I have read the Offer Document of CAMS and wonder if it is worthy of Investment as it focusses on Mutual Fund and Insurance Industries.

What I have put here is entirely from of Draft red Herring Prospectus as I am not capable enough of my own research. This is just an effort to get views from seniors to see if CAMS could be a long-term Investment candidate.

Computer Age Management Services ( CAMS) is a technology-driven financial infrastructure and services provider to mutual funds and other financial institutions with over two decades of experience.

It is India’s largest registrar and transfer agent of mutual funds with an aggregate market share of 69.4%. Over the last five years, they have grown their market share from 60.5% to 67.6% during March 2015 to March 2019.

Mutual fund clients include four of the five largest mutual funds as well as nine of the 15 largest mutual funds.

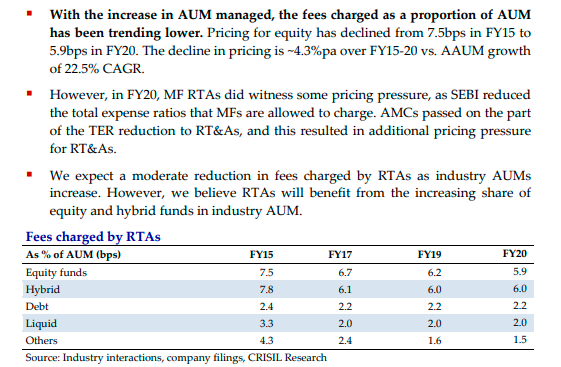

The growth in the AUM of mutual fund clients is important as substantial portion of revenues based on Average AUM. Also, they get more fees from equity mutual funds as compared to other categories of mutual funds. The AUM of equity mutual funds serviced by CAMS grew from Rs. 2,180 billion to Rs. 6,701 at a CAGR of 30% from March 2015 to September 2019.

Mutual Fund Industry Overview:

The AUM has risen at a CAGR of 17.4% from Rs. 1.1 trillion as on March 31, 2000 to Rs. 23.8 trillion as on March 31, 2019. Mutual fund AUM as a percentage of GDP rose from 4.3% in financial year 2002 to 12.5% in financial year 2019.

The AUM of equity-oriented funds grew at a CAGR of 39% from Rs. 2.1 trillion in financial year 2014 to Rs. 10.7 trillion for the financial year 2019, whereas the debt segment grew at a CAGR of 9% during the same period.

Individual investors (retail and high networth individuals) AUM outpaces institutional segment. Individual Investors Invest more in equity schemes (68%) vs institutional (14%).

SIP contributions have seen strong growth. Between April 2016 and March 2019, the monthly amount invested through SIPs has risen from approximately Rs. 31 billion to Rs. 80.5 billion or over 150% in absolute terms. Number of SIP Accounts grown 24% to 26.2 million in financial year 2019 from 21.1 million in financial year 2018.

According to CRISIL, the mutual fund industry’s AUM is projected to grow from Rs. 23.8 trillion as of March 31, 2019 to Rs. 54 trillion by financial year 2024, which represents a CAGR of 17% to 19% of which Equity AUM expected to grow 21-23% CAGR.

As on March 2019: HDFC Mutual fund is the largest AMC in terms of its AUMs (14%) followed by ICICI Pru (13.1%) - SBI (11.6%) - Aditya Birla Sun Life (10.1%) - Nippon India (9.6%) - UTI (6.5%) - Kotak Mahindra (6.1%) - Franklin Templeton (4.9%) - Axis(3.7%) and DSP Mutual Fund (3.2%). Top five AMCs have 58.4% Market Share.

There are 3 Mutual Fund Registrar and Transfer Agents Viz. CAMS | Kfin technologies | Franklin Templeton Asset Management.

Among the top five AMCs, HDFC Mutual Fund, ICICI Prudential Mutual Fund, SBI Mutual Fund and Aditya Birla Sun Life Mutual Fund are serviced by CAMS and Nippon India Mutual Fund is serviced by Kfin.

As of November 2019, CAMS serviced Rs. 18.7 trillion of average AUM which constituted approximately 69% of the total mutual fund industry AUM.

CAMS has the highest revenue in the industry and also witnessed the highest revenue growth in the past three years with a CAGR of 20.4% in between financial years 2016 and 2019. For the financial year 2019, CAMS revenue from operations has grown by 8.1% and its EBITDA margins and RoE are better than its competitors. CAMS is the most productive MF RTA with its AUM per branch being the highest in industry.

Apart from Mutual Fund Houses, CAMS provides services to Insurance Companies with its division CAMS Insurance Repository Services. Insurance repositories act as a single stop shop for policy servicing for e-insurance policies.

Currently, there are four Insurance Repositories. Out of 1247475 E-policies - Market share of:

NSDL Database Management 45%

CAMS Insurance Repository 39%

KARVY Insurance Repository 11%

Central Insurance Repository 6%

(As on September 2019)

Other than above CAMS has:

Electronic payment collections services business.

KYC registration agency business

Software solutions business where it develops software for in-house mutual funds services business and for other mutual fund companies.

I did not read much into other business as Almost 87% of the revenue comes from mutual funds services business.

PROMOTERS:

Great Terrain is the Promoter of CAMS based out of Mauritius.

Great Terrain held 100% by Harmony River Investment Ltd, Mauritius.

Harmony River Investment Ltd is directly owned by certain private equity funds managed by Warburg Pincus LLC, New York.

This promoter of promoter of promoter type holding - could it be a problem in future (Thinking of GMM Pfaudler!)

I am surprised to know that CAMS Identifies - HDFC, HDFC Bank, Acsys, NSE, NSE DAL, NSECL and NSEIL as the group companies

Financials:

Not much data available as it’s a new listing:

As on March 31, 2019 they generated a revenue of 694 Cr - Operating profit of 201 Cr @ 29% margin and PAT of 131 Cr.

Interesting that CAMS gives out Dividend payout @ 65% which they intend to continue.

Risk Factors:

Almost 87% of revenue generated from mutual funds services business. Decline AUM of Funds could adversely impact revenue and profits.

Client concentration risk as TOP 5 client contribute 65% of revenue.

Regulatory Action Risk.

With my limited knowledge, I may not be able to answer any queries other than just hitting LIKE button

Disclosure - I have taken a tracking position - looking forward to inputs from ValuePick’rs to add more.

Thanks.