The recent news of Axis Fund Managers’ front running and collusion with brokers has really jolted CCL Products. From what I understand CCL constituted 6% of their portfolio and this is the first time ever that an allegation of this sort comes up for the company - even though it is a part of a collective group of Axis’ holdings.

Personally, I have never had doubts over the integrity of the management (management delivers on targets, no hiding bad news or downtrends, the AR is one of the cleanest in the Indian Market - no confusing RPTs or round tripping, proper disclosures and focus on business rather than share price) and the 4 yr Revenue and PAT doubling story is also playing out. The valuations looked reasonable at 400-410 levels and the current hammering makes it even more propelling. Financially, CCL Products, from my viewpoint, looks to be on track for c. 1500 cr top line and 220cr bottom line for FY22. Add this to a healthy FCF conversion and valuation of 4k cr seems like a steal.

On the business front, the instant coffee demand and macro trends are in place and soft commodities continue to hold steady demand; plus the company is largely unaffected with raw material price increases as it passes these onto the customers. The brand building exercise is also in place with more and more outlets stocking Continental Coffee. I’ve seen even the most staunch fans of Nescafe adapt to Continental - so its efforts are not for nothing on that front. It is a long exercise to present a FMCG challenger to the market but that, at best, is an optionality for the business - the key repacking segments and its proprietary blends continue to remain its key business.

Able management, growing order book and steady operations - this has everything that I have looked forward to in a steady compounder in the last 5 years and continue to hold it (no reco).

With all of these factors, the key question I have is - what am I missing that the market is seeing? Is the management integrity under scrutiny? Or is this just the aftermath and the burden of being an Axis MF holding? Would love to know the thoughts of fellow VP members here.

Markets seem to be in hammering mood, so i guess nothing will be spared.

But in the backdrop of growing protectionism across the globe, dependence on a foreign country for its key raw material may not seem overblown. Could that be applicable here… If not, i agree Continental is available and its big to be able to successfully compete with Nescafe

This is a foray by the Company and its subsidiaries into a

new product category which is outside coffee. Progressing on the vision of the Company to

be a house of brands, this is our first step.

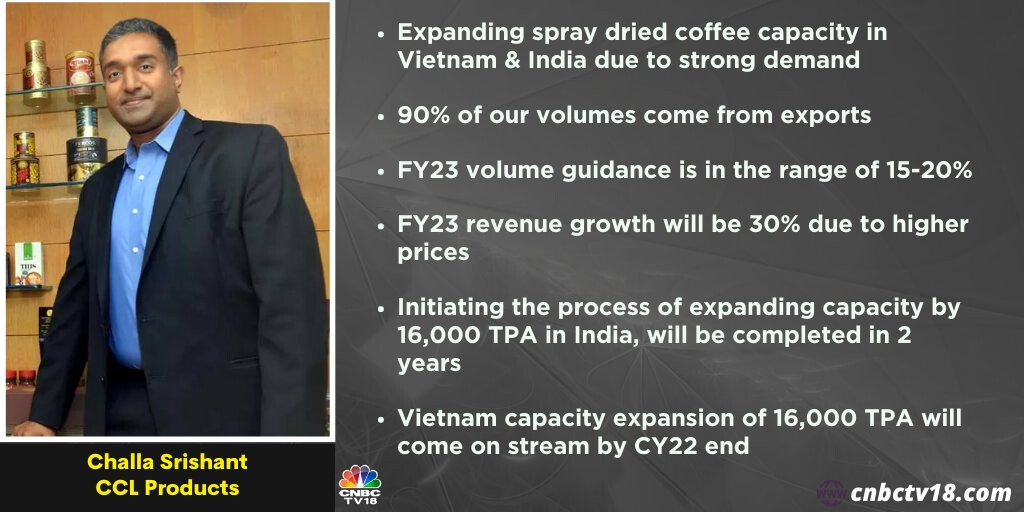

Expanding spray dried coffee capacity in Vietnam & India due to strong demand. FY23 volume guidance is in the range of 15-20%, revenue growth will be 30% due to higher prices, says Challa Srishant of CCL Products

Having read the whole thread and also studied this company otherwise, I have 2 questions

what led to the earlier CFO, Mr Sarma leaving the company? It dint look like a regular retirement exit as he has joined another company/ family run business. And a follow up to that is, there is close to no information about the current CFO, Mr V. Lakshmi Narayana. Nothing comes up on a regular search or even linkedin. Can someone share some light on this?

The promoter remuneration is higher than recommended, and as much as I have read so far, Mr. Srishant’s role is very clear in spearheading the company while there is no clarity on designation/responsibilities/ role led by Mr. Mohan Krishna. Mr. Srishant and Mr. Mohan Krishna bag the highest salaries and they are also related (brother in law). I would like to know if I’m missing something here.

I could be wrong, but I am sensing you are looking at the business from your profession perspective. It is not incorrect per se, people give a lot of thought about the who run the business, and at times, it even becomes a very important reason to invest or not to invest, for example when there is visibility of succession in sight.

But your questions to me seem to be asked because of your education, despite reading the whole thread. My limited answer to your questions is that look at the people and their decisions in the context of the business, look at the business, its growth, its profitability, its expansion, its limitations, valuation given by the marker over years, institutional participation etc.

You can even get benefited by understanding about the people who run the business, but even then business comes first, they cannot defy the nature of the business, particularly with CCL like FMCG businesses, wherein the end users’ psychology plays a part in the growth of the business, but this has to be reflected in the numbers, because we may be right, but we don’t move the price, we go along with the price.

They are trying to increase their retail business also. I personally like their premix coffee. It is much better in taste. The quality they are producing is top notch. Other companies are selling lower quality of product at higher price. CCL is extending its premix capacity. B2C business is high margin business. Company is likely to increase its share in the market.

The capacity addition plans for CCL provides good visibility for potential growth in the coming years:-

Currently at 37500 Tons, they are planning to add 16000 Tons in Vietnam (coming on line this quarter) and 16000 Tons in India (coming on line end of calendar year 2023). Additionally, they have also added 6000 Tons of Freeze Dried Capacity in Vietnam (in 2024). In total, this will take them up to ~76000 Tons from 37500 Tons in the next ~1.5/2 years

This is a cost plus model and if coffee/prices go up/down it does not really matter. They make money on more volumes as they charge in EBITDA/Ton. The management is guiding 15-20% growth for next year in volumes with the new added capacities.

This quarter should be the first one where we will see the effect of the first new capacities coming on board. Vietnam additional capacity was commissioned in Q3 as per the concall, and we should see commercialisation in Q4 FY 23. Additionally, they took some plant shutdowns in Q3 to put the lines in place, and hence hopefully Q4 should be much better than Q3 in terms of volumes/EBITDA.

Consumer business setup is also an interesting part of the story covered in detail in above thread. As per last concall, it is growing and has broken even now. It will be interesting to see how this element plays in and supports the potentially strong growth in the the B2B business.

Valuations/charts all reflecting strong growth expectations. Will be interesting to see if they can deliver.

Disclosure: I am invested and biased. This is not investment advice, I am not a registered advisor.

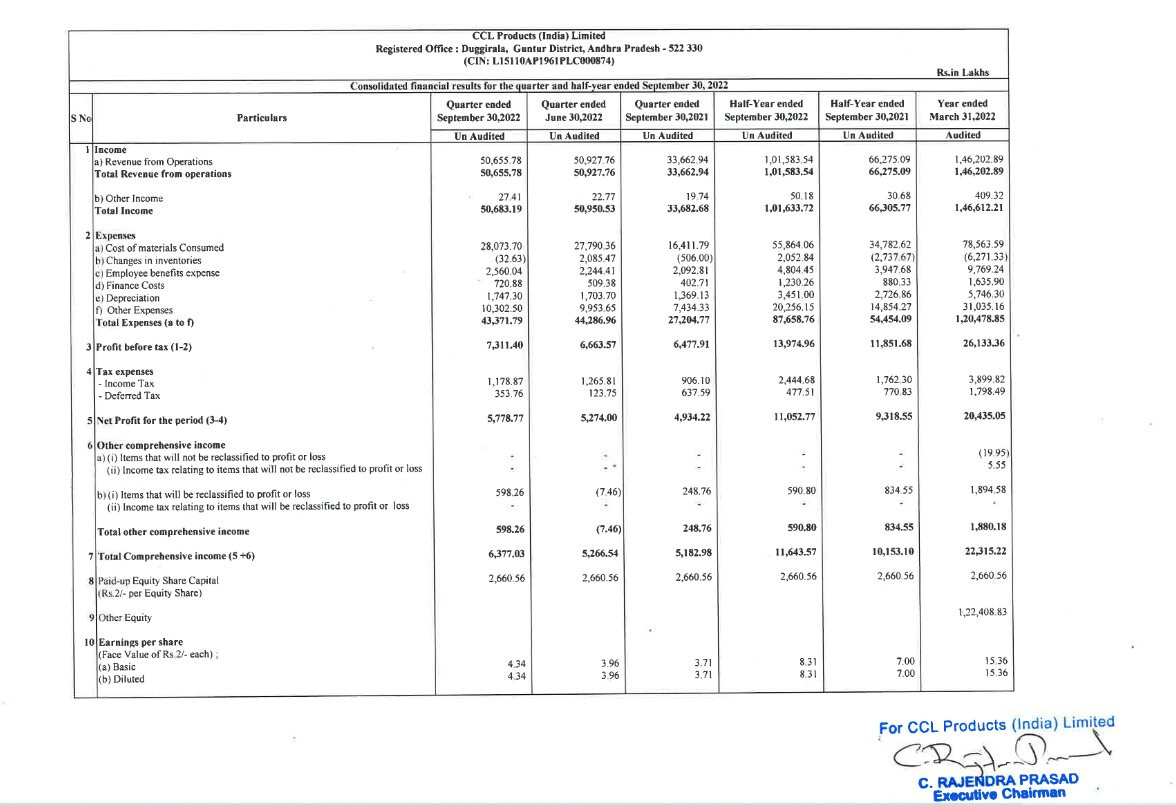

Company came up with good set of numbers

PAT already at 269Crs (although on back of lower tax rate which would increase from coming qtrs)

Vietnam capacity now at 30K MTPA , mgt. expects to utilise 50% of additional (16k MTPA) in FY24.

domestic retail business did 150-160Cr business also making profits now

The conference call was hosted by Nirmal Bang Equities Private Limited.

The call was attended by various analysts and representatives from the company.

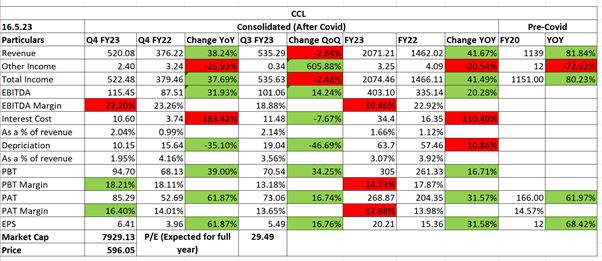

The company achieved a turnover of INR520 crores for Q4 FY23.

The company achieved a turnover of INR2,071.21 crores on a year-to-year basis

The net profit for the corresponding previous year was INR204.35 crores

The company’s EBITDA is INR403 crores and profit before tax is INR305 crores

The company plans to put remaining free cash flows into ongoing projects and building capacities.

CIS countries contribute almost 20-25% to the company’s volumes.

The expected volume growth for the next year is around 20%.

The company’s revenue is broken up into different geographies.

The company’s volume growth for the quarter and the year was consistent at around 20-25%.

The expansion in Vietnam led to growth in EBITDA this quarter.

There was no contraction in demand during the COVID period.

The company operates mostly with clients who consume instant coffee at home.

The freeze-dried capacity is 100% full for the next one and a half years.

There is no apparent demand contraction going forward.

The turnover for the whole domestic business in FY '23 was around INR 50 crores.

The projected growth momentum for this year is between 30% to 40%.

The EBITDA growth is always in line with the volume growth.

The new crop in Brazil should result in lower coffee prices, but robusta prices have increased due to high demand.

The increase in arabica prices has caused a transition towards robusta, which has also put pressure on robusta prices.

Coffee prices are currently at an all-time high, but are expected to soften once new crops come in from Indonesia and other regions.

The company is expected to complete the trial operations and start commercialization by the third quarter of '25

EBITDA per kg for spray-dried and freeze-dried products is in the range of 90-100 and 130-140 respectively

Long-term perspective should be considered when looking at volume growth and EBITDA growth

The business had a 25% growth rate this year.

The projected growth rate for the next two to three years is 30% to 35%.

The growth rate may be affected by competition and other factors.

There was not much of an increase in expenses from Q3 to Q4.

The volume growth was almost around 20% on a Y-o-Y basis.

INR320 crores is expected to be rolled in the form of debt funding for the new safety capacity facility in India.

Niche products like Cold Brews or Specialty Coffee contribute 5% to 10% of the company’s volumes

The small-packaging unit has a capacity utilization of 50% to 60%

The company gets 10% to 15% additional margins due to value addition from the small-packaging unit

The U.S. market contributes 10% to 12% of the company’s business

The company sources coffee from different origins depending on factors such as the blend and the client’s preferences.

The realization benefit does not depend on the origin of the coffee, but rather on a complex set of factors.

The company outsources coffee to meet higher demand and production constraints.

The India business had a revenue of INR250 crores, with INR150-160 crores from the branded business and a growth expectation of 13% to 25% in the next two to three years.

The Greenbird expansion is slow, but they have expanded to six cities and plan to expand to three to four more soon.

The company is currently focusing on coffee and Greenbird, but evaluating other categories to enter.

The CEO does not expect a lot of profit generation as they plan to keep investing in the business and expanding into other categories.

The effective tax interest rate on working capital is around 6%

The interest rate on term loans is likely to be around 8%

Depreciation is expected to increase by around INR7.5 crores per quarter

The company experiences a regular churn of clients, with around 40% being new clients and some old clients switching to new products.

20% of the company’s business comes from traders and middlemen looking for cheaper coffee.

The company is commissioning a pilot plant and participating in specialty coffee fairs to increase its play in the premium and specialized coffee segment.

Capacity constraint and price are the primary reasons why deals may not go through.

The company is building a new Freeze Dried capacity in Vietnam to address the capacity constraint issue.

The value addition percentage for companies in the instant coffee market depends on various factors such as processing cost, packaging cost, logistics cost, and brand strength.

The company’s market share in the instant coffee market is around 5%

The Indian coffee market is predominantly in South India

The company focused on the South Indian market initially and is now expanding to other cities and towns

The brand intends to use D2C platforms like its own site, Amazon, Flipkart, and Big Basket for sales.

The strategy for the India market is to build distribution in the South market and use D2C platforms for sales.

The brand plans to expand its business in the South market by increasing distribution to smaller outlets and increasing their play in plain sachets and small packs.

The global market for instant coffee is estimated to be around 9 lakh metric tonnes, with the brand’s addressable market being around 4-4.5 lakh metric tonnes.

The brand aims to double its volumes in four years and maintain a CAGR of approximately 18-20% volume growth.

The company has set a goal to expand their business in the next three to four years.

Vietnam operations are expected to contribute significantly to the company’s revenue growth, with around 40% of total revenue coming from Vietnam in FY2023.

The Vietnam capacity of 16000 metric tonne has been utilized, and the new capacity which is coming up will be utilized by 50% in the current year.

The new expansion in India is expected to commercialize operation in Q1 of FY2024-2025, while the new freeze-dried capacity in Vietnam is likely to come into commercialization in Q3 of 2025.

The company is planning to set up a new facility in India with a capacity of 16000 metric tonnes SD, costing around 400 Crores, with the company contributing 80 Crores and the balance being availed in the form of debt.

Coffee prices are expected to slowly soften once the new crop starts coming in from Indonesia and other regions.

Guidance: Volumes and Revenue both are expected to increase by 20% for FY24. The company aims to double its volumes in four years and cross 10% addressable market share globally in the next three to four years. The tax rate for next year is expected to be around 12%.

The company is looking to aggressively pursue the coffee vending business and is installing machines for large clients on a PAN India basis.

Is it fair to say that we just need to look at volume growth in such kind of businesses such as CCL products? Ultimately the business is very simple to understand. It is nothing innovative it is just coffee. Just having a good estimate of volume growth in future and current volume growth suffice to analyze such businesses? What other businesses are like these?

A lot of aspects pertaining to the business of CCL were discussed before in the thread, go through them, and you will get a better understanding of the business.

Things like distribution, competition, debt, geographical expansion, inflation, weather, regulation intervention and many other things also exist.

Hi @Lajja_Shah - Could you please throw some light on the debt scenario for CCL products, if you are tracking the business? It seems they have increased their debt position in Q1FY24.