Very impressive set of numbers. Disbursals slowed quarter on quarter, may be one off, but grew YoY.

The margins continue to improve. Very pleased. With interest rebate for low income houses announced from Gov, they are trying to capitalize it with opening centers to approach this particular segment. Would be interesting how it pans out.

1 Like

5 Likes

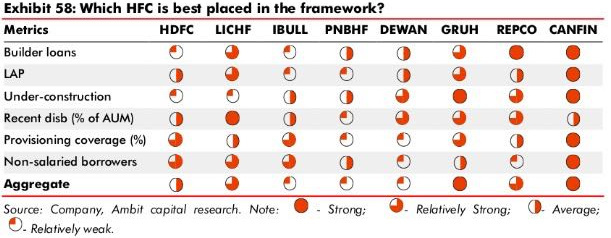

Exactly should have bought a piece of the business when it was not in the fancy of investors . PNB too I have studied its impressive too . On a Peer comparison basis than Odds are higher for PNB at current levels … At the same P/e of 28 it’s a cheaper with Lower p/b, Post IPO its at 2.6 somewhere so that’s looking cheaper .

ROAA is what I’m looking for as PNB is a little diversified and in its loanbook than Can fin and geographically diversified to 3 regions whereas Can fin is more of business in South India . Managment both being PSU have to wait and see how their Asset quality is going forward .

1 Like

Canfin Homes Concall update:

- Dont see much impact of demonetisation—there was some slack in Nov–but growth is back to pre-demonetisation levels

- Avg business/branch is ~100crs

- Canfin is known for its asset quality

- Maintain our priority for salaried class—which accounts for 77% of the total loan book

- Avg loan to Value is 70% in housing segment, LTV in LAP book is below 50%

- Interest subvention announced by government is positive and augurs well for growth

- Prepayment rate in housing is 16-17% including advance payments

- Canfin follows risk based category pricing—

- Avg yield in housing segment is 10.7%, and in non housing ~14%

- Disbursements improved inspite no rates slashed by company in Dec–rates are reduced by 75bps effective today

- Rural hosuing is 12% of loan book—this is a fixed pricing book

- Lot of opportunity present in affordable housing—10 sattelite centres to be converted into full fledge affordable housing centres

- Expects to maintain and work on improving cost/income ratio

4 Likes

Any idea why they had cut the lending rate so steep if business is back to normalcy? They are offering 8.95% (cut of 0.75% from earlier starting ROI of 9.7%) which is very close to that of banks and leading salaried class targetting HFCs like HDFC.

not to forget it is the fastest growing too…

Banks have reduced their MCLR by ~75 basis points in January. The cost of borrowing in capital markets and NHB borrowings is also in the process of declining substantially. Overall, In January, their cost of funds has declined substantially and hence they are reducing interest rates for customers. They expect to maintain the interest spreads. I think that their RoA may cross 2% in Q4, but this would be pretty much the peak RoA for them unless their business model undergoes a major shift.

2 Likes

Pranav - I was actually wondering why they have priced their starting ROI close to that of the banks and big HFCs. They were always higher by 0.5% or more normally. Perhaps this is to curb customer attrition to other institutions.

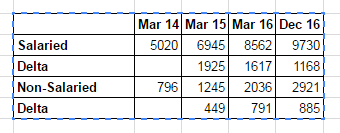

Also about the RoA, they are showing keen interest in non-salaried class now. In the con-call, Mr. Hota mentioned that they like that segment as they pay more interest. While it is a very basic point, I just felt they have more inclination towards that segment now. It is at 23% of the overall book compared to 14% in Mar 2014. Just from Mar 2016 till Dec 2016, the loan book has increased by 1200 Crores for the salaried class vs. 900 Crores for the non-salaried. Pretty close to even lending to both segments.

Additionally, they have announced creation /conversion of Affordable Home financing after government subvention scheme, so naturally this looks like a slight shift in business model towards more lending to non-salaried class.

If worked well, it can result in higher RoA.

6 Likes

I agree with your observations. Over the past 12 months (Jan 2016 to Dec 2016) the loans to salaried class have grown at 20-odd percent and 60-odd percent for non-salaried class. This shows that they are finding it easier to gain non-salaried customers. However, this may work out to be positive. The interest rate differential is about 2.5% between salaried and non-salaried class and historically non-salaried class has not shown a very high credit cost.

There still would be interest rate differential between CanFin and large PSU banks. Bank of Baroda reduced their minimum interest rate to 8.35% this month. Other banks are dropping interest rates.

3 Likes

Yes Pranav. Lets hope for the best.

Good point newone.

I would just add one more thing & that is - salaried class incremental loan book actually went down in March 16 & likely to remain to March 16 levels in March 17. This likely means that increased competition for a piece of pie of salaried class with nationalized banks.

As you mentioned, non-salaried class loan book can lead to higher margins but there might be more risk associated with it. I think we need to work on profiling borrowers in non-salaried category & analyze credit assessment practices of management in this segment.

Disc - Invested, not a buy/sell reco

2 Likes

@newone @rupeshtatiya Where do you get data on Salaried vs Non-salaried? I looked at their press release and other filings with BSE but didn’t find it anywhere. Did they disclose that in concall? Are you considering non-housing as non-salaried?

About the interest I found following in one of their filings

Their yields are dropping less than costs so margins have improved. Also that 8.95% is just a headline rate, not many borrowers are getting it.

1 Like

You can refer to the investor presentation in the company website.

http://www.canfinhomes.com/canfinhomes.php?page=investors

1 Like

Basic question - What are your views on sharp cuts in lending rates by banks?

From recent management interview - Company feels it is insulated by such rate cuts, as even earlier as well, company used to charge 40-50 bps higher than banks. Now the rates are even more competitive due to rate cut.

Will there be a customer behavioral change?

What is the reason customers are happy to pay higher to housing finance companies? Why they didn’t (and will not) move to banks for loan approvals at cheaper rates?

Do we know the revenue ,percentage of loan book and growth rate of the loan book by each state?

No that information of the loan book diversification according to geographical Areas is very dark have to look more into that part . Geo diverse gives a horizontal growth as well as vertical where the reach can be more. According to my understanding Each State or region can provide more growth in terms of availability. But as per Operating efficiency more diversification and expansion will lead to Cost to income to raise and Opcost as a % of income to raise.

Banks are having their own issues with NPAs. They aren’t gong to get into rate war with HFCs.

In the long run banks with access to low cost deposits are better placed to offer a rate sensitive product like a home loan but in the short term HFCs are good at serving customers than banks.

1 Like

If am not wrong, the seventh pay commission has been put into effect already. Did the management of Canfin mention anything about the impact of the same in their loan book growth in the latest quarter? Or did it get subdued due to demonetization?

Short Summary of Q3 conference call:

we have also prepared few other summaries. Sharing here: https://goo.gl/5RTk0o

Read disclaimer for summaries here: https://goo.gl/HELov8

4 Likes

1 Like