Account addition while important is not the most important metric. It helps in contributing to part of the revenue which is largely stable in nature.

Equity delivery volumes are the key metrics to track. This is cyclical in nature - during bull run there will be high volumes and during other times it will be low volumes. Revenue earned from this is what drives the bottom line growth or de-growth and also brings in operating leverage during good times.

Equity delivery volumes have been on a downtrend since many months now and that is also reflecting in the share price. Lot of shift has also happened to F&O volumes, but CDSL does not directly earn from the trading of the same (please correct me if I am wrong).

So unless we see a meaningful increase in equity delivery volumes, share price will not show any worthwhile growth.

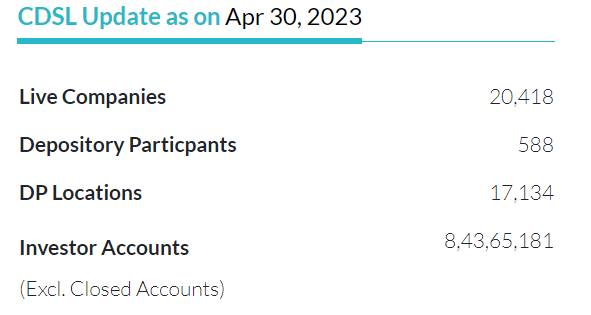

The account addition momentum is very much intact. Another month with >15lakh new accounts. Total accounts added during the year has exceeded 2 Crore translating to about 17 lakh new accounts per month - while this is significantly below last year’s average monthly account addition of 25 lakh, the trend is reasonable and seems to be sticky around 15 lakh per month currently.

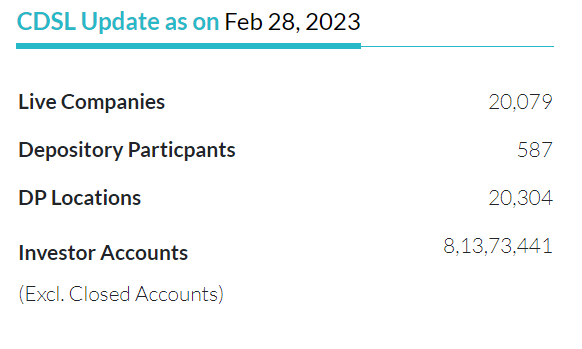

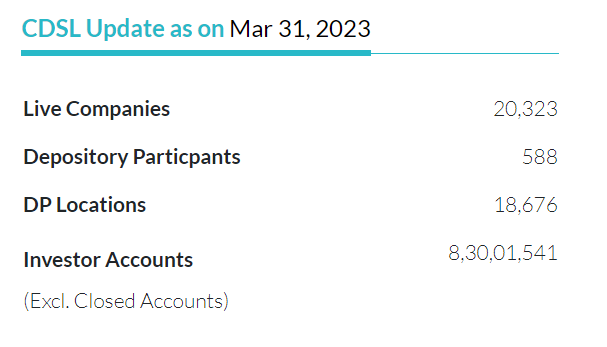

The live company addition is about 2000 for the year (18,268 as at end of March 2022 against 20,232 as at 31 March 2023).

Team, I’ve a question regarding the CDSL balance sheet. Under the balance sheet section for Mar 2023, we can see CWIP of 173 cr which was 4cr for 2022. Can anybody throw some light on this particular section and how come it will help CDSL to unlock value. In a typical manufacturing co, we understand there must be some CAPEX at a forward looking view but for CDSL where net profit is close to 300cr then how come this CWIP is going to help the company?

How is this purchase going to unlock value for them is my next question. Somewhere, they must mentioned about it, I am sure, they must have weighed their options and understand the pros and cons.

If the bull run comes (indications are in that direction), traded volumes will spike and that should directly result into more revenue and higher earnings for CDSL. As and when that happens, CDSL will become a relatively lower risk script for decent gains

@AJ41 How are you tracking the total equity delivery volumes in real time?

If we track the nifty volumes, would that be a good proxy? Since you’ve been tracing CDSL since a long time, wanted to understand your perspective.

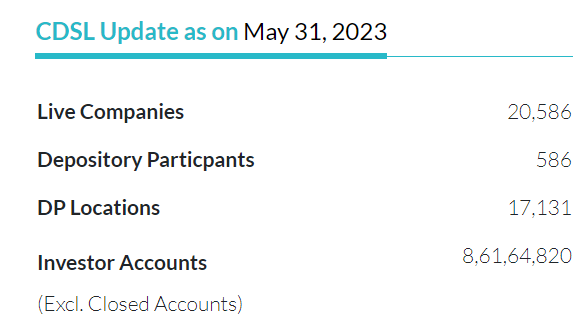

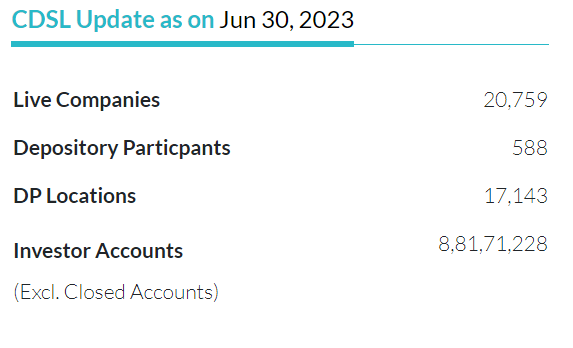

20 lakh new investor accounts and about 170 new live companies added in the month of June 2023.

In excess of 51 lakh new investor accounts and 420 odd new live companies are added during the quarter. Momentum is certainly encouraging. Lets see how this is going to reflect in the results for the quarter.

As NSDL IPO is coming in sometime with an potential valuation of 15-16k crore. How does this arbitrage justify with CDSL having higher MarketShare, better profitability and cashflows??

Based on the latest data, CDSL is significantly ahead of NSDL in terms of DP accounts and financial performance.

Investor Accounts:

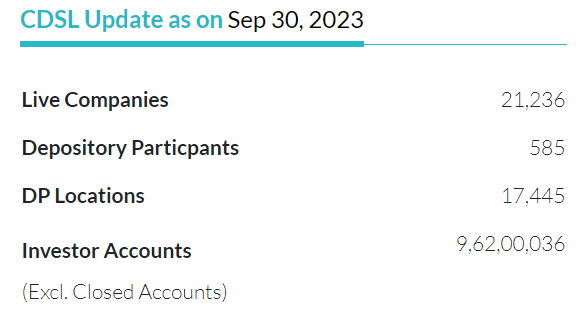

CDSL is at 8.81 Crore against NSDL’s 3.23 Crore as at end of June 2023 - That’s a gap of approximately 2.5 times.

Financials:

CDSL has reported revenue of 555 Crore and profit of 275 Crore as against revenue of 401 Crore and profit of 210 Crore reported by NSDL(link to NSDL financial statements) for the year ended 31 March 2023.

NSDL has traditionally concentrated on high quality customers and most foreign and domestic institutions continue to be loyal to them where as CDSL has positioned as the most preferred depository for new age broking houses offering extremely attractive pricing and efficiency. While both serve the same purpose, the way the organizations are functioning are not really comparable.

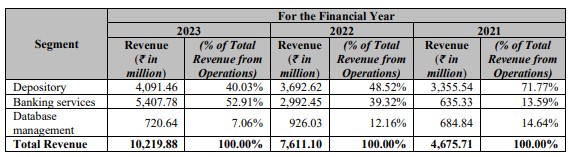

According to NSDL DRHP, it has entered into other ancillary businesses of database management and payments bank businesses, through its Subsidiaries, NDML and NPBL, respectively. Segment-wise revenue generated is as follows:

It shows that the payment bank business is responsible for most of the revenue and growth in recent years. This is also the reason for lower margins than CDSL. It is not comparable to CDSL due to different business models. We should treat NSDL as a payment bank business as its contribution rises further.

Mutual fund investment in india are growing year by year! Is it a big growth driver from CDSL? I know we can hold our MF holdings in dmat where CDSL can benefit, but what about the MF investments through MF house way? Even MF houses need to buy and store shares in depository right? So can we say that the growth in MF investments in india is a bull case scenario for CDSL?

sorry for the noob question but i am still learning this business…

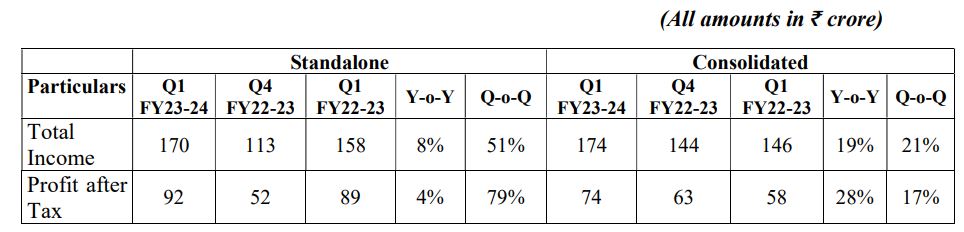

Update for Q2:

New investor accounts exceeding 80 lakh (51 lakh during Q1) and Live company additions exceed 470(approximately 420 during Q1) for the quarter.

Both numbers exceed the numbers reported during Q1.

We are likely to see the best ever numbers from CDSL for this quarter.

AJ

Disclosure: Holding CDSL from last many years. Views are biased.