No. From 2015.55 to 5276.20 = 162 % increase = 2.6 X (to be precise).

If RBI cuts rates, market decline will accelerate. I hope they don’t cut. (I know this sounds contrary to mainstream narrative, but that is what empirical data shows). Let’s see.

No. From 2015.55 to 5276.20 = 162 % increase = 2.6 X (to be precise).

If RBI cuts rates, market decline will accelerate. I hope they don’t cut. (I know this sounds contrary to mainstream narrative, but that is what empirical data shows). Let’s see.

I think CAMS movement against the Index was primarily due to its majority revenue coming from MF business. But going forward(long term), I think there would be bit of divergence from this view as its business is getting diversified to other areas.

Damodaran had argued similarly. As I wrote this, I realized RBI cut rates.

I came across American Express business - it charges 2.5% to the merchants. However, the best part of it was that, it’s revenue increases with inflation. As the inflation rises, the price of goods and services also rises and given Amex still shares the same (2.5%) over the years, the revenue still increase as over all prices surge.

Given that, if we consider CAMS in place of Amex (don’t comment that how they can be same, there is no comparison and all). Consider clients of MF as customers (Customers using Amex, MF as Merchants) and customers buy MF, CAMS charges the MF for the transaction, over years, MF increases their prices with inflation. Does CAMS increase their prices with inflation, or it lowers the prices as MF size increases over the years?

Just for discussion. I’m holding CAMS from lower levels.

They follow ‘inverted pyramid pricing mechanism’ where, as the AUM of a fund house increase, the pricing reduces or does not increase by the same magnitude.

Please go through the thread, its extensively discussed.

CAMS follows an inverted pyramid pricing model, its fees per rupee of AUM will shrink, but total AUM growth can offset the lower fees.

Mutual fund AUM in India has been growing at ~15-20% CAGR, which can sustain CAMS’ growth despite lower fee rates.

Risks: 1) During bear markets, redemptions increase and new inflows slow, impacting revenue.

2) If rivals like KFin Technologies cut prices aggressively, CAMS might have to reduce fees further.

I was thinking, if you invest in CAMS vs any AMC (Nippon AMC or Aditya AMC).

What is the difference in the returns that we get?

What will be more convenient holding?

Just a question, I was eyeing on NAM India AMC!

Very nice analysis @Chandragupta . Do you see similar corelation is case of AMC stocks as well such as HDFC AMC?

| Division | Revenue Growth | Key Highlights |

|---|---|---|

| Overall | Just short of 28% | Despite a slowdown in capital markets, CAMS reported strong revenues, profits, wins, product launches, and market share gains. EBITDA grew by 34%, and PAT grew over 40%. |

| MF | In excess of 28% | MF revenues grew on the back of about 38%-39% growth in assets. CAMS won all 3 MF-RTA mandates on offer: Jio BlackRock, Pantomath MF, and Choice. Won the second MF-RTA migration mandate from competition. Equity assets crossed the INR25 lakh crore mark. Net registration share increased to 64% from 60%. |

| Non-MF | About 22% | Despite market conditions, non-MF revenue showed substantial growth. Share of non-MF revenue is at about 12.5%. |

| CAMSPay | 53% | Stellar revenue growth driven by digital payments. Added almost 24 new logos in Q3. Empanelled by LIC for auth and payment gateway services. |

| CAMS KRA | 27% | Grew despite a slowdown in new account openings. Added 20+ new financial entities and one of the top 5 brokerages. Launched WhatsApp KYC. |

| Alternatives | Not explicitly stated, but included in non-MF growth | Added 21 new clients. CAMS WealthServ had almost 185+ sign-ups. GIFT City now has 25 clients managing over $1 billion of AUM. |

| Repository (REP) | Not explicitly stated | Scaled to INR10 lakh a quarter. Won a second life insurer, Star Union Dai-Chi, to give 100% of their policy base. Bima Central unique base crossed 4 lakh consumers, volumes grew 40%. |

| CAMSfinserv | Not explicitly stated | Won a mandate for account aggregator, TSP, and analytics from one of the largest scale banks in the country. Think360 won a TSP++ analytics mandate from a top bank. |

Key Observations:

I was going through AMC businesses, I figured that most of the AMCs are going through pricing pressure. Most of them increased their management fees and then reduced it.

Apart from that, I see CAMS isn’t facing such problems. However, if someone is betting on digitalizing of India, and Indian Markets. One should go with CAMS and CDSL rather than a specific AMC or Broker (I haven’t studied brokers yet).

Equity MF inflows at ₹29,300 crore, among lowest in FY2025 - The Hindu

Not all that bad I guess, in the context of the brutal carnage we have seen non-stop for 6 months now. Net inflows into equity at Rs.29,300 crore. Can offset FII outflows of about Rs.1,000 crore per day, though their current run rate is higher than that. Monthly SIP inflows at Rs.26,000 crore, with 44.6 lakh new SIP started though terminations are higher than that. Purely in terms of sentiment, we probably saw the worst by February end I think, and March seems to be marginally better so far. From April, annual increments and tax cuts for the middle class will come into play, boosting consumption (& SIPs!).

Risks if any, are mainly from Uncle Sam but even here, a lot of Trump’s Tantrums will start getting discounted. Markets don’t fall for the same reason twice, they say. Let’s see.

in March people will do tax loss harvesting as well i guess which will add to the selling pressure but all in all i too feel we are almost at the end of the carnage provided the upcoming earnings and gdp data doesnt go haywire

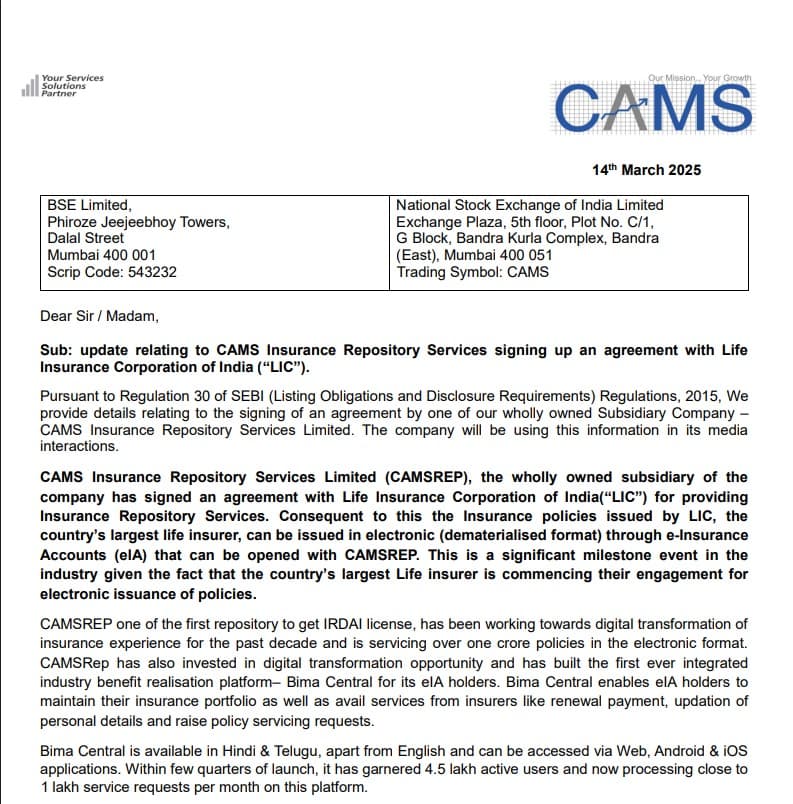

CAMSREP, subsidiary of CAMS, has signed an agreement with LIC to provide Insurance Repository Services.

LIC policies can now be issued in electronic (dematerialized) format through e-Insurance Accounts (eIA) opened with CAMSREP.

This is a major industry milestone as LIC, the largest life insurer in India, is starting electronic issuance of policies.

CAMSREP, one of the first IRDAI-licensed repositories, already manages over 1 crore e-policies and operates Bima Central, a digital platform for policyholders.

The platform has 4.5 lakh active users and processes nearly 1 lakh service requests per month.

CAMS | Outlook 2025

CAMS signed agreement with LIC to provide insurance repository services.

LIC will move new issuances, not legacy policies, into this new architecture.

Insurance repository business can grow 25-30% next year by FY26.

Watch the interview here

LIC has also entered into same agreement with CDSL.

LIC is shareholder in both CDSL and CAMS.

What does it signify of LIC entering into same business agreement with 2 different companies?

my understanding is, end customer can choose with whom to open a Insurance e-Rep account. It is similar to having a Demat account with either CDSL or NSDL.

Edit: For Demat, This is true if the broker has tie up with both NSDL, CDSL. Just call the Broker’s Backoffice/customer service team, how this can be done even for online applications. They can map the CDSL/NSDL mapping in the backend to your application form. For physical, they will have options to check box or different application forms. Just ask your Brokers Team. Brokers also open a stand alone demat accounts this way. I have done this with Sharekhan / Geojit earlier. Zerodha has only CDSL tieup now, so NSDL may not be possible now.

we don’t get to choose CDSL/NSDL, the broker decides who they want to go with and we are stuck with them.

Edit: Thanks Garuna, I was not aware.

We can choose. I requested them to do that while opening my account.

I was going thru the Annual Report fy 24 of CAMS. In the notes of income statement i saw the Recoverables as a part of revenue from operations. I am not able to understand it. Can anyone help to understand please.

As stated in annual report:

’ Recoverables represent expenses incurred in relation to services performed that are allocated and recovered from the customers based on the agreed terms and conditions of the agreements entered into by the Company with each customer.’

eg: Imagine CAMS has to send a physical account statement to an investor on behalf of a mutual fund. The cost of printing and mailing that statement is an expense CAMS incurs. If their agreement with that mutual fund allows them to “recover” such direct costs, CAMS will then bill the mutual fund (or potentially the investor, depending on the agreement) for the cost of that statement. This reimbursement is the “recoverable.” (AI generated)