How do we know if the series of resignations is a good sign rather than bad? Let’s hope they can hire a suitable replacement fast enough.

We will have to see how CRISIL performed in Q3 to evaluate the Q3 results of CARE? Looks like credit offtake is still low.

Wanted to highlight one point: I wouldnt compare QoQ.

If you check on screener, there seems to be some seasonality in CARE’s quarterly earnings, where June (Q1) and Dec (Q3) ending quarters , the earnings are lower than Q2 and Q4. Have to confess, i dont really know the reasons for this seasonality/cyclicality.

2 Likes

You are right Saurabh, as many of the listed debt instruments has a half yearly requirement of ratings disclosures on nse. So that could be the reason…

1 Like

Appointed new CIO and website revamped … Things are slowly

1 Like

He joined Care a few months back, if you observe the CTO is a serial job hopper from India infoline to Poonawala fin to Care …it appears he doesn’t stay somewhere for long …not prejudiced but just an observation

2 Likes

CRISIL’s revenue from rating service in FY21 Q3 (150.66 Cr) is more than 3 times of Care 's (48.34 Cr) !

Different accounting policies and revenue recognition between the 3 agencies

Assuming valuations based on a multiple of revenue, it seems that care is extremely undervalued. This statement also assumes that CRISIL is appropriately valued. Crisil’s market cap is 10x that of Care and I expect this difference to close down significantly. Care should be at least 3x from this valuation. It’s obviously impossible to predict when will that valuation gap close. Time will tell.

@a_investor : - Interesting valuation perspective put across here.

However, below are few factors to consider which make CRISIL sell at a valuation they sell for : -

- A more diversified revenue stream

- Promoter brand - S&P

- Mgmt reputation - Didn’t had thr name involved in debt rating crisis

- Scale of operations - Thr revenues vs. revenue of next 3 players

So, while looking from pure valuation comparison perspective - CARE may seem undervalued, but it might also be the case that whn taken above factors into account CRISIL might deserve to be appropriately/ a bit overvalued and CARE deserves to remain undervalued.

I’m assuming if u’re already invested, u might have made an assessment of above factors in ur decision. And u can add ICRA to ur comparison list, check for above factors thr and analyze to see which one is better bet or none of thm are.

Disclosure : - Not invested.

@shardhr, I agree entirely that CRISIL is a much better operator with a far better pedigree, brand when compared to CARE. My bet on CARE out of all the Indian rating agencies is motivated by their cheap valuation. It may be so that they continue to be cheaply valued and never recover or close the valuation gap.

Based on both empirical and theoretical evidence there is space of 3 competitors to exist. CARE being the top 3 rating companies should therefore survive and hopefully thrive.

One major qualitative factor in my mental model is a “home turf/pedigree” advantage. I’m not completely trusting of the slogan ‘atmanirbhar’ or ‘make in India’ but definitely think that these marketing slogans can give home-brewed companies a tailwind. Valuation is the only thing that makes me sit comfortably to hopefully watch this thesis playout.

Looking forward to learn more from other informed investors and analysts.

3 Likes

Honestly, I believe the most important aspect CARE need to work on is the actual quality of work and reporting itself. They should invest into its talent pool, pay them as per the industry norms, ensure that the most valued employees are retained, provide the analysts and managers best in class training and invest into analytic tools and applications.

End of the day a consulting firms future will be directly related to the quality of work they deliver - pricing power and valuation will follow once they start delivering. Crisil gets the valuation it deserve since they deliver best in class service.

AJ

Disclosure: Have a tracking position in CARE.

3 Likes

There is a seasonality to the earnings of Care Ratings. So, two quarters are lacklustre and the other two aren’t. This has always been true, for the most part. Crisil is not strictly comparable since they have a data dissemination business that is around 40 percent of their top line. In the case of Care, the current decline started immediately after the quarterly results and has been exacerbated by the fact that they got kicked out of the Nifty 500 benchmark.

The management seems to be very careless about investor communications. Sometimes, they have a post results earnings call and sometimes they don’t have one. That sends the wrong signal and indicates poor corporate governance. They should either not have an earnings call at all, or they should have one irrespective of the quarterly results. The current policy of a random call does more harm than not having any calls. It doesn’t show transparency on the part of the management. They should ‘care’ about their investors (no pun intended). I expected a change after the new guys took over. Still waiting for that to happen.

The next quarter should be better than expectations.

(Disclosure: Long)

3 Likes

Hi Ysk,

I think new management is changing the things. If you follow the last updates , Senior Management have been replaced with more creditable names, latest being Sachin Gupta from CRISIL. So, it is a step in right direction. Lets see what happen.

And Yes, I agree with you on earning call. When you are turning out the company at least quarter earning calls is a good point of contact.

4 Likes

Excellent set of numbers from CARE. Momentum seems to be back and hopefully with economic revival, this business is poised for good times ahead. The new CEO is seriously revamping the business and have hired some quality people at the top - been hearing about some internal operational restructuring as well.

Valuations are supported by cash and investment balance of 500 Crore and reasonable dividend yield of about 3%.

See the results and the investor presentation.

AJ

Disclosure: Invested and biased.

7 Likes

CARE Q4 FY21 Earnings call - CARE Ratings Earnings Call for Q4FY21 - YouTube

Worth a listen for broader context as well.

Here are my notes from their Q4FY21 concall and subsequent interviews

• Market share had dropped to lower 20s from high 20s in the last few years, reiterates focus on ratings quality and independence given to the ratings team

• Growth in credit doesn’t always translate into additional rating business because a lot of credit is issued by large banks/NBFCs which are already large clients. Also PSUs pay very little for ratings whereas private sector pays more. It leads to rating business growth when credit growth is broad based across companies from different sectors and from smaller and mid-sized corporates

• Sustainable operating margins going forward should be 35-45%

• Added senior level employees, appointed a new CEO for one division and came up with a new rewarding scheme for outstanding employees

• Wish to reach scale in non-ratings business (risk solution + advisory) accounting for 1/3rd of overall revenues over the next 3-years. Will use cash in the books to catapult this growth

• EBITDA margins over the next 4-5 years: Risk solution (30-40%), Advisory (depends on brand adoption)

Disclosure: Invested

6 Likes

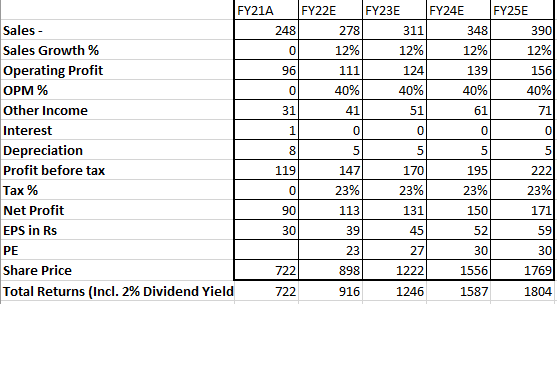

I have tried to compute how CARE’s growth will reflect in the stock price. In this computation, U have assumed the following

- Rating business grows at 12% CAGR over FY22-FY25. Basis of this assumption is that overall bank credit growth will grow at low-mid teens over this period. CARE’s rating business will grow at the roughly the same rate.

- EBITDA margin at 40% (basis: middle of the band that management has guided for).

- PE improves gradually from 23 in FY22E to 30 FY25E in this period (basis: CARE used to trade at 30 PE+ during FY17-FY18 when business growth was roughly in this range).

- Not included optionality from consulting/advisory business that CARE is looking to incubate.

Calculation is attached.

|Year|Price|

|FY22E|898|

|FY23E|1221|

|FY24E|1556|

|FY25E|1769|

Please let me know views on this.

4 Likes

I believe the rating revenue projection of 12% CAGR over FY22-25 is a little aggressive.

The rating revenue for CARE is driven by the growth of wholesale credit, led by non-government, non-finance firms in the economy.

That would in turn depend upon capex by the private sector. Even today, most of the credit growth is in the public sector enterprises or driven by financial firms.

In my view, credit to private sector non-financial firms would not grow in the mid-teens (I hope to be wrong).

Furthermore, even in the boom period of 2014-2017 with GDP growth upwards of 8%, the rating revenue for the players in the industry grew at 6-9% CAGR. Although the past is not an indicator of the future, it does give it some colour.

The upside to all this is that we are starting on a very low base, and who knows if the recovery is strong and the animal spirit gets rekindled, Credit growth could even smash past 12% CAGR.

Rest all the assumptions are quite probable. Thank you for sharing that.

3 Likes