Thats good to hear. Are they seeing any slowdown in new loan requests in

their branch?

Take a loan man! If you take a loan of 30 lacs I would gain Rs. 300. I will buy you a coffee if we meet

Thanks for sharing the findings of your check!

2 Likes

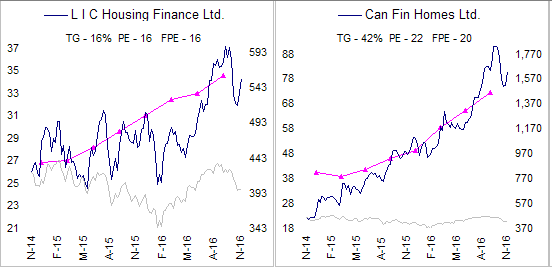

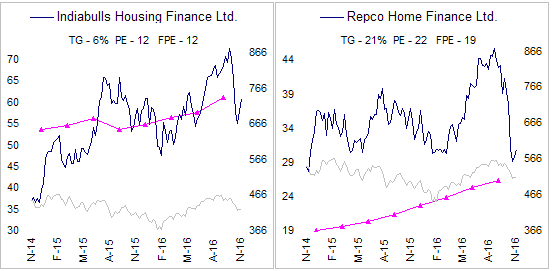

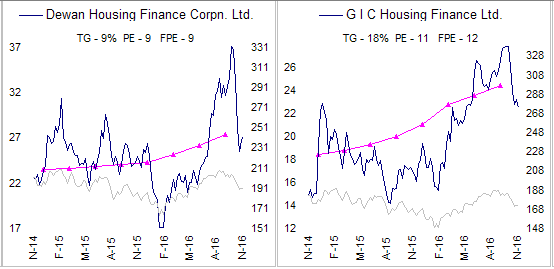

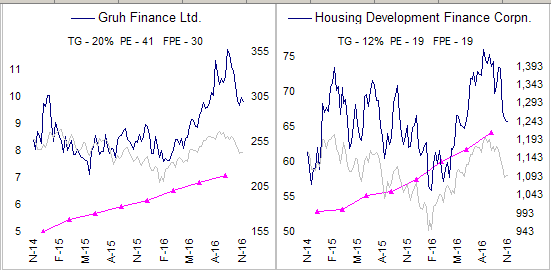

Further to my earlier post on fundamental attributes of HFC, here are a few charts about valuations. These are price charts for last 2 years along with movement in TTM EPS and Nifty as these are two most important factors that drive stock price.

Stock price & Nifty 50 is on right hand scale and EPS is on Left hand scale.

Legend -

Blue line is stock price

Pink line with triangle markers is TTM EPS line.

Grey line is Nifty indexed to stock price.

TG = Trend Growth in EPS. This is the slope of a log linear regression line of the TTM EPS numbers. This number shows short term (2 years) trend growth rate in EPS.

PE = Current (Dec 2, 2016) Price / TTM EPS.

FPE = Fair PE calculated using DCF valuation for each company.

In general, if the price line is below the EPS line the stock is undervalued. For each company, a DCF valuation is done to determine the intrinsic value and this value is divided by adjusted EPS to arrive at a Fair PE ratio. Generally, but not necessarily, fair PE is close to trend growth rate for average quality companies. for better quality companies, market is willing to pay up so fair PE is higher than trend growth and for lower quality companies, fair PE is generally lower than trend growth mainly due to higher discount rate used in valuation. When fair PE is revised upwards (downwards), EPS line will move higher (lower). In the long run, shareholder returns will be close to trend growth in EPS if you manage to buy at the fair price and sell it at a fair price.

My Analysis -

LIC - Trend growth rate is medium 16%, somewhat undervalued.

CanFin - High growth rate (42%), fairly valued.

Indiabulls - Trend growth is low at 6% mainly because of a QIP issue in 2015. growth should pick up in 2017. Fairly valued.

Repco - Trend Growth is high 21%, stock is overvalued despite recent fall due to high PE and lower fundamental ratios

Dewan - Trend growth is low 9% somewhat cyclical. Stock is volatile. Fairly valued.

GIC - Trend growth is medium 18%. Picking up. If this rate sustains, stock will be re-rated. Undervalued.

Gruh - Trend growth is medium-high 20%. Stock is overvalued as PE is much higher than fair value. This stock continues to trade above fair value due to strong fundamentals and growth opportunities.

HDFC - Trend growth is lowest 12% reflecting it’s big size. EPS growth is stable however stock is not. Fairly valued.

Overall, HFCs have a consistent growth in EPS over the last 2 years (compared to other companies) but stock price has shown volatility possibly due to problems elsewhere in financial sector.

19 Likes

Two questions in my mind.

Would the Prime Minister’s interest rate waiver announcement be valid for home loans taken from HFCs also or would it be only from the banks.

Also how would government compensate banks or HFCs for the waiver.

Answers to these two questions would be important to influence the growth trajectory of HFCs in general and Canfin more specifically.

Disclosure: invested at lower levels

1 Like

- Interest subsidy would be given to all FIs (including NBFCs) registered with NHB

- Interest subsidy would be paid by NHB to HFCs in one shot and that would be adjusted again Principal outstanding.

Disc: I work in NBFC HFC

10 Likes

Thanks umang for clarifying.

That would be a good trigger for loan growth for HFCs in smaller ticket sizes. Also since effective interest will be equivalent to savings account interest for the customers along with small EMI size, I tend to believe that NPAs would be negligible in this category.

Interestingly, Can Fin is up 5% today again great way to start 2017 also.

Going through the entire thread…it’s interesting to see how this long term story has been unwinding and to me personally it looks like the run way is pretty large and to be kept unwinding for years to go!

1 Like

Great work, Yogesh. Thanks for sharing your detailed analysis. BTW, I’ve also read your similar analysis on Banks, but yet to read on MFI’s. Kudos

1 Like

Dear boarders - Can anyone throw some light on the impact Canfin might have due to sudden drop of lending rates by banks? I know Canfin’s funding from banks is less. But the NCD / CP funds - can they be re-priced quickly, so they can reduce their home loan rates to customers? I generally see the commercial paper duration to be shorter.

An eg., below.

Jan 3 (Reuters)- Below are the details of India commercial papers dealt in the

primary market. (10 million = 1 crore)

ISSUER INVESTOR MATURITY RATING DEALT VOLUME VALUE

YTM(%) IN MLNS DATE

PRIMARY MARKET

CANFIN HOMES MF 06-Mar-17 ICRA A1+ 6.5500 1000 04-Jan-17

CANFIN HOMES BANKS 06-Mar-17 ICRA A1+ 6.5500 5000 04-Jan-17

MFI comparison is here,

5 Likes

Hi @Yogesh_s,

Thanks a lot for this informative comparison. I particularly liked your style of presenting data through charts, makes it so easy to comprehend.

Is this in excel or are you using some other charting tool?

1 Like

This is Excel and version is so old that I don’t event want to mention it. ![]()

If a picture is worth thousand words then a chart is worth a thousand numbers. Makes number crunching easy.

1 Like

I never mind it. Old is Gold and many a times only Old is Gold. ![]()

Absolutely agree. It’s quite handy in striking it big when market gives you opportunity if one is “few bets, infrequent bets, big bets” kind of super concentrated investor aka CM and I find tremendous virtue in this. Just do the comparative industry analysis that lies in one’s CoC with long term predictable economics, i.e. Finance and many of its offshoots, keep the analysis ready preferably in pictorial forms and wait patiently for the right opportunity and strike it big when one gets it and market seems to offer such opportunity once in while every 1-2 years.

1 Like

Thanks for the link, Yogesh. This one is similarly impressive…

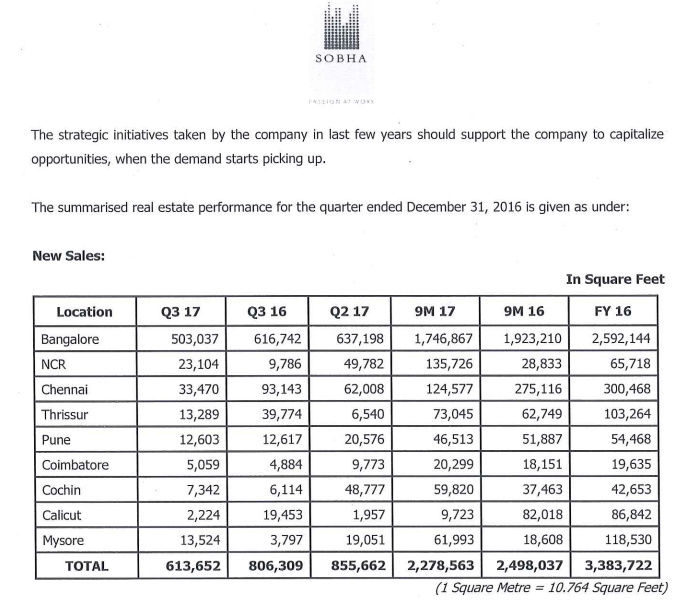

Sobha developers (one of the leading, slightly high end real estate developer in Bangalore and Kerala) has reported de-growth in new home sales for Q3 2017. Details below. In Bangalore alone there is 25% de-growth vs Q2. I am not sure about seasonal factor but it was festival time, so sales should only be higher. Also, customers of properties from this developer don’t really belong to the target customer segment of Canfin Homes. And one developer is not a benchmark for the whole real estate market of Bangalore. Still worth to see the impact of demonetization on real estate transactions.

I am quoting Bangalore here, as that city alone comprises 38% of the loan book of Can fin (as mentioned by the CEO in a TV show or some).

Also interesting to know that Godrej properties had recorded very good apartment sales in this period is Pune. That must definitely be in the high end segment. We will know more once Gruh announces results this Friday and Canfin next Tuesday.

1 Like

I think instead of just a QoQ numbers, info on active projects and new launches during the quartet might be more helpful to see why revenues were down. I thought Sobha wouldnt cater to people who bought using blackmoney (the black money paid in cach and goes unaccounted). I agree with the fact that there are some challenges for the real estate companies, especially the ones that are small and deal with unaccounted cash. I am keeping my fingers crossed to see how would have housing finance companies done this quarter.

In their report to the exchanges, the builder has mentioned that this is a

short term phenomenon due to demonetization. Also, the YoY numbers also

indicate a 20% de growth. That is why it is interesting.

Another interesting thing to note is: in the dec quarter, the promoter

stake of canfin homes has gone by 0.6% It is not Canara bank that has

increased the stake but their JV - Canara Robeco MF has bought that share

from market. The fall based on selling by catamaran has been bought into.

3 Likes

Textbook style execution.

NIM has risen every quarter since last 10 quarters.

3 Likes

CAN FIN HOMES - The PSU which has Quadrupled in wealth for investors in a short span of time is a wealth creator without doubt . I have been tracking Can fin homes for the past 6 months , nd its track record has been excellent . Its posted numbers in terms of Asset quality and Loan book growth has been impressive .

The execution of the Managment seems to be excellent , Major target customers are salaried people that’s nearly 88% and remaining Profesionals is directly linked to the Asset quality and lower delinquency rate . Loan portfolio too is majorly concentrated on Housing loans and a lower proportion on Non housing loans .

NIM around 3.2 % is excellent with 1.65 ROAA and a ROE of 18% the banks p/BV is around 5 which made me skeptical about the valuation . With a 18% ROE I would be willing to pay near 3.5 times Book whereas the stock quoting at 5 times Book is a little over valued . The NPA are lowest under 0.18 whereas the industry average is 0.70 and a full provisioning looks strong in terms of mitigating risks .

I have written a research report on Can Fin homes , the link is provided above .

Disclaimer : I’m not a registered analyst . Not holding . Following closely , views may be biased . The report has been presented to clients and some of whom may have bought with/without my knowledge .

2 Likes

well you can’t blame valuations now, there were enough options to accumulate it during past 2 months, esp after the management clarification post catamaran plunge… The world lacks growth and where ever investors see consistent growth it would be bought into… you may look at PNB housing as valuations are still reasonable there or maybe Repco post the recent fall

3 Likes