What is the impact on CCL due to recent surge in coco prices?

High raw material price would increase working capital needs, hence increased debt and negative impact on p&l due to interest.

I think this is a short term pain and may last until mid FY25.

Fitch ratings revised outlook to negative, this report has more details

3 Likes

CCL-Products–Company-Update–17-Apr-2024.pdf (nirmalbang.com)

“Robusta coffee prices continue to make new highs on a daily basis.

Duration of future orders could be lower, say 3-6 months, thereby indicating lesser visibility than in the past.

While we remain positive, relatively lower demand visibility

and working capital debt overhang might offer a better entry point to

investors in the near term” - Nirmalbang’s view

4 Likes

hi folks!

I analyzed this business today by scrolling through the valuepikr threads only. I think thats a better option than reading through all concalls.

I know about the moats and cost-plus model of the business BUT

I have a quite neutral view of the business.

Cons:

-

Mediocre earnings growth

10 year Profit growth : 15% while

10 year stock returns : 25%

hence speculative returns : 10%2. Branded Coffee Business is just 7.5% of their total revenue

They commenced their branded coffee business around FY15 and they did around a revenue of 40 cr in the next year itself. Today their revenue from branded business stands around 200 crores which is around 7.5% of their total revenue.

I think it is very insignificant right now and I guess this part of the business had been the thesis for most of the investor community.

We have to see how it grows up. In my view, it might stay <10% of the total revenue in next 4-5 years. will be happy to be wrong here.

*Pros, not so pros: *

3. Its a slow, boring and compounding business. Honestly, a very good business to own for long term which gives you 15% compounded annual return with minimal downside because I believe the valuation multiples are hovering around their averages.

Also there is an optionality of branded business doing well and valuation re-rating because of that but that might come over 7,8 or 9 years in my view. A lot of patience is required for that.

Conclusion:

One can think of this as a defense stock.

Disc : I am not invested in CCL Products

7 Likes

3 Likes

Q1 FY25, Concall notes - Excuse for any mistakes:

- Revenue growth is around 18% yoy

- Volume growth is 15 - 16%, Maintain the volume growth guidance of 10 - 20% for the whole year.

- EBITDA growth is also around 23% yoy, EBITDA growth is driven by high value contracts being executed vs base. This is temporary and but will look to improve margin profile may be after a 1.5 or 2 year period.

- PBT growth is around 25.5%.

- PAT growth is around 18%

- Domestic market gross turn over is 90.5 crore (11.6% of total revenue), 65 crores out of that is branded sales.

- Branded business is growing at 45 - 50%, also expanding distribution and all channels. With volume growth of 30%+.

- Branded business is currently focussed only in south India, having good traction in 5 lakh + population towns. Expanded to Metros with 1000 - 1200 outlets.

- Overall India business targeting at 400 crore and branded business targeting at 300 Cr by End of Year.

- Looking to get 7 - 8% EBITDA margin for the branded business this year. This has broken even last year itself.

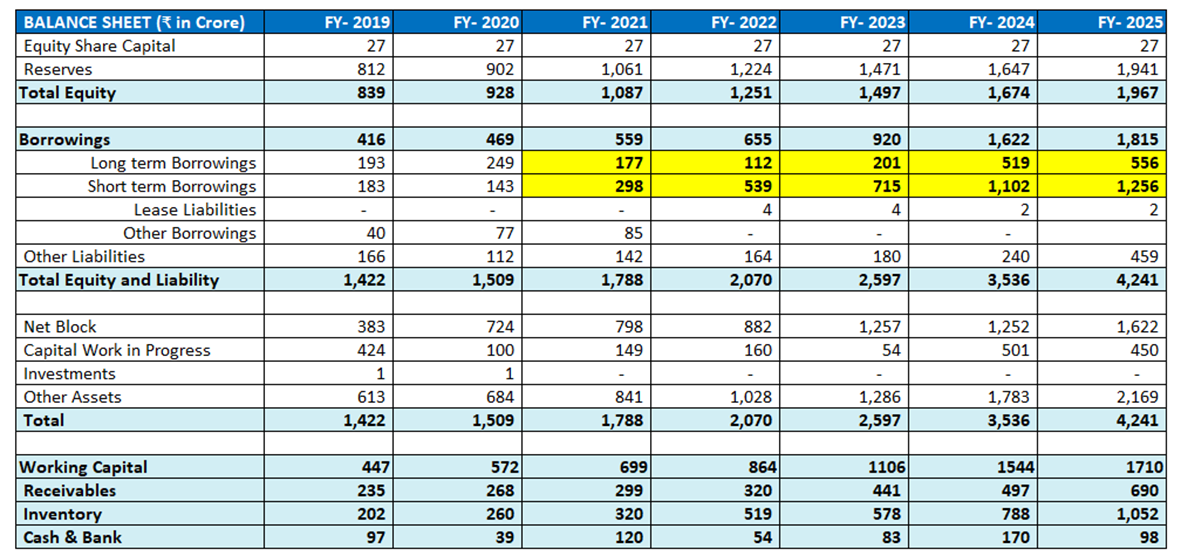

- Gross debt is at 1885 Cr: 1200 Cr is working capital and 675 Cr is term loan. Expect it to go to 2200 Cr assuming current price with volume growth.

- Cost of funds will be at 8.25% from July for 1200 Cr working capital

- Rough revenue breakdown:

- 40% from Asian markets

- 20 - 25% from East Europe market

- 15% from Western Europe and UK

- 10 - 15% from US and balance from South America, Africa, Australia and New Zealand.

- No inventory build up yet seen on client side, coffee prices are at pretty high levels.

- Need to watch out the next coffee crop yields in Vietnam and India, which we will get to know by November / December.

- Long term contracts are not yet revived at elevated price, there is wait and watch to see things settling down.

- Capacity Utilization:

- India: Capacity excluding food and beverages is running close to 100%, but F&B should be just 5 - 10%.

- Vietnam: First line is running at full capacity and second one at around 50% capacity

- Margin drivers: Value added products - Small packs and speciality coffee. Sweetest - speciality coffee in small pack

- Small packs - contributing close to 20% of total units, from single digit 4 / 5 years ago.

- UK business: Percol business is being ramped up, looking to get the listings back, it is seen as environmental friendly brand.

- Coffee Prices:

- Brazil coffee prices are much lower and producers there are having some advantage, both in price and logistics

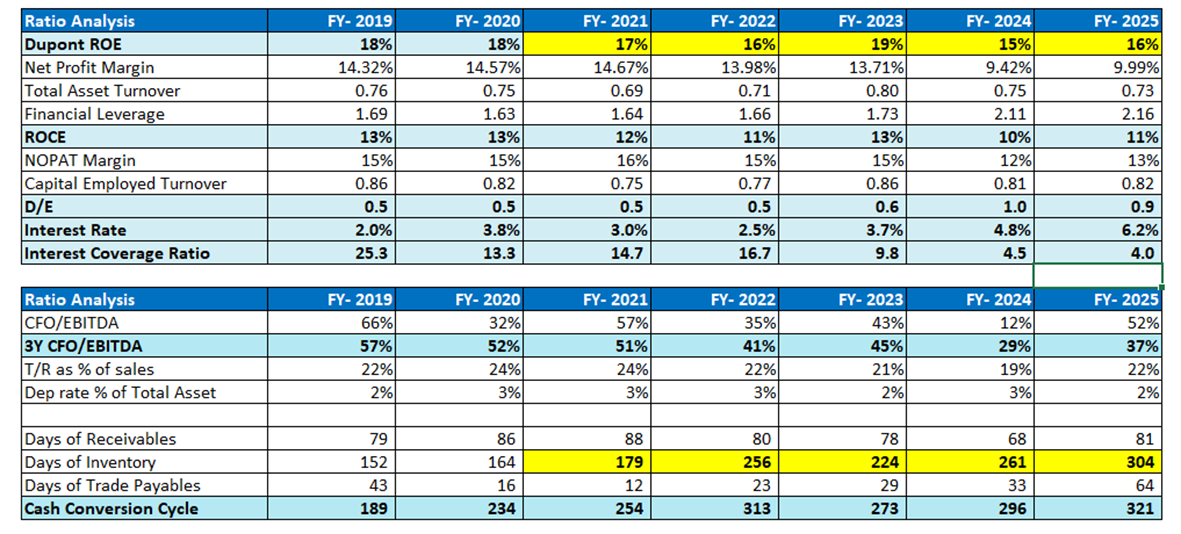

- Inventory days have gone up to 180 days from 120 days earlier, because we are buying from Brazil market and it takes longer to get the shipment, which is helping in margin but having impact on finance cost.

7 Likes

One more thing to add is that CCL has started a few cafes as a Proof-of-Concept (POC) which is a pure play D2C business.

The way management approached this was quite prudent. They started off with few Continental trucks and then to a few outlets in colleges and metro stations and now to a full fledged cafe. The journey taken to prove the concept is probably ready while creating brand visibility. Hopefully this is not a start to an end but a step towards a new beginning. Market may see this as a good opportunity only if the return ratios align well. If the POC gets validated in a year or so this could well be a significant step towards a new line of business. Starbucks is talking about opening 600 new stores by 2028. Starbucks is still in the red after opening 421 stores with a turnover of 1218 crores.

CCL is an prudent management but a scale up with already high debt on books would be a significant challenge but management has got the timing right for the D2C foray.

7 Likes

When asked, the founder(s) of Third Wave coffee chain, as to why they start their branch almost next to, or in the vicinity of StarBucks which is intuitively opposite in logic, they said : due to SB being present, the coffee drinking crowd is already drawn to the location, the captive audience is homed in - all we have to do is capture their final steps, and induce them to our outlet - by being unique in our way.

Remains to be seen how CCL go about building their branded cafe shops. It is not easy - CCD has shown how treacherous rapid expansion is.

5 Likes

stores of their own is too much of a jump and not an easy diversification to manage, best to be very very cautious, esp when macros are against them (high coffee prices) and they have high debt to service, which means they are ill placed to fund burn

current situation of coffee crop and scope of expansion

2 Likes

If anyone tracking coffee industry. this would be helpful.

1 Like

got a good bump yesterday, market probably expecting red sea crisis will resolve and bring down the logistics challenges that CCL has been facing

Q4 FY25 Concall summary

- For the full year, the volume growth was around 10%. This is lower than previous year which was 20-22% growth as they deliberately avoided taking on too many low-margin contracts which also helped increase EBITDA per kg in Q4

- Out of 440 crores sale from India, 300 crores come from branded products.

- Growing through various verticals - Exports (B2B and private label), Domestic Market.

- Developed economies are already highly penetrated (now need to gain market share) while developing economies are the future drivers in coffee consumption ( double-digit growth in the coming years)

- Aims for their profitability to grow at a CAGR of 15% to 20% year-on-year over the long term with their domestic branded products, are expected to grow even faster than the overall company average.

- Operates on a cost-plus model. This means they add a fixed profit margin on top of their production costs. Their main concern is unstable and fluctuating coffee prices and also the possibility of consumption decline if high prices deter consumers.

- Last 2-3 months, the prices have been stable for coffee however still high with management waiting for Brazil crop to see how future might be. Stability can help them have longer contracts which can help reduce working capital.

- In B2C, they do price hikes in larger packs while for smaller packs they do optimization like redoing blends, reducing weight per pack while committing to maintaining their profit margins in this segment. Small packs have crossed 20% of sales in contribution compared to last years 17-18% and they plan to increase this contribution by 2-3% more.

- The coffee industry in India, including CCL Products, has increased prices on larger coffee packs by about 30% to 35% over the last year.

- Reasons for increase in debt :

- Huge increase in green coffee bean prices (from $1000 to $5000 in a span of 5-10 years) which has lead to higher cost of holding inventory.

- Due to upward movement of these prices, the coffee market has shifted to a Seller’s Market. This means the supplier has more power than CCL, often demanding quicker payments or shorter terms and hence, CCL has to secure supply immediately to avoid unfavorable terms.

- About 1150 crores of the total debt is for working capital while the rest long-term loans are used for expanding their production capacity. They invest in expansion every 6-7 years, which temporarily increases debt.

- Over the next 3-4 years the company expects debt levels to come down significantly - by repaying their long-term expansion loan and if coffee prices go down, it’ll give them even more operating leverage.

- Their working capital debt is primarily for confirmed contracts which means they secure inventory only for secured contracts.

- Regarding tariffs, there are positive signs that both India and Vietnam are in a good position to finalize trade deals with the U.S.

- In B2C, there is some short-term stress and slowdown in demand from consumers due to high prices.

- Strategies for growth:

- Increase Private Label Consumers

- Penetrate Newer B2B Markets like China, Taiwan

- Grow Domestic Branded Segment in B2C

- If coffee prices drop significantly, might take on more low-margin business to boost overall volumes which will be lower EBITDA margin. Focus and guidance remain on overall absolute EBITDA growth of 15% to 20% year-on-year.

- If one country becomes less favorable due to tariffs, have the option to supply from the other country.

- Older capacity is running at 100% utilization, for newer capacities it’s around 10-15% on a yearly basis

- Reason for higher inventory :

- They buy from multiple sources - supplies from Vietnam and Indonesia are closer to their factories, while buying from Brazil involves much longer transit times.

- They also face challenges with local farmers/aggregators in a rising price market.

- The inventory split is majorly green coffee beans heavy which can be approx. 3 months stock while finished good stock is roughly 15-20 days of stock

Disclaimer: Studying and Tracking

17 Likes

- Lot of outsourcing is visible wrt companies catering to Coffee segment especially the likes of CCL products.

- CCL should ideally grow better vs other peers

- Operating leverage + Vietnam capex which is live

- Holding cost reduces for CCL coz of Vietnam angle Vs a similar player moving inventory via Brazil

- Guiding 15-20%Volume growth.

- Just like insurance player – new entrants might face a lot of issues scaling to CCLs level

- Freeze dried Coffee + Coffee prices not as volatile in the recent past

Single most contributing factor was coffee prices. No one in B2B loves to enter into contracts when Coffee prices are volatile.

- “The single most contributing reason [for higher debt] has been the prices… For the same amount of coffee itself, I will have to… spend 5 times more money.”

- Higher inventory days partly due to increased procurement from Brazil (longer transit times vs Vietnam/Indonesia).

3 Likes

The US is to significantly cut tariffs for several Vietnamese products - Vietnam State Media

Vietnam Leader in phone call with Trump asks US to recognise Vietnam as market economy

Vietnam leader To Lam, in phone call with Trump, asked the US to remove restrictions on exports of high-tech products to Vietnam

- Vietnam’s improving global trade positioning will benefit CCL’s largest expansion.

- Management projects 15–20% annual EBITDA growth

- Massive Capacity Expansion Backed by Capex

Also coffee prices falling helps CCL manage contracts and WC

10 Likes

PPFAS TaxSaverFund, the ELSS fund of Parag Parikh has taken a small 0.29% exposure to CCL as per the PPFAS May 2025 factsheet (most recent one).

It’s not on PPFAS Flexicap yet though.

As a consumer, find good value in a CCL product over a Nescafe anyday.

Interested in a tracking position to begin with, closer to the 52 week low levels.

9 Likes

Well said but yes the thread is vey rich to learn ,seeing the journey of the company growing twenty times and the people who were able to ride journey with the company , so much to learn

3 Likes

One day, while I was having my coffee and scrolling through a news app, I came across an article saying that coffee prices were falling and that the earlier issues in the coffee industry were largely behind us.

As an analyst, this got me thinking it could mean an easier working capital cycle, a stronger balance sheet, and better P&L for companies in the space. Basically, good news for the overall industry.

With that in mind, I started reading more about the coffee sector and ended up buying CCL. That’s why I’m discussing this. I own the stock, so yes, my view might be a little biased.

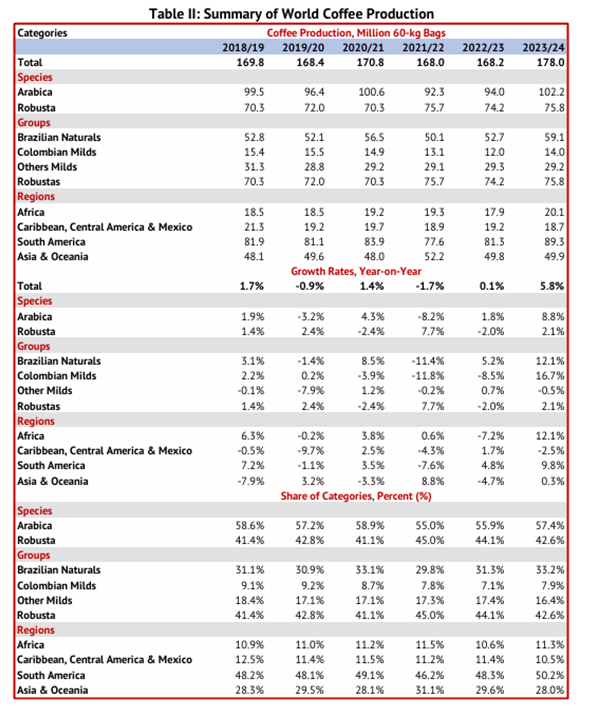

Global Coffee Trends: A Volatile Market

The global coffee market has been quite volatile lately. Prices are swinging due to a mix of factors climate change, supply-demand imbalances, rising production costs, and even geopolitical issues.

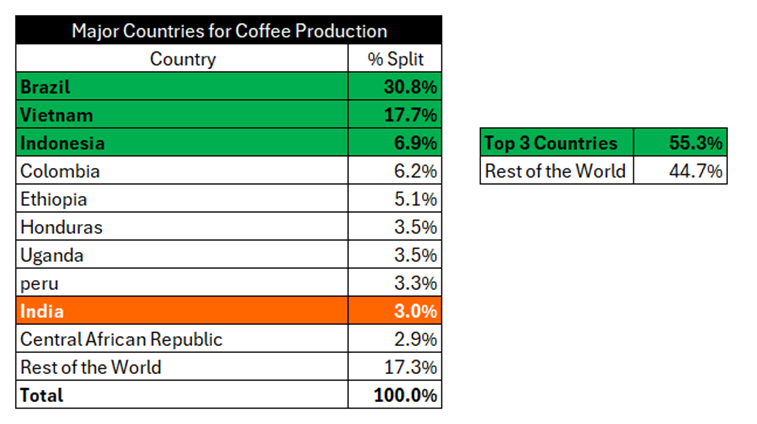

Brazil, Vietnam, and Indonesia together account for around 55% of global coffee production, and there have been some disruptions in these regions in the recent past.

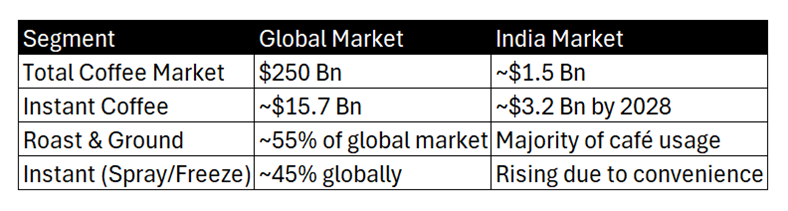

Industry Size & Segments:

Basic Coffee Value Chain:

Green Bean Cultivation → Primary Processing → Drying → Milling → Grading & Sorting

Roasting (crucial to flavor profile)

- Spray-Dried : Cheaper, mass-market, lower margin

- Freeze-Dried : Premium, better taste, higher margin

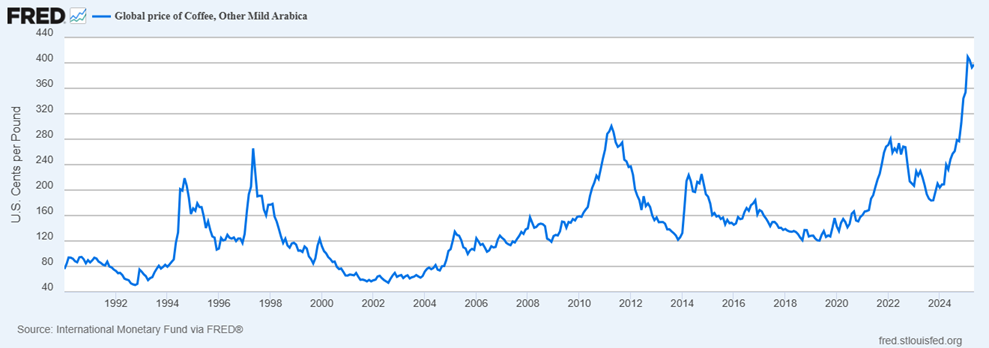

Coffee Price History:

Driving Factors

1. Supply and Demand

- Supply: Coffee production in key countries like Brazil and Vietnam often sees sharp ups and downs. Extreme weather especially droughts and frosts in Brazil can seriously hit crop yields.

- Demand: At the same time, global coffee consumption is steadily rising, particularly in emerging markets where coffee culture is catching on fast.

2. Climate Change

- Climate change is a major challenge for coffee growers. Rising temperatures, unpredictable rainfall, and more pests and diseases are all affecting crop yields and bean quality.

- Many farmers are being pushed to shift to higher altitudes in search of suitable land but that land is limited, which can hurt their livelihoods and raise production costs.

3. Geopolitical Tensions & Trade Policies

- Political instability in coffee-producing countries can disrupt supply chains and drive price volatility.

- New trade regulations, like the EU’s Deforestation Regulation (EUDR), add pressure exporters now need to prove their coffee isn’t from deforested land, which complicates logistics.

4. Rising Production Costs

- The cost of fertilizers, pesticides, and labor is going up. Add to that global factors like the Ukraine war affecting fuel prices, and it’s clear why coffee farming is getting more expensive.

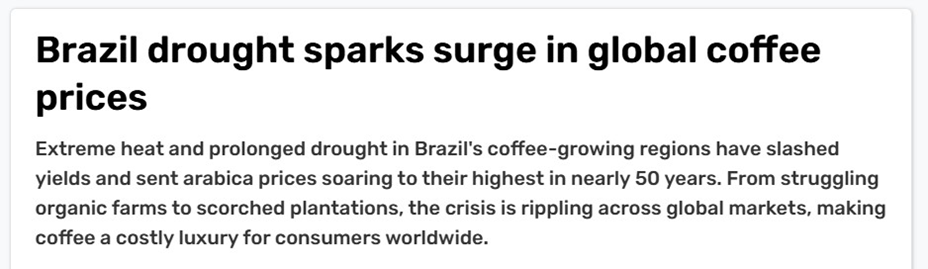

Why Coffee Prices Have Risen Recently

The recent spike in global coffee prices is due to a mix of factors that have tightened supply and added to market volatility.

1. Supply-Side Challenges

- Extreme Weather: Major producers like Brazil and Vietnam have faced harsh conditions in recent past. Brazil, the world’s largest coffee grower, has seen both droughts and frosts, which hurt yields. Vietnam has also dealt with droughts and floods, affecting Robusta production.

Source: India Today

- Lower Output: These weather events, along with labor shortages in some regions, have led to lower overall coffee production.

- Thin Stock Levels: Brazil’s coffee reserves are running low. A large portion of the recent harvest is already sold, leaving very little stock before the next cycle.

2. Rising Demand & Market Speculation

- Stronger Global Demand: Despite supply issues, coffee demand is still rising—especially in emerging markets across Asia and the Middle East adding further pressure to already tight supply.

Source: INTERNATIONAL COFFEE ORGANIZATION

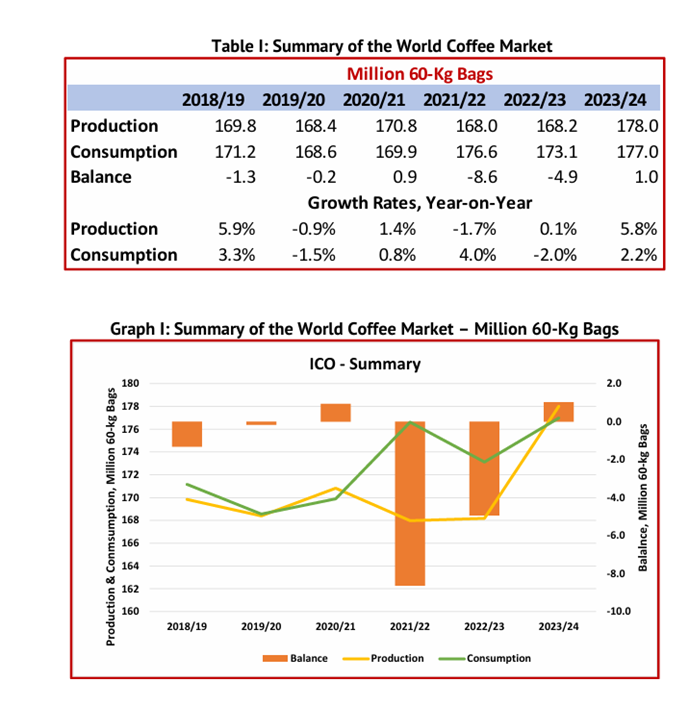

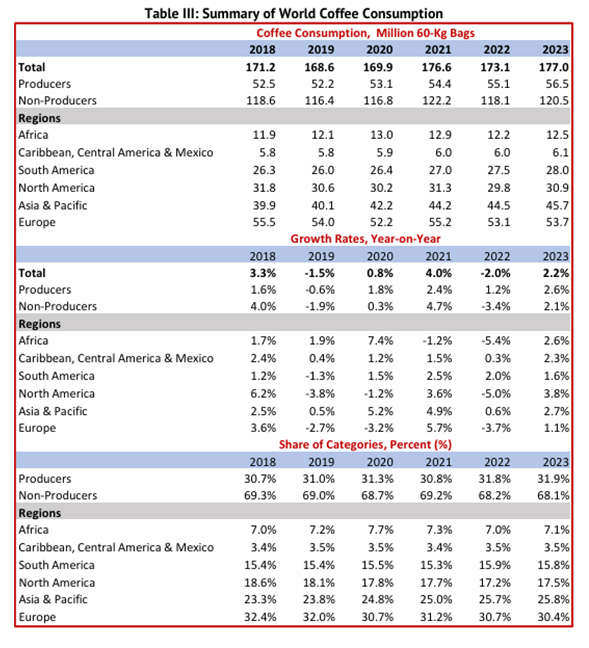

Let’s see Historical Production vs Consumption Pattern

Source: INTERNATIONAL COFFEE ORGANIZATION

- Speculative Activity: Traders betting on coffee futures have added to the price surge. Even when supply isn’t severely constrained, speculation can exaggerate price movements.

3. Higher Production Costs & Other Pressures

- Input Costs Going Up: Fertilizers, pesticides, labor, and transport have all become more expensive. These cost increases are often passed on, raising prices at the consumer level.

- Currency Movements: In some producing countries, local currencies have weakened against the US dollar. This raises the cost of imported inputs, pushing production costs—and ultimately prices even higher.

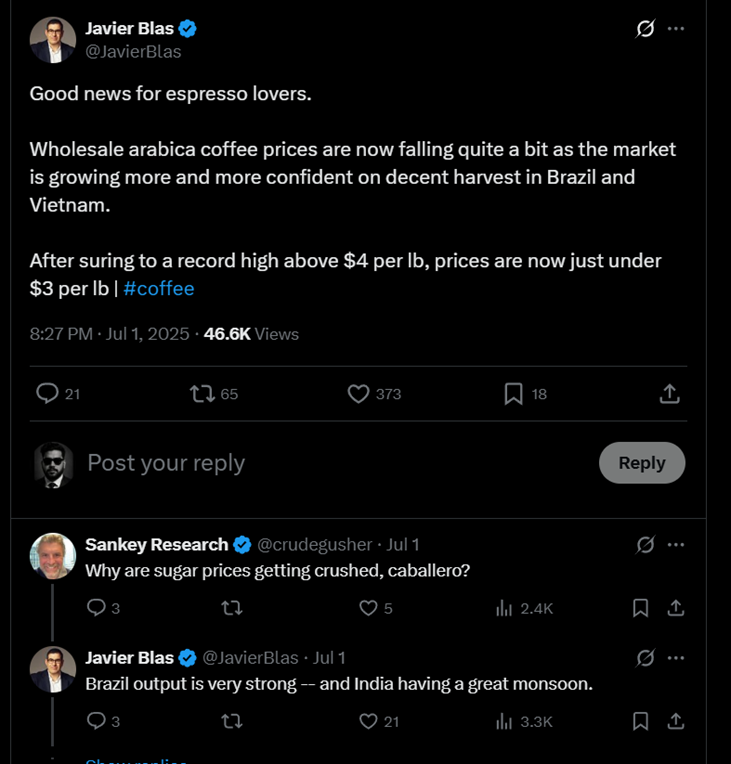

Coffee’s Getting Cheaper Again—But Why?

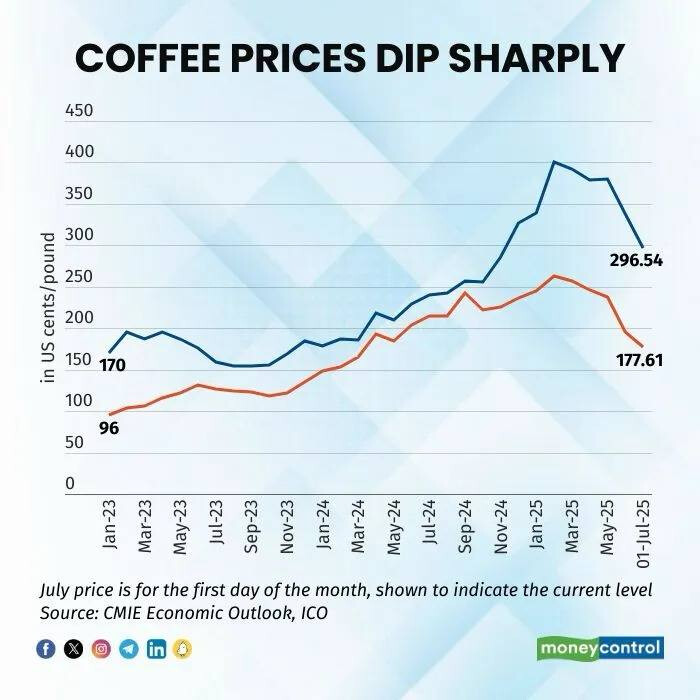

Yes, coffee prices have dropped recently after a long stretch of steady increases.

What’s been happening:

- The global coffee price index (I-CIP) fell by almost 12% in June 2025 going below 300 cents/lb for the first time since late 2024.

- Both Arabica and Robusta futures dropped too Arabica hit a 5-month low, and Robusta went to its lowest point in over a year.

- Robusta especially saw a sharp fall down 17.5% in June alone.

Why it’s happening:

Source: https://x.com/JavierBlas

- The main reason? Supply is looking better.

- Brazil and Vietnam are expecting bigger harvests this year, and the weather has been a lot more favorable than last year.

- Coffee inventories are also rising stock levels for both Robusta and Arabica are at multi-month highs.

- On the demand side, concerns have eased a bit, and speculative traders have pulled back too so prices are settling.

But it’s not all clear:

- Weather can still flip unexpectedly, especially in Brazil and Vietnam.

- There are also ongoing issues with logistics and shipping in some regions.

- And Brazil’s stockpiles, while improving, are still running low.

So while prices have cooled off for now, things could change quickly depending on how the next few months play out.

Why I’m Betting on CCL Products?

↓ Lower coffee prices → ↓ Working capital needs → ↓ Short-term debt → ↓ Interest cost → ↑ PAT & EPS

- New capacity & better utilization → Bottom line grows faster than top line

CCL Products Ltd:

CCL Products Ltd. is an Indian company that has quietly become one of the world’s largest makers and exporters of instant coffee. What started as a small plant in the 90s is now a global operation that serves over 100 countries and manufactures coffee for some of the biggest brands in the world.

History:

- The company was founded in 1994, and it started commercial operations in 1995 with a small spray-dried coffee plant of 3,600 tons.

- It was started by the current promoter’s father. Mr. Chalash Rishant, the current MD, has been instrumental in scaling it up over the years.

Early Setback

- In its early days, CCL tried a joint venture with Jyothy Labs to scale its B2C play using Jyothy’s distribution. But the venture didn’t take off as expected and was shut down

Plant

| Country | Type | Capacity |

|---|---|---|

| India | Spray + Freeze | ~60,000+ TPA |

| Vietnam | Freeze-Dried | ~17,000 TPA |

- CCL’s capacity has grown 15x over the last two decades from 3,600 tons in 1995 to 77,000 tons in 2025.

- The real growth picked up after 2015. In 2015, capacity was 18,600 tons. In 10 years, that has jumped more than 4x.

- What’s more impressive? They’ve done all this without diluting equity. The entire expansion has been debt-funded, showing strong confidence and control.

Business Model & Segmentation:

CCL Products Ltd. operates primarily through two distinct business segments: Business-to-Consumer (B2C) and Business-to-Business (B2B).

1.B2C (Business-to-Consumer) ~8–10% of Revenue (target 20–25%)

CCL launched its own brand, Continental Coffee, in 2022. This is a natural next step—selling directly after mastering production for decades.

Why B2C?

- Higher margins: Consumer brands have better pricing power.

- Built-in industry connects: CCL leverages existing coffee relationships and expertise.

- Innovative offerings: Includes unique flavored sachets (e.g., hazelnut) and regional blends like Malgudi and Chikori.

India Strategy

- Focused on South India (70% of India’s coffee demand).

- Distribution:

- 100,000 retail outlets

- 4,000 vending machines

- In-house cafes/kiosks

- Market share:

- <5% pan-India

- Low double digits in South India

- Growth: ~40% CAGR in recent years

- Goal: Scale B2C to 20–25% of total revenue

2. 2B (Business-to-Business) ~90% of Revenue

This is the backbone of CCL. They manufacture instant coffee (spray-dried and freeze-dried) for global brands and retailers. Most of it is exported to North America, Europe, Asia Pacific, and Russia.

Why brands choose to outsource to CCL:

- Full-service platform: CCL offers over 1,000 coffee blends (Arabica, Robusta, spray, freeze-dried) making it a one-stop shop for global customers.

- Cost-plus model: Clients pay CCL a markup on costs. So, even if coffee prices go up, CCL’s profit per kg stays stable.

- Focus advantage: Brands can focus on branding and marketing. CCL takes care of the manufacturing complexity.

- No plantations: CCL avoids owning farms staying asset-light and sourcing beans globally.

- High switching costs:

- Custom blends and recipes are confidential.

- New supplier onboarding takes 6–12 months of quality testing and costs.

- Wide client base: 400+ clients worldwide; no single customer contributes >10% of revenue.

- Exclusive supplier: For many Indian coffee chains, CCL is the sole source.

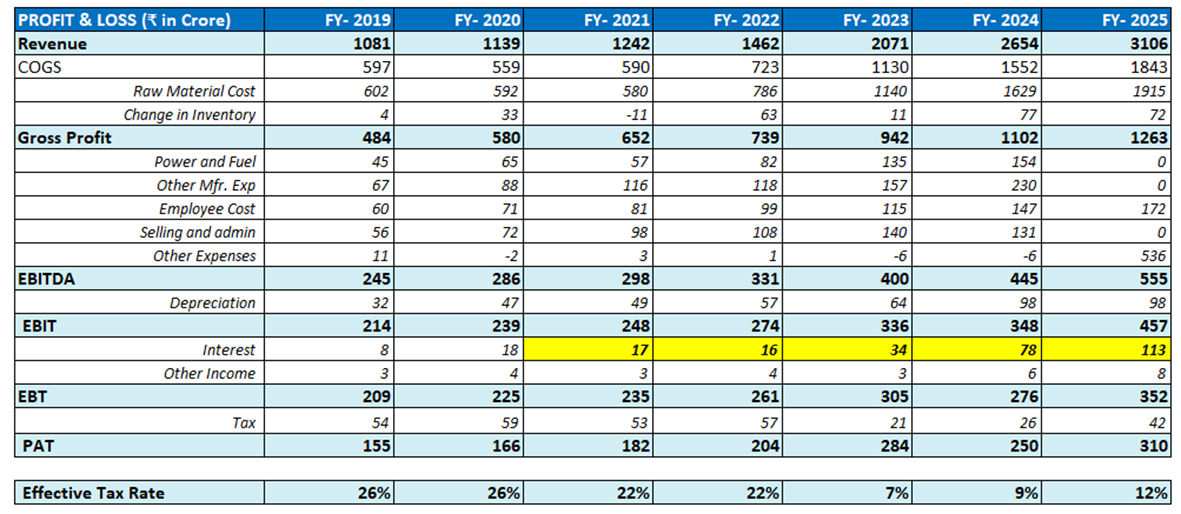

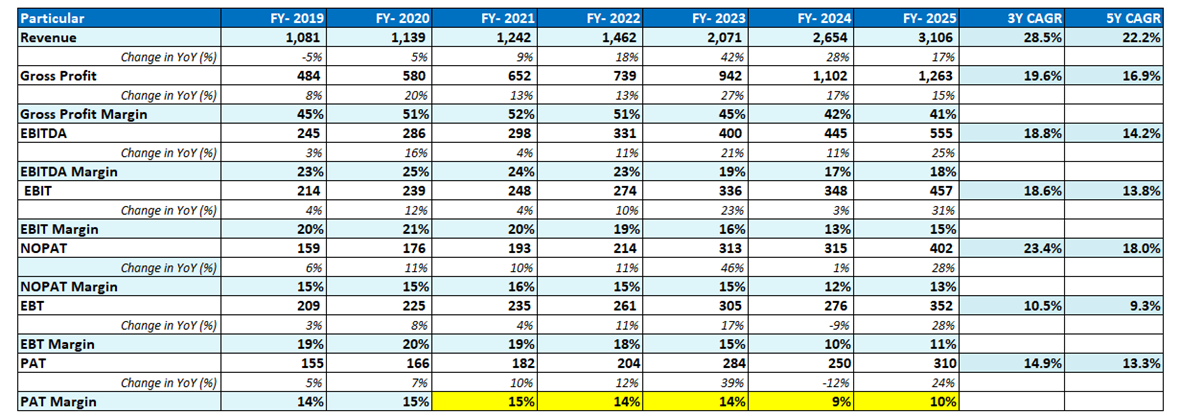

Financials Statement Analysis:

2021–22: Brazil/Vietnam drought → 5x price spike

High volatility = Shorter contracts = Higher inventory = WC pressure

Management Quality:

CCL’s management isn’t flashy—but they’re quietly building one of the world’s largest instant coffee platforms through clear strategy, discipline, and deep understanding of the business.

- Chalash Rishant built it from scratch; CEO Pravin Japury (ex-F&B) is scaling B2C smartly and frugally.

- Conservative yet ambitious: targeting 15–20% annual growth, not chasing headlines.

Disciplined Growth, Zero Dilution

- Capacity grew 15x in 20 years, all debt-funded not a single share diluted and strategically used

- They only expand when capacity hits 85%+ utilization and customer demand is confirmed.

Low-Risk, High-Stickiness B2B Model

- Core B2B business runs on cost-plus contracts → protects margins from coffee price swings.

- No plantations → asset-light and focused.

- High client stickiness: 1. Custom blends (confidential), 2. Long onboarding (6–12 months)

B2C – Big Optionality

- Focus on South India, vending + retail push (4,000 machines, 1L+ outlets).

- Differentiated SKUs (hazelnut sachets, Malgudi blends).

Q4-FY 2025 CCL Products (India) Ltd Con-call Analysis:

1. Business & Financial Snapshot – FY25

Strong topline growth, better margins even with coffee cost pressures

- Revenue crossed ₹3,100 Cr (↑17% YoY), hitting a key milestone.

- Net profit grew 24% YoY to ₹310 Cr; EBITDA jumped 25% to ₹564 Cr. Margin boost in Q4 came from a richer contract mix.

- Volume growth slowed to ~10% (historically ~20%+), showing a shift from chasing volumes to chasing value.

- Q4 saw a spike in EBITDA/kg thanks to high-margin contracts and end-customer sales though management says this may not sustain every quarter.

- Working capital borrowings rose to ₹1,150 Cr (part of total ₹1,800 Cr debt), largely due to a 5x jump in green coffee prices from ₹1,000/kg to ₹5,000/kg.

2. Segment & Strategy Overview

Well-balanced B2B/B2C play; doubling down on India; innovation driving premiumization

- B2B International (~85% of revenue): Europe and US are steady (flat growth, but market share gains); faster growth expected in China, MEA, and Africa.

- India B2C: Out of ₹440 Cr domestic revenue, ₹300 Cr is branded sales led by sachets, e-commerce, and pricing tweaks on large packs.

- New launches: Microground coffee, cold brews, and customized blends (blend library now 1,000+). Tailored solutions = pricing power.

- Capacity update: Old plants nearly full; new Vietnam plant running at 10–15%, will ramp up gradually.

- Private label: 60–70% customers are long-term partners; pricing volatility is shortening contracts, but relationships remain sticky.

3. Outlook & Guidance

Focus remains on absolute EBITDA growth, not just volume push

- Guided EBITDA growth: 15–20% YoY; volume growth expected to stay around 10%.

- Cost-plus pricing and back-to-back raw material buying reduce volatility but make contracts shorter.

- Coffee prices are stabilizing—debt tied to working capital should ease in 2–3 years. Term loans (used for capacity) to be repaid in 3–4 years.

- Global expansion continues: gaining ground in China, Taiwan, ME, Africa. In India, long-term tea-to-coffee shift will power high double-digit growth.

- Freight/tariff challenges: Red Sea issues are inflating costs temporarily, but dual-country production (India + Vietnam) provides flexibility.

4. Key Risks

Managing coffee inflation and shorter contract cycles with tight planning

- Coffee inflation: Raw coffee jumped from 1,000 to 5,000 this pressures working capital and shrinks contract tenures.

- Debt stress: Linked to green coffee stocking, not operational strain. Brazil’s 60-day transit time forces ~3 months of buffer inventory.

- Tariffs/geo risks: Mitigated via sourcing flexibility (Vietnam, Brazil, Indonesia) and dual-location setup. US–India tariff outlook improving.

- Customer caution: Buyers avoid long contracts but CCL’s immediate raw material procurement reduces mismatch risk.

- India B2C challenges: Price sensitivity in sachets company using smart packaging and blend tweaks to preserve margins.

5. Analyst Q&A – What the Street Asked

Analysts focused on sustainability of margins, contract visibility, WC impact, and future growth

- Growth drivers: Where’s the next leg? Management sees India B2C and emerging market B2B as key levers.

- Coffee price risk: Can margins hold? Management leaned on its pricing model and just-in-time procurement strategy.

- Debt/Working Capital spike: Clarified that higher debt is order-backed, not speculative. Expect easing as coffee prices soften.

- Shorter contracts: Mgmt. acknowledged it’s a trend but assured client relationships are strong.

- Product & market bets: Analysts liked the innovation pipeline and the focus on underpenetrated regions.

CCL Capacity Expansion

1. Vietnam – Ngon Coffee (Subsidiary)

- Type: Spray-Dried & Freeze-Dried Instant Coffee

- Future Expansion: A large freeze-dried project still under construction (~₹199 Cr spent by FY24)

- Significance: Now the largest coffee unit in Vietnam

2. India – CCL Food & Beverages (New Subsidiary)

- Type: Spray-Dried Instant Coffee

- Capacity: 7,000 MT per year

- Location: Tirupati, Andhra Pradesh

3. Capacity Overview

- FY23 Group Capacity: ~55,000 MT

- FY25 : ~77,000 MT

- Current Utilization: New plants at ~10–15%, old ones near full

- Future Capex: No major expansion planned FY25–FY27 (only maintenance)

| Plant | Location | Type | Utilization Status |

|---|---|---|---|

| Ngon Coffee – New Capacity | Vietnam | Spray-Dried + Freeze-Dried | 10–15% utilization (new capacity ramping up) |

| CCL Food & Beverages Pvt Ltd | Tirupati, Andhra Pradesh | Spray-Dried | 10–15% utilization (early stage) |

| Older/legacy plants Running at or near full capacity |

34 Likes