Yes I agree. The AGM is pretty disastrous and very disappointing. The worst part is NO ANSWERS were actually ANSWERS.

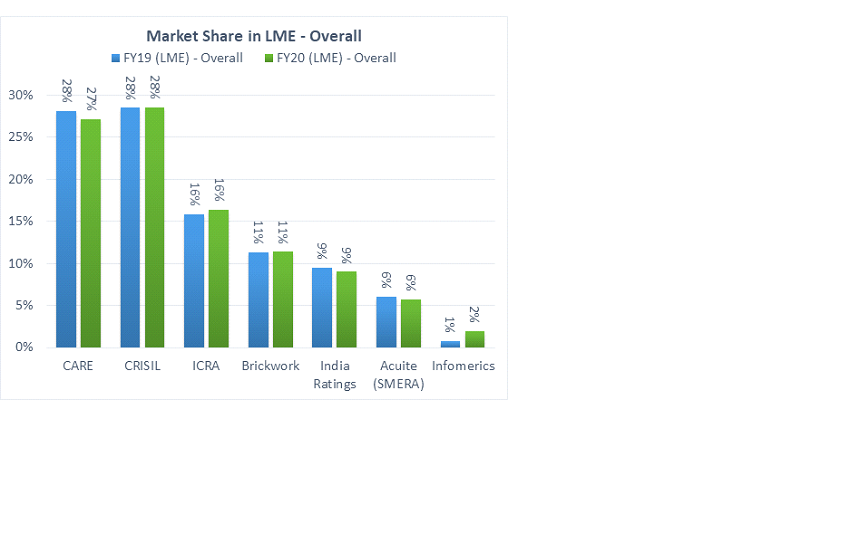

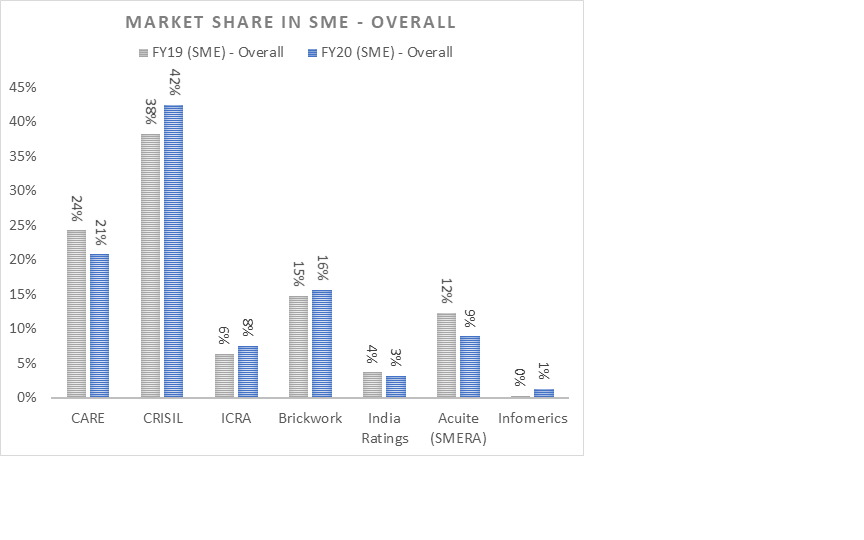

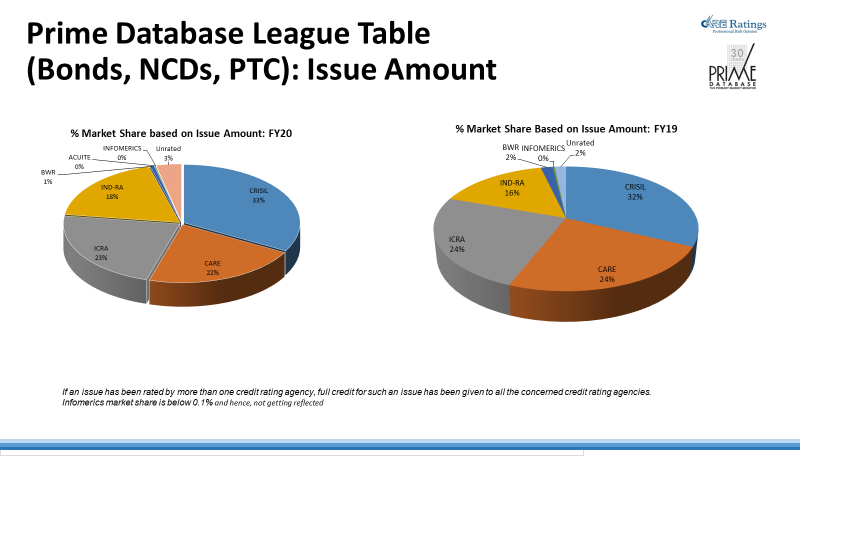

However their argument on market share have some ground.

Yes I agree. The AGM is pretty disastrous and very disappointing. The worst part is NO ANSWERS were actually ANSWERS.

However their argument on market share have some ground.

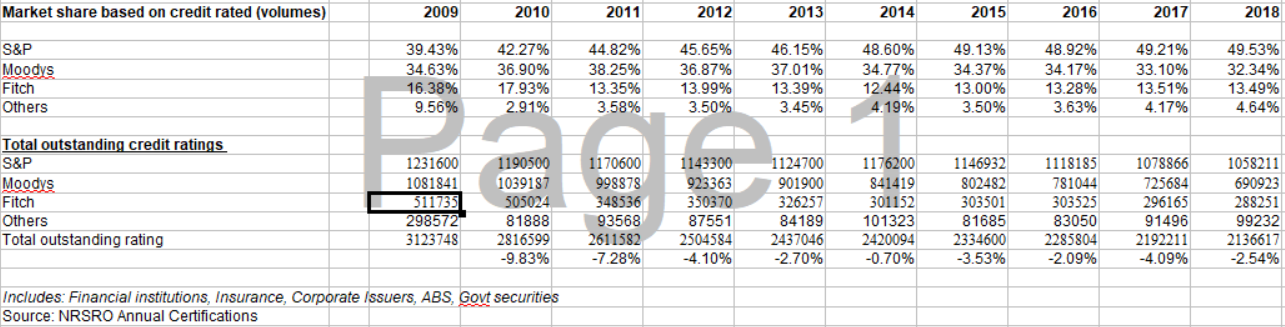

Did some digging around the US CRA market shares, by volume. Not a significant decline / change seen. That being said, you can see how much of a stronghold S&P has here ![]() (and so will CRISIL, esp. in down-cycles)

(and so will CRISIL, esp. in down-cycles)

The interesting trend to see is that the # of rated paper has gone down across most years

You can have a look at the actual reports from here: SEC.gov | Reports and Studies

CARE RATINGS update: Was looking at the NIFTY500 list. CARE is on the verge of getting dropped from the list. Is it market over-reaction?

Can you share elara capital research report please

Nirmal Bang inteview (link)

CARE results out - largely in line with last year results. Rs 8 dividend declared as Interim dividend.

Here are my notes from the concall

One thing that I want to know is how much of the current rating business is from the BLR line to PSU banks and what is the impact of a shift to Internal Risk based ratings from banks?

Disclosure: Invested (Position size here)

Wow finally mindset change ![]()

Mindset change happened for CRISIL, Happened for ICRA , Happened for FITCH and so this is also in a similar industry. Right !!!

During the webinar, the CEO was asked about buyback as opposed to dividends. The questioner suggested buybacks instead of dividends. The CEO said he had to discuss regarding this.

The issue price of CARE was above 700. Dividends are taxed as per the tax slab of the recipient. Since the current market price is below the issue price, buyback tax of 22.4% wouldn’t apply and thus buyback would be the better choice for the existing shareholders if done via the open offer route.

You are still not getting the point. First of all Let me tell you that ratings research is not a rocket science just like sell side equity research. It is a 27 years old company with undiluted focus on rating biz in India and they still lag their peers. This is despite the fact that they have got their turf protected by regulations. On top of that they got into everything to dilute their brand with weak organizational control. I am saying that again not because of recent negative headlines.

Let’s invert the argument - they know that their peers are global ones and they would still survive despite events like GFC. Would Care Ratings be able to withstand reputational damage like they got occasionally especially since Care’s area of operations remain limited? Trust and integrity is the only differentiator in this biz and they just squandered it. Good for them that regulators are not adding more rating agencies. They would bounce back eventually as economy revives and everyone focuses back on growth of balance sheet rather than recovery. These rating agencies can again relax till the next crisis.

Disc.- I am not interested in this stock at any price so can’t do any comparisons.

I guess it matters what a company does when it finds out that their reputation is hit. How do they react? Are the changes they make meaningful? Can they recover if they take the right steps? A statement regarding reputation over business is the same Buffet made in the Salomon Brothers scandal.

Something similar is happening in Wells Fargo Bank now. Compared to CARE Ratings, they have done much worse (as it seems to me). So, maybe CARE can recover from this and even do better than before. Anyway we get to study a company with a damaged reputation over the next few quarters/years as it tries to right the ship.

Also, CRISIL owns 9% of CARE. Here is a story from 2017 regarding the same.

First L&T MF and then Aditya Birla Mutual fund collectively sold 1+ million shares approx in a week and thats the possible reason for a sudden and huge drop in price just before the qtrly results.

As Basant Maheshwari has so aptly said “Everyone knows the RISK , a prudent investor knows HOW MUCH is already factored in the price”

CFO and Chief Ratings Officer resigned. Is that a good or bad for CARE in the long term?

I really disagree with the view. Even after GFC, Moddy’s took 7 years to get to the pre 2008 levels of earnings. Reputation is everything here. Although I am invested here and have seen moderate returns (30% in 3-4 months) but after SEBI rebuked them for Oaktree, I am skeptical.

Although I really admire the new boss and they have started cleaning their house. Internally they have let go off many people who are being there for a long term. He is bringing about cultural change.

But I totally agree that we have to wait and watch. it is too premature to give opinions.

Thanks for highlighting the recent changes as I do not track it closely. Some recent personal changes are much required and timely. I had been highlighting its mediocre talent in the past with lots of folks marking my messages offensive. It can result in turnaround if they could manage to hire good folks and improve work culture. Mr. market is defnitely sensing the same but I would rather bet on the frontrunner Crisil if at all have any bet in the sector.

Disc.: No interest

Guy Spier on CARE. It is a long talk, but he has lot of positive points for CARE.

Dear Paragbharambe,

Thanks for sharing. Very insightful…!!

now that the Company Secretary is also checking out …hope the new leadership that Ajay will bring on board will deliver the much-expected results …

Rs:3 interim dividend declared and 19th-Feb is the Record date for the interim dividend.

Compared to last quarter this quarter isn’t good. Q2 EPS 12.04 vs Q3 EPS 6.32

Results can be checked here