Press release has no mention on this other financial asset.

Anyone from Accounting background who could help here?

Press release has no mention on this other financial asset.

Anyone from Accounting background who could help here?

The decrease in cash flow on account of financial asset is approximately representing increase in investments into fixed deposit maturing with in a period of 12 months. Please have a look at how “Bank balances other than Cash and Cash equivalents”(which generally represent investments in fixed deposits with banks) are moving.

Thanks,

AJ

Thanks for the reply. I was under the impression that such bank deposits placed should be under the head of “Cash outflow from Investing activity”.

Shouldn’t that be the case, or is it at the discretion of the firm preparing the cash flow statements.

These are short term fixed deposits placed with banks which are considered as a part of working capital. One will categorize these as investing activities, if underlying is in the nature of fixed deposits with maturity exceeding 12 months or are invested in schemes with mutual funds etc.

AJ

Here are the two management interactions with the media post their results (video1, video2). The new MD has started making the right noises, here are my notes:

Unfortunately, I missed the morning conference call. I will update my notes once the transcripts are made available.

Its time to see how efficient the management is in diversifying their revenue base and building new business lines. I see a lot of webinars organized by CARE training, their research and analytics business should provide growth, execution is the key!

Disclosure: Invested (latest position size here)

I went through the RBI paper and here are my notes:

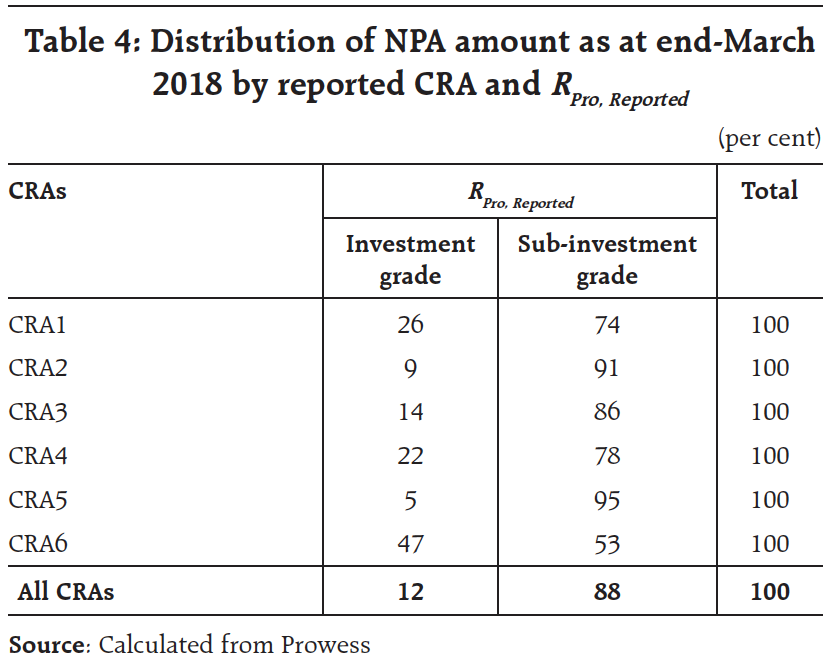

In the picture below, who is CRA6?

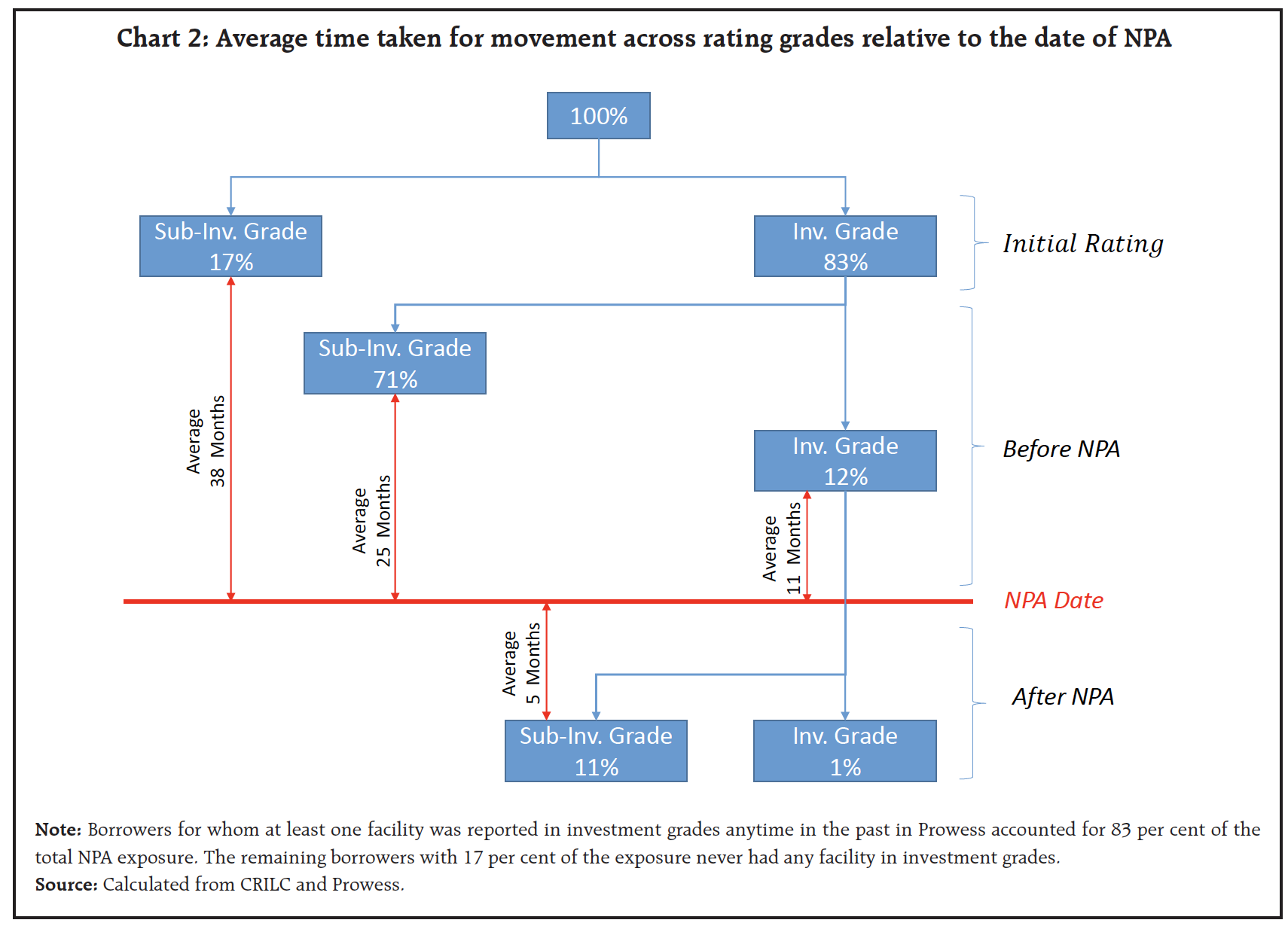

This is the average timeline for movement across different rating grades to NPA.

@nirav565 Have I missed something?

https://m.rbi.org.in/Scripts/BS_ViewBulletin.aspx?Id=18704

Multiple implications for the Banking & Finance industry

Who is CRA 6 is a great question!! Is there any more information on this?

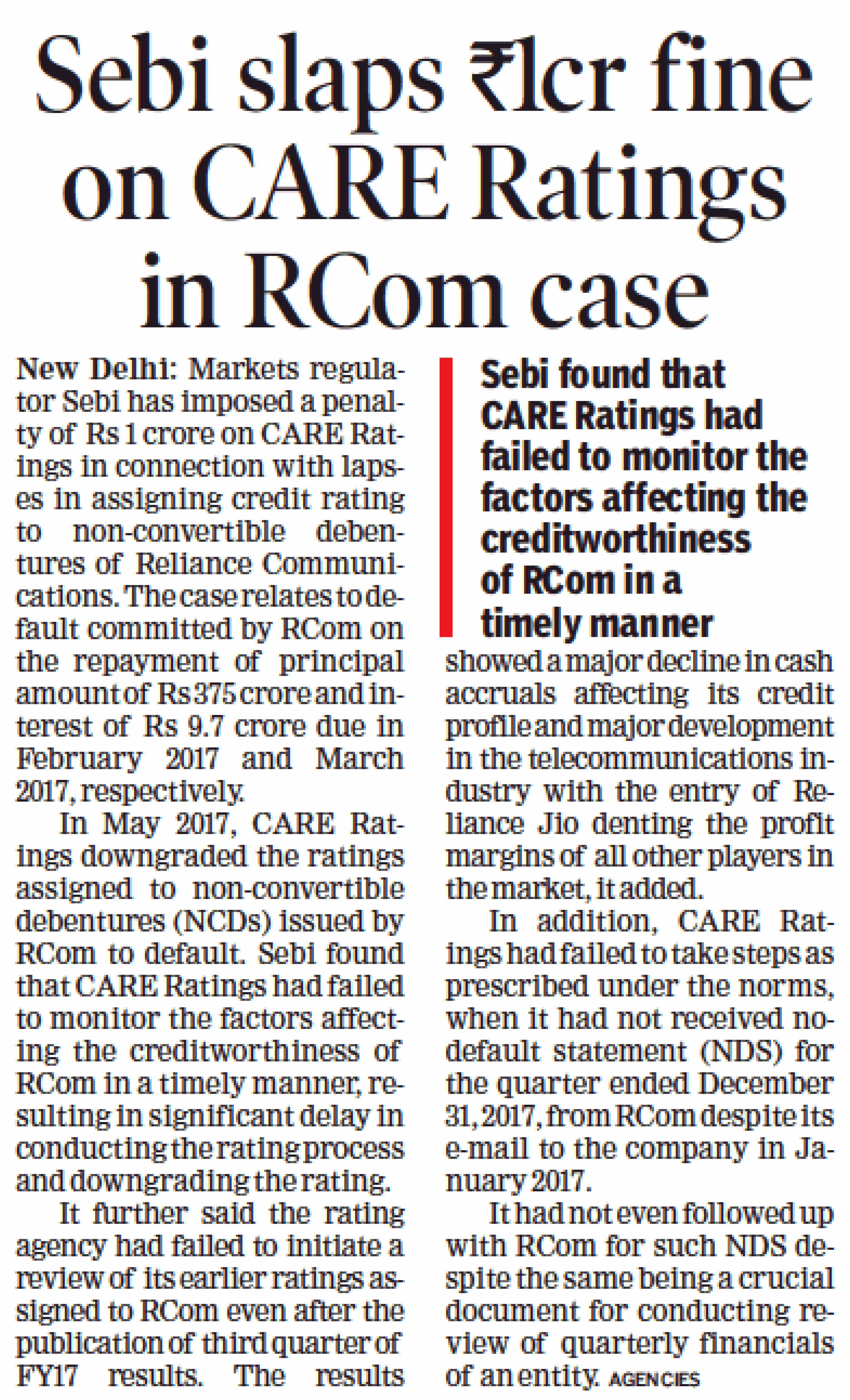

SEBI has imposed a penalty of INR 100 lakh on the company, under section lSHB of SEBI Act, 1992. CARE is reviewing the adjudication order and considering the appropriate course of action. I think, this is max penalty (100 L). I believe CARE may not take any action. Though settlement of this case is notional in mind. But getting over of this is must for future.

Once this SEBI action is out of the way, market will start looking at the company with a new perspective. Afterall its second largest rating company and had been consistently posting 100-150 cr. kind of NP for many years. It has a cash and investment of around 450-500 crores and is trading at 1300 cr of marketcap. Thus core business of around 125 cr. of normalised operating net profit is available for a p/e ratio of 6-7. Compare this with 20-35 kind of valuation being given to ICRA and CRISIL. The tainted executives have already been relieved from the company. It is a matter of time before market perspective changes about the stock. Though economic cycle also has to pick up if company has to come back to its normal level. If my memory serve me right sometimes during last year SEBI had introduced a uniform grading system for all rating agencies that should help reduce the quality perception gap in the ratings given by the companies.

(Disclosure - Invested. Have added more quantity during last week)

So it seems this penalty was for Rcom case. That means the adjudication proceedings are still ongoing for other cases i.e. ILFS, DHFL etc. and SEBI can impose a penalty upto 1 cr. in each case. Overhang will remain till it comes out clean.

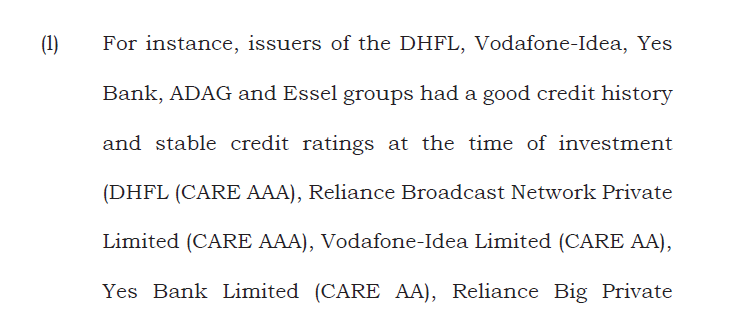

Looks like CARE ratings was penalized by SEBI recently. CARE seems to have been the rating agency for ADAG, Yes Bank, Vodafone cases etc.

This is definitely going to cause the reputation of CARE to be damaged and will make their ratings less valuable in the market. This overhang probably explains the low P/E. Low P/E contains the junk of the market

Most of these companies would have been rated by multiple rating agencies besides CARE, so it does not seem to be a CARE specific issue. However CARE PE and performance seems to have declined more than peers.

The question to ask is that if CARE substantially improves its rating standards and makes them stricter, how much lasting impact does this create on its revenue. Also has anyone tracked loss of key personnel and thereby loss of relationships for the rating agency

In terms of rating pecking order, if one leaves out CRISIL, the rest of the pack are generally trying to target the same market and it is this competitiveness among the 4 - CARE, ICRA, Brickworks, Acuite and to an extent India Ratings which impact the rating quality and pricing. Have the recent events made capital market participants change how they value CAREs rating benchmarked to CRISIL? If this is the case the long term devaluation of the PE multiple is justified else there is an investment case.

Any views on this appreciated.

Disclosure: No holding

Most investors comparing the 3 agencies miss out on the part that CRISIL and ICRA aready have a fairly established Research and Analytics Business ( This is my understanding frm studying 3 cos., contesting thoughts are welcome on this). However, CARE ratings is more of a pure ratings-play. Hence, more volatile revenue fluctuation and which in turn, gives it the lower PE it deserves.

In research and analytics business, they are starting out but I blv the Foreing parentage of other 2 cos. vl give them an edge here.

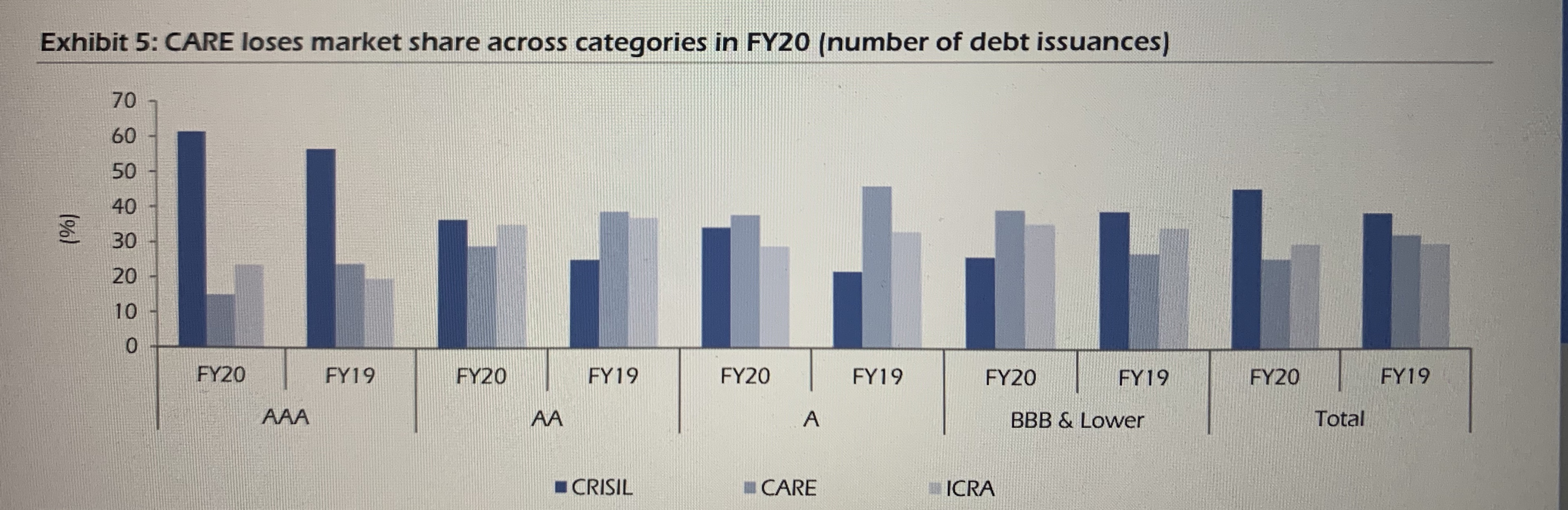

Amit , I’ve read your previous posts here and found them to be very insightful. In case you haven’t seen the marketshare loss, see below

You can see how much better place Crisil is, among the agencies and look at where CARE is positioned

Seems like CARE is no longer the #2 player from the last column and ICRA has taken its position

Can you also share the source too?

My bad , it’s Elara Capital’s 1Q broker note that came out a month ago. I’m looking at this name for obvious reasons but the headwinds they face are quite steep. Let’s see in coming quarters. If you have updates on the marketshare and any colour, please do share

Great data, yes its getting reflected in the quarterly numbers also.

Interesting thing though all the time bomb “BBB and below” CARE market-share has increased.

Got chance to view CARE Online AGM proceedings (FY19-20). Unfortunately could not get a single transparent answer of shareholder’s queries from the board. Most of it was beating around the bush.

Apart from it, it looks the board is in psychological denial of accepting that ICRA has beaten them from number 2 position, which is clearly visible from last 2 years data and particularly from Q1 2021 numbers.

Apologies for being negative about these developments, but could find anything positive from AGM, not even the acknowledgement of lagging behind.

Disclosure- Invested