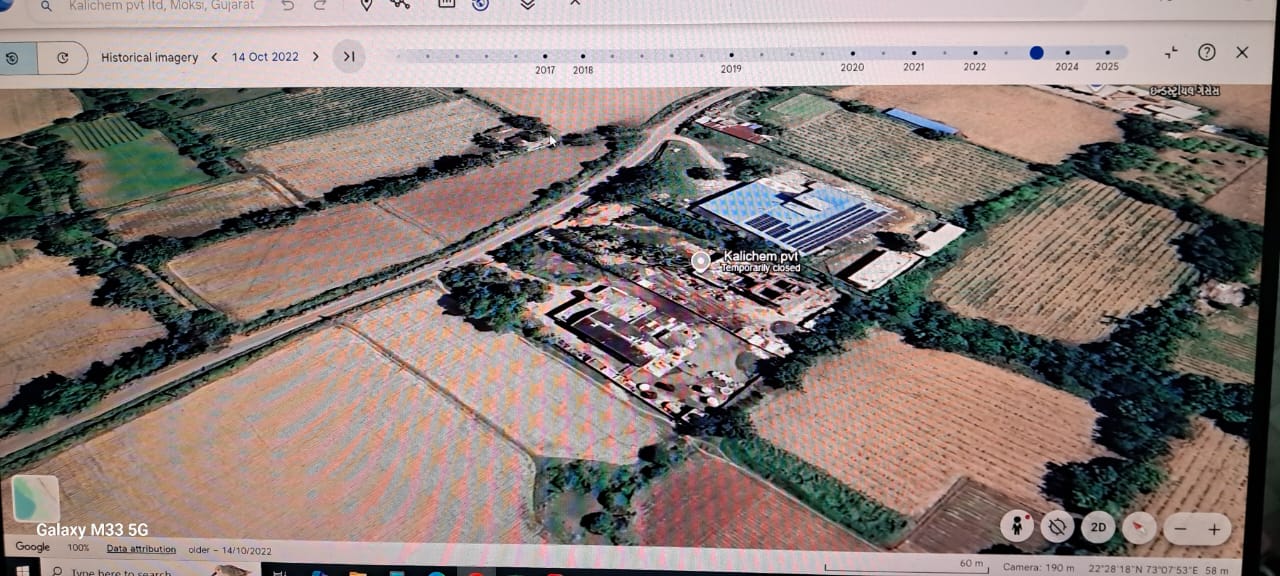

Developments of Kalichem from October 2022 to March 2025

An update to the forum.

1 Like

HIGHLIGHTS FROM THE AGM

-

Chemcrux remains committed to capitalize long term

industry favourable trends. Volumes have increased

in spite of revenue de-growth owing to increased

pricing competition lowering margins. De-growth

was due to subdued global demand, logistics

challenges and geo-political tensions.

-

FY 25 sales were down due to this and margins were

suppressed due to higher purchase costs and

increased logistics costs. FY 26 may be a dull year

too.

-

Despite pricing pressures and global challenges the

company has retained the confidence of long term

clients with healthy collections and liquidity.

-

Sales volume were 4% lower compared to FY 23-24

but 21% higher than FY 22-23, reflecting demand.

-

Steam expenses have reduced. The overall utility

cost per KG of productions reduced by 15%

compared to FY 23-24.

-

Kalichem is a wholly owned subsidiary with

operations commencing.

Rs.50,000 was spent towards share capital and a

repayment loan commitment to Kalintis was given to

the tune of Rs.3.11cr

-

50% capacity utilization for FY 25.Company aims to

achieve 20%-25% growth over the next three years

supported by expanded capacities, taking the

capacity utilizations to 70%-75%.

No further capex in the near term.

Approximately, on average 50% of sales from

benzoic derivatives.

-

The company imports Chloro-toluene majorly.

-

Company has an exclusive marketing and supply

agreement with Deepak Nitrate for Para nitro

benzoic acid. This provides wider market access,

brand acceptance and faster customer on-boarding.

raw material for this product is Para nitro toluene

which is supplied Deepak Nitrate.

The company will benefit from consistent quality

maintenance and timely availability of the product

avoiding any raw material supply shocks and

procurement risks.

The company can focus on efficient manufacturing

and benefit from marketing spends, distribution

spends and sales infrastructure for the said product.

This ends the AGM.

While it is too early to take a decision on whether all or

some of the prospects bear fruit.

There was a contradictory statement of 20-25% growth in

next 3 years and, the next year may be a dull year.

There was not much clarity on Deepak nitrate sales

prospects to the company, though the agreement was only for a single

product.

or could it be a start to pave way for other products to

come Chemcrux way.

I remain invested as the promoters seems to be honest

and seem to be in line with shareholders expectations

about management integrity.

Thank you

4 Likes