16.3% (EBITDA margins look optically dropped, but its the value growth due to cost plus model that has increased revenue and hence led to increase in denominator)

22%

PAT Margin

9%

10%

Krishnapalem and Tirupati capacity and execution timeline - NCL Capacity at 55000 tons , fully operational. Tpty (spray dried) another 16000 tons by next yr march. With that capacity will be at 71000 tons. Next FY Q2, 6000 tons of freeze dried capacity at Vietnam. With that total capacity at 77000 tons (spray dried + freeze dried)

Cost of capex: India - 400 cr, Vietnam USD 50 million

On recent acquisition of Percol and Rocket Fuel in UK - CCL products, after 5 years has CCL launched continental coffee and started to build as a good brand. They want to further foray into B2C segment and hence looked to acquire in new markets. Going forward it can add 100cr portfolio. Currently working with, Sucafina, partner in UK to resurrect and launch the brand.

Current revenue from the brand - 18 to 20 cr. We are looking to make it 100 cr in 5 yrs.

Why no continental coffee brand in international market - Brand building in mature markets is difficult. Better to resurrect an existing brand than to introduce a new brand (CCL)

Volume growth 18 to 20%. Company works on cost plus model => Coffee prices go up, selling price also is increased => optically sometimes EBITDA margins look low. Important to track volume growth.

Vietnam capacity utilisation: Old capacity 14000 tons is at 90%, new capacity of 16000 tons at 50%. Blended utilisation growing forward wil be at 70%

UK business will be taken care by Sucafina. Company fully focused on domestic as well as abroad business.

On product innovations going forward - In the past developed freeze diet, instant cold brew, currently working on instant speciality coffee (setup a pilot plant).

Cold brew (innovation complete - looking to push the product) seems to be a very good opportunity. Spcl coffee also is receiving good interest.

CCL Prods also does product development for new startups and companies and help them create product profile.

Interest cost about 88cr per qtr.

No additional WC required for acquisitions as they are already running brands.

Debt profile - 1000 cr WC debt (600 cr India, 400 cr subsidiary), capex debt 600 cr by end of FY 24.

Inventory about 550 cr.

What is the driver for high teens volume growth as coffee market is not growing at exponential pace - Coffee mkt. growing at low single digit whereas company is growing in double digits (meaning mkt share gains)? Economies of scale working in growth, ability to innovate and give better product profile to client with R&D profile.

In 5 years, CCL has built a brand and became no 3 player in India.

On further brands, being very careful not to overlap with B2B customer’s brands

Planning to go to 1.5L outlets, focus on brand building in non-south markets.

Expecting volume growth by 18 to 20 %. Coffee prices supporting, company should do well.

Order book : Freeze dried booked out for 1-1.5 years, spray dried visibility is usually short term. Booked out for next few months.

Currently 8% of B2B market share. Company has ability to gain market share due to low base and hence high growth is expected. Probably the growth will saturate at around 15 % market share.

Currently interest rates are going up from 3 to 6-8% now. On debt: WC debt 1150cr. WIth other facilities coming up, the total debt (including WC debt) is expected to be 2000 cr by FY 25. This is likely to be the peak.

Expected retail revenue % after all the capex is complete? - Can’t say the exact % but it all depends on coffee prices. In B2B if coffee prices increase, because it is cost plus model, revenues will shoot up, but in retail it is difficult to hike prices.

Earlier debt guidance was 1200cr but now guidance is for 2000 cr. Why is the difference QoQ? - It is the changes in the working capital debt that has changed the debt outlook.

Linking an informative post on ‘Export Data…’ thread.

The price (unfortunately) has reacted negatively with the idea of company taking on debt, at maximum, of 2000 crores. However 20% of growth projection for next 4 years is welcome news.

CCL Products going through a demerger between Continental Coffee Private Limited (Demerged Company) and CCL Products India Limited. https://www.bseindia.com/xml-data/corpfiling/AttachLive/fee2cb72-c2a0-4e22-ba37-30b5b881d2d0.pdf

Point xi in the appended order by NCLT Hyderabad Branch:

“The present Scheme of Arrangement does not contemplate any issue / allotment of shares by the Resulting Company (i.e., the transferce Company) to the Shareholders of the Demerged Company (Le, transferor Company), since the Demerged Company is the Wholly Owned Subsidiary Company of the Resulting Company. Need to determine Share Exchange Ratio or valuation does not arise. Hence, Valuation Report has not been obtained.”

Some business updates after Q2 2024 concall: Information is best of my knowledge, excuse for any inaccuracies

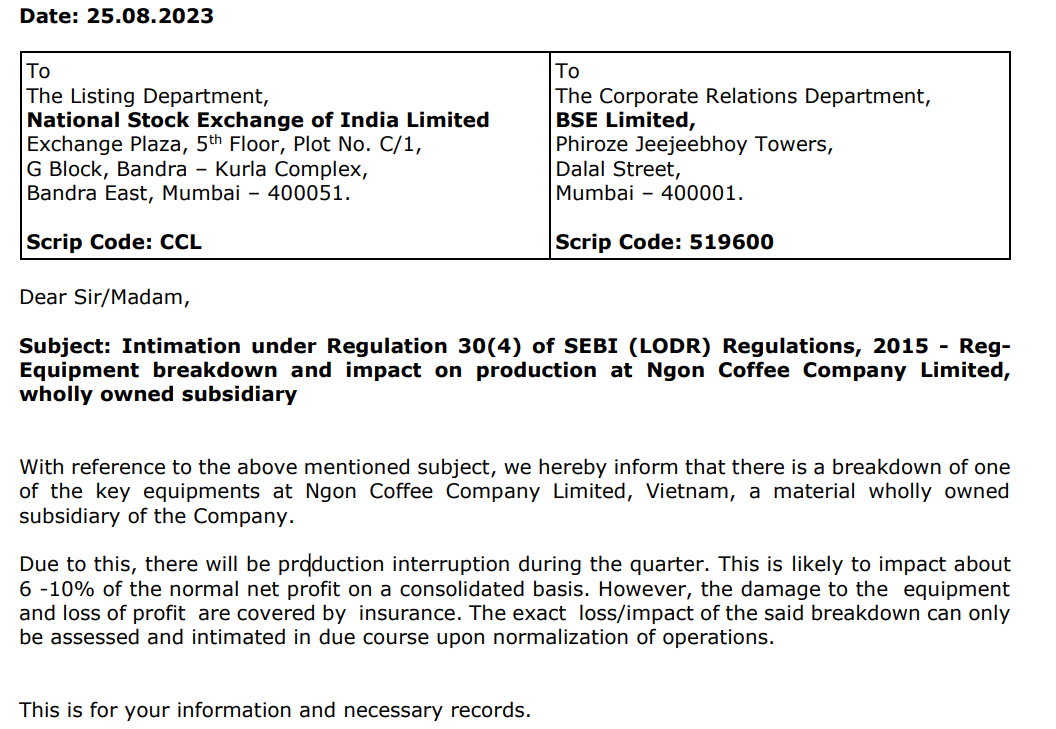

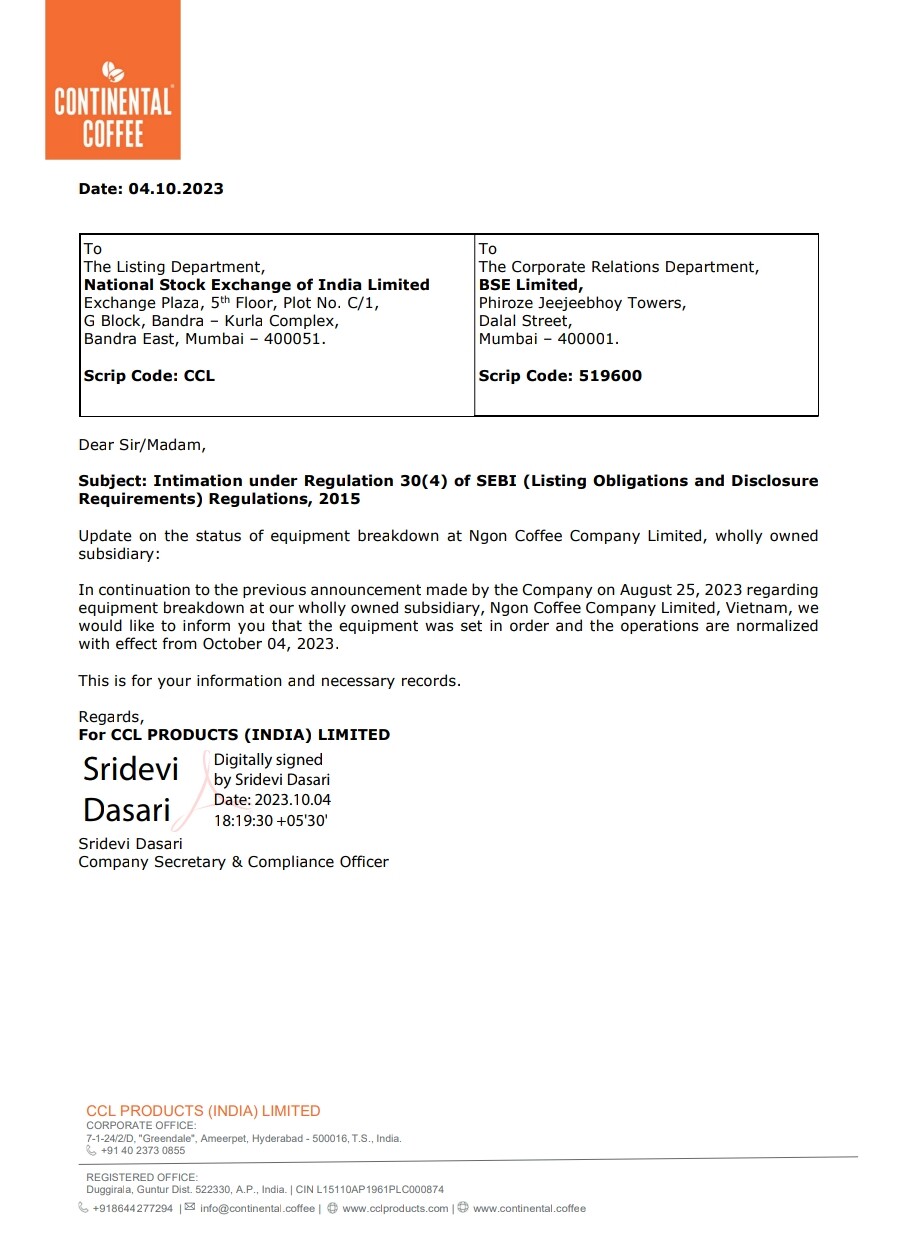

New Vietnam production line got impacted due to machine breakdown, still assessing the exact revenue or volume loss, will be updating once survey is completed.

In this quarter, 12 or 13% volume growth & 20% value growth.

Will get to know the coffee prices trend by December 2023, as new crop supply comes out from Vietnam & India

Capex for whole year is likely to be around 650 Crore, out of that 260 crore is utilized in H1 and rest will be gaining pace in second half.

India Capex - 400 Crore - To be completed by March 2024

Vietnam Capex - 250 Crore - To be completed by H1 FY 2025.

Overall for the Year - Capacity available till FY23 is running at 100% utilization & new capacity will be utilized close to 50%

Thumb rule: Usually for any new capacity - we will utilize close to 30 - 35% in first year, 60-65% in second year & close to 85% in third year.

But for vietnam’s new lines, we have started utilizing 50% from first year.

Peak debt is likely to be around 1800 Cr and all should be done by March 2025, after which repayment would gain pace. By H1 FY25 all capacity expansion capex should be completed & commercialized.

Pure brand business is going to be around 200 Crore by end of this year, which will be less than 10% of overall topline of FY24. Looking to grow this business around 30 - 35%. For next couple of years looking to push more on the topline and not much on the EBITDA for branded business, which we will start realizing from third year.

Margin guidance at group level to be around 18 - 20%, as there are segments that will be accretive & dilutive with new capacities & initiatives.

Speciality segment is close to 2% of overall volumes. There is some exciting development or innovation is happening around it & there is lot of traction from clients

On bottom line, because of interest & depreciation kicking in EPS growth is likely to be impacted & lower than Top line & EBITDA growth for 4-5 quarters - My Understanding

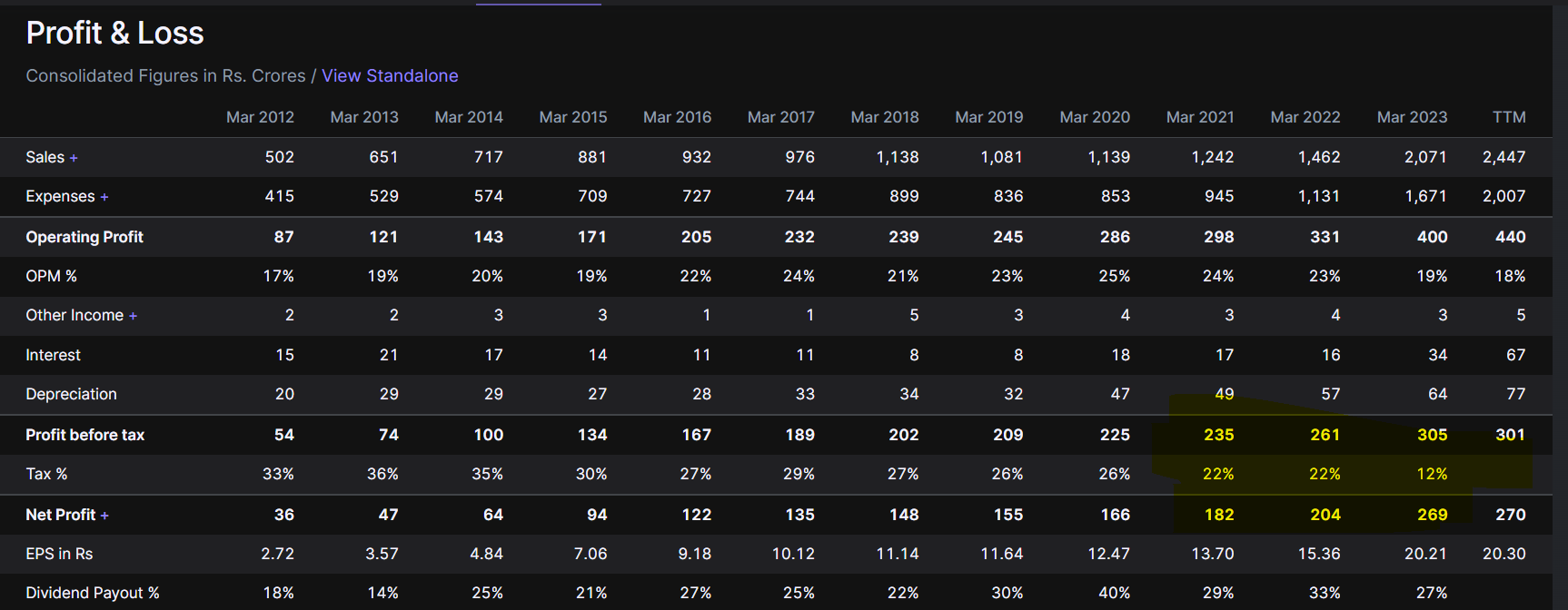

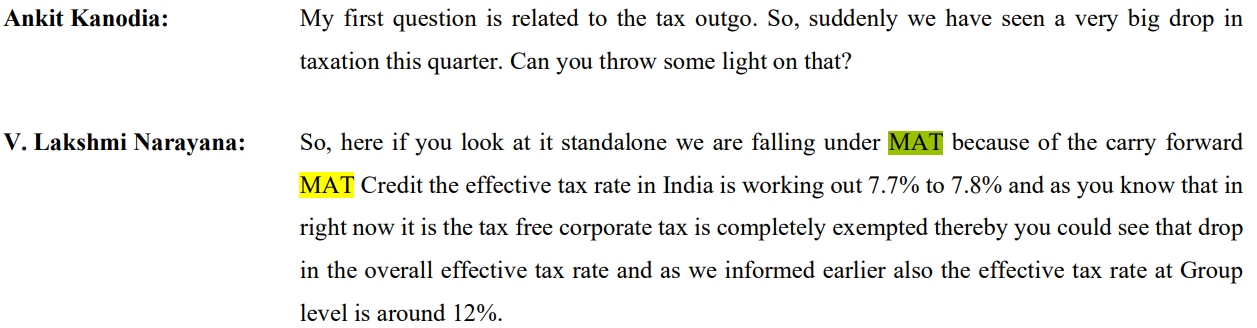

On consolidated basis, Effective tax rate is going to be around 12%.

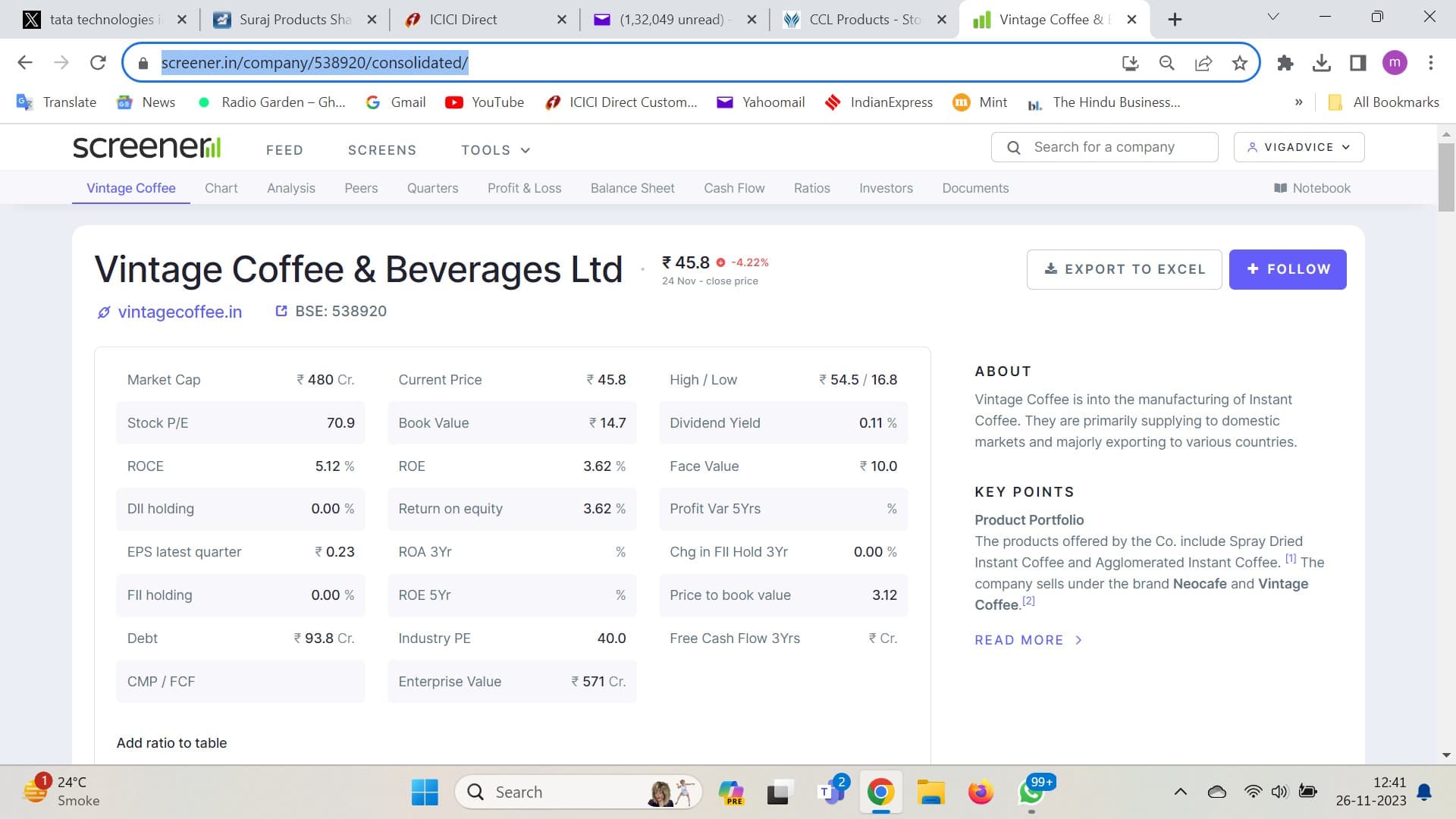

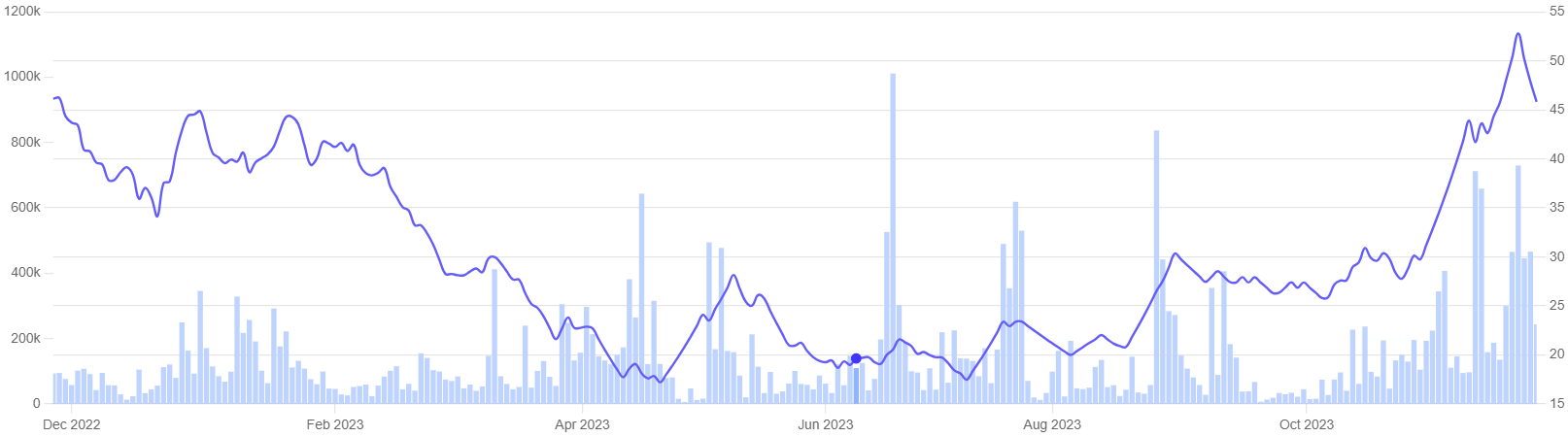

Another coffee maker, Vintage Coffee. A small cap. The management changed hands. Since then, it has been securing orders from Russia, Latin America and the South East Asia. It is still very expensive, but the financials are improving.

800 tons of materials couldn’t be shipped due to Red Sea issue, which comes upto 40-45 crs worth of sales, which will be pushed to the next quarter

On the breakdown of equipment in Vietnam last quarter - Impact was to the extent of 5% of bottom line, currently working with insurance company to get the claim, if claim doesn’t come through until next quarter there might be a mild revision on guidance of Profitability. No change in guidance in terms of Sales

There are 2 kinds of contracts for shipping the products: FOB and CIF. Incase the Red Sea issue persists, 30% of the contracts are CIF, where shipping costs for a longer route to reach destination will be borne by CCL Products and remaining 70% will the borne by customer

Branded Business this year might generate 5-6% at EBITDA level, and will plough it back into the brand. There is no burn at PAT level

Will end the year for continental coffee at 200crs

Coffee Machine (Vending Machine)Business - 4000 vending machines all over India, and looking to be aggressive going forward. Will scale this business in a sustainable manner. Currently the business is around 20-25crs and can become a 100crs business in 3-4 years

Looking at the demand in the out of home consumption, Have been doing some experiments, like Kiosks, and coming up with cafes, to get some proof of concept

Coffee Ecosystem like startup sand D2C brands, most of them are doing business with CCL Products

Continental Coffee - in South, the present is quite good in most of the stores, now focus os on developing markets in the North and other areas

Largest selling pack for the consumer in regard to Continental Coffee is 200 gram pack, which is lower of the segment all together

10% of Continental coffee revenue, is from Online sales

Debt free in 3-4 years, but difficult to exactly give a time line

EBITDA/Ton remains steady, apart from this quarter, where there was a little aggressiveness in Vietnam

Vietnam new capacity running at almost optimum capacity utilisation

There aren’t any challenges with regions, expect there were issues of meeting demand when capacities were running at optimum

Market shares in South market is 3.5% and all India level 2.5%

Continental Coffee Revenue from South India is 60-65%

It’s interesting how their tax rate has been so low for the past three years. Can someone explain why this is happening? It seems like because they are paying less tax, their profit after tax is higher, which makes their earnings per share (EPS) appear better than the actual situation.

Coffee prices are still at high but demand is still intact, and company expects no change to that in near term until Brazil crop outcome by mid of the year.

Minimal impact on deliveries and margins due to Red sea issue