“Moat” is a much misunderstood word in the investor community but here is a classic case of what one looks like:

The main challenge for any new mutual fund is how to attract investors, most of whom would already be investors in other mutual funds. You can have your website and mobile app but then the investor must need you really badly so as to specifically download your app and invest. CAMS services most of India’s largest mutual funds. The myCAMS app has more than 5 million downloads and allows one to invest in any mutual fund serviced by CAMS. So essentially the MF has a “captive” potential customer base even if those people have not invested in your schemes at present. No wonder CAMS won all the three new MF mandates who set up a mutual fund in India last year.

A classic case of what a “moat” looks like.

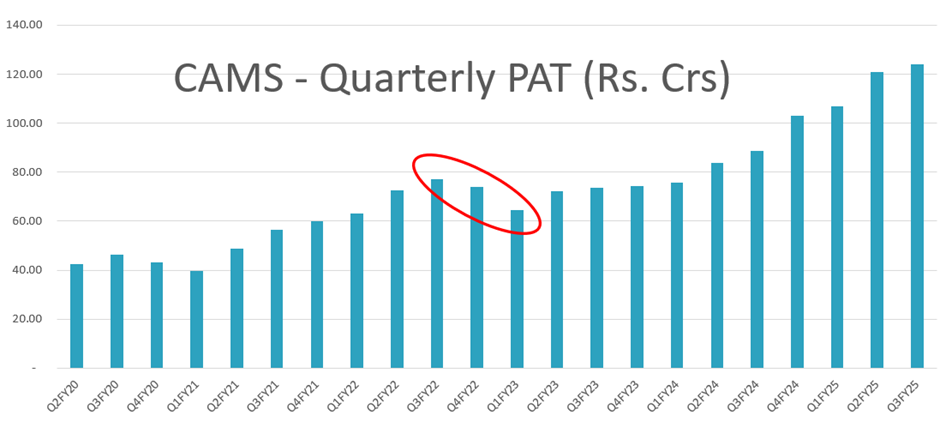

Meanwhile, CAMS had an almost goldilocks kind of a Q4, where everything came together and worked in their favour. Gross and PAT margins were among the highest in history, growth rates were strong across the board and cash flows (for the year) increased faster than the revenues. Overall company revenue grew about 25 %, MF revenues at 21 %, and non-MF at 38 %. (52 % including inorganic).

The non-MF businesses contribution to revenues has gone up to 13.5 % from 11, in line with the 2 % increase every year expected. AIF grew 24 %, CAMSPay grew 24 %. Management expects EBIDTA margins to be maintained at current levels going ahead as well.

During the year, CAMS won every single mutual fund mandate that decided to set up shop in the country.

GIFT City business is scaling up, with a larger office being set up and a larger team in place. Client size has gone up to 17.

Fintuple has become profitable at the EBIDTA level. Fintuple provides digital onboarding solution and integrates Custody, Clearing, Fund Accounting, Treasury & Forex services DIGITALLY under one roof

KRA grew a huge 30 % Q-o-Q and 90 % over the year with penetration in fintechs picking up dramatically. I had mentioned in one of my previous posts that the PayTM Payments Bank crisis will provide a good tailwind to CAMS KRA business. (See this)

Management says KRA, CAMS Pay and AIF will continue to propel the non MF business growth in immediate future.

Meanwhile, the mandatory demat of insurance is still awaited but IRDAI has taken one step forward mandating digital policy issuance. Mandatory policy demat will take time, I think.

Government has opened up Atal Pension Yojana servicing to more players, so CAMS will now participate in this as well.

Management says expense growth will remain in line with historical trends going ahead as well. Current headcount is 7800, annual increments are due in April and the company invests around Rs.7 crore per quarter in new platforms.

Non MF margins have crept up from 15 % in the past to 20 % now as the businesses scale up, but the steady state is close to 35 - 40 % in the long run so there is considerable scope for them to move upward.

(taken from Q4 FY24 concall transcript)

(Disc.: Invested)