2 upcoming growth engine for CDSL

-

Dematization of non listed companies…

There are lakhs of MSME and SME in India… -

Dematization of all financial products… mainly insurance

When SEBI mandate the above 2… the number of demat accounts will grow…

2 upcoming growth engine for CDSL

Dematization of non listed companies…

There are lakhs of MSME and SME in India…

Dematization of all financial products… mainly insurance

When SEBI mandate the above 2… the number of demat accounts will grow…

LIC is bringing its own digital insurance platform. Also, on both points, why won’t we have CAMS as competitor ?

SEBI comes as a Capital Market regulator and CDSL being a Depository is an entity under SEBI’s purview. Having said this, only instruments that can be traded in the market (primary/secondary) would fall under capital market.

By saying this, do you mean insurance products are likely to be traded?

Regarding the new announcement on insurance Dematization… I just want to find how it work. Will the insurance companies dematerialise or the customer have to do…

If customer have to do, many brokers like paytm, zerodha would open up opportunities to dematerialise. else the customer who have CDSL account can directly do it…

What about insurance policy holders who doesn’t have demat account? If I am not wrong they would prefer to dematerialise with their own demat partner (mostly NSDL)

When new policies are issued will that be dematerialised when issuing itself.

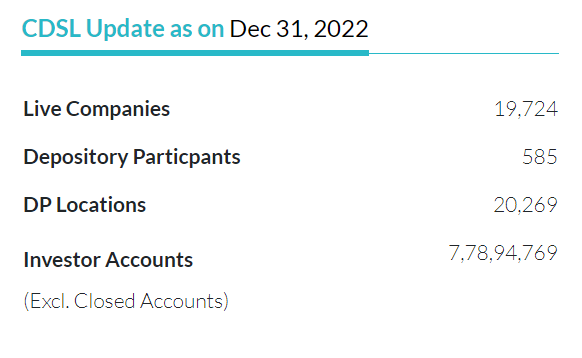

Account additions continue to be impressive with about 46 lakh new accounts opened during Q2.

AJ

Disclosure: Remain invested.

Good questions.

However, Dematerialisation is a misnomer here. What is being looked at is digitising the insurance products which every industry participant would look at offering for the obvious benefits.

Healthy trend of account additions continue:

AJ

Disclosure: Remain invested.

Just a general question, what happens if is CDSL is not available ? Can Market function ?

did some more digging

i am really surprised at the nonchalant report they filled doesnt have too much details

since CDSL is a listed entity i think they should do better reporting and even more worrying is the fact that www.cdslindia.com is down too ![]()

BTW : got some interesting info from Nitin (Zerodha) on the same topic

https://tradingqna.com/t/cdsl-unavalibility/139381?u=aveekbhat

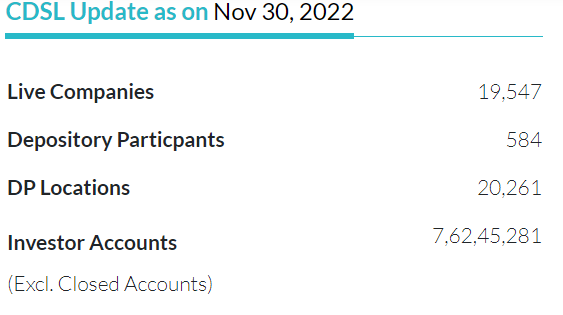

14 lakh accounts added during the month of November 2022:

AJ

Disclosure: Remain invested.

New share: CDSL to buy more than 46K squrefoot office space at Marathon Futurex-4.

Any update on the total investment in the property would be useful.

AJ

Disclosure: Remain invested.

Account additions continue to be healthy.

Disclosure: Remain invested.

AJ

In my limited knowledge, I think we need to focus on transaction volumes growth as that largely determines the money CDSL makes. Is their a way we can get that data every month (like how we get similar data for MCX)?

News share: BSE to sell 2.5% holding in CDSL via OFS route.

I believe this is to bring down the shareholding to limit as set by SEBI.

AJ

Disclosure: Remain invested in CDSL and BSE.

Can you please elaborate more on the minimum shareholding threshold? I believe BSE holds 20% currently, is that the requirement from SEBI for exchanges ?

As per my understanding , SEBI have prescribed maximum 15% share holding

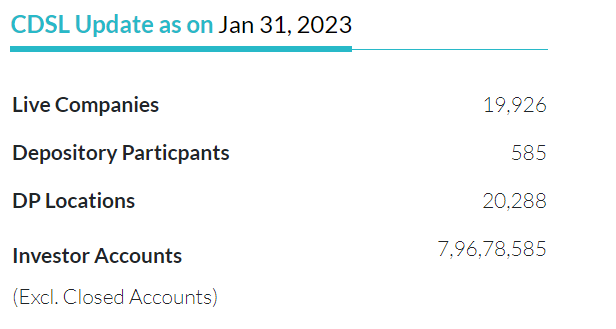

The account addition continues to be healthy with nearly 18 lakh new accounts added during January 2023. Expect a disclosure on hitting 8 crore accounts soon.

Live company additions >200 for Jan.

AJ

Disclosure: Remain invested.

I don’t know if this point was discussed in the thread before, but the opening of new demat accounts need not be from new participants in the market, it could be a combination of existing participants who are opening accounts with different brokers, along with newcomers. Many people have more than 1 demat account, and some of those accounts are dormant, the accounts are not used as they are opened just to check the features of a broker, and if unsatisfied are not used again. So I am guessing CDSL benefits from new accounts opening but the benefit does not get extended if the accounts are not used further.

And I think many brokers publicize that there are no AMC charges, so if a part of those charges goes to CDSL, it will not get this.

Just sharing what I am thinking, no investment.