Market did not react that well to results initially. But today stock price has given breakout, with 14% gains since last 5 days.

Is there any news?

So what would be the target for this stock basis the breakout on chart?

@Anubhav_Garg maybe near 3750 3800

2 Likes

- They have done a very large transformation in one of the top private sector banks, We will see some announcements in December

7 Likes

Here, I try to dissect the latest conference call by separating it into 4 parts.

- Improve Business Understanding

- Forward-Looking Statements by the Management

- Possible Positives

- Possible Negatives

This is not a recommendation to buy/sell. Purely for educational and informative purposes.

1. Improving Business Understanding

-

E-Insurance is a new venue for the company. Earlier, eIA was relevant for the life insurance industry, but now it is seeing renewed interest from non-life insurers also. The company has tied up with the top 5 of the 50 insurers in India.

-

CAMS KRA is the fastest growing segment for the company which provides e-KYC solutions to brokerages and MFs. It has seen 100% growth in the last year (from a low base).

-

The margin for the MF business is the highest at around 44.5%. In the future, KRA and AIF businesses should also approach these levels of margins. Payments Business is currently at 30% but it can reach 40% with a limited amount of scaling.

-

There is a huge Total Addressable Market for the Account Aggregator Business. Services include - Verification, Digital Lending, KYC, NFO Onboarding, 3rd Party Verification of bank accounts.

-

It is the paper transactions which are generating revenue for the company. NOT Digital Transactions.

-

The Out-of-Pocket Expenses borne by the company while servicing clients are added to compensated for by the client himself and hence added to the Revenue of the Company.

2. Forward-Looking Statements by the Management

-

~20% Revenue Growth in the next 12-18 months. MF Business should be slightly less than 20% and non-MF Business should be slightly more than 20%.

-

Margins are expected to hold at 44% or slightly improve from here. Payments and Insurance business can be at 40% margins in the next 3-4 quarters.

-

Operating Expenses (with Out-of-Pocket [OP] Expenses) / Revenue with OP Expenses) = ~12%

-

Operating Expenses less OP Expenses / Revenue less OP Expenses = ~7.5%

-

Fixed Expenses have peaked and will not see further increases (apart from inflation-driven). The only increase expected will be in salary expenses (~34% of Revenue). There is no big lumpy expense in the immediate future.

-

A very large transformation has been done for a large private sector bank using Fintuple. The announcement is expected in December.

3. Possible Positives

-

All Public Sector banks have come on board the Account Aggregator Platform. Huge TAM due to Fintechs.

-

Net Monthly SIP Collection at the CAMS level has grown 2.5x to 10,000 Croresin in the last 3 years.

-

There is no price resetting event in the next 4-5 quarters and the price depletion is now over.

-

The company is expected to benefit from Operating Leverage with a greater portion of incremental revenue flowing to Net Profit.

4. Possible Negatives

-

Digital Transactions such as SIPs, Triggers, etc do not create any incremental revenue for the company and there is no incremental cost either. In the future addition may have to be done in terms of server capacity (not in the immediate future).

-

There has been a huge price depletion in the Account Aggregator business to the extent of 80% i.e. company can charge only 2rs where it used to charge 10rs.

16 Likes

Rs 250 SIP in MF could be a game changer for MF industry and CAMS/ Kfin?

3 Likes

Thank you everyone for sharing your thoughts. Very insightful discussion.

I had questions regarding the current board structure and incentive for current management to perform. If we look at the current shareholding pattern, HDFC Bank and LIC are the biggest shareholders followed by Seafarer Overseas Growth & Income Fund and Ashish Parthasarthy.

Following are concerns:

-

No entity has any significant share to be sufficiently incentivized and have skin in the game. Am I correct in my inference or there’s some other agreements/details that I am missing?

-

Previously, Warburg was the majority shareholder (around 30%). Unlike Warburg which operates as active investor, HDFC and LIC seems like passive investors. Does this mean that the board oversight over management, business plans, and objective will get impacted?

It’ll be great to get some perspectives on these.

Thank you.

4 Likes

The results are quite good, and I am surprised at the muted market response to the results. Gross margins are the highest ever, operating margins and PAT margins have improved further and are now close to 45 % & 30 % respectively. Non-MF revenues have shown strong growth, and the management says 4 of the 6 businesses have grown by more than 20 %.

CAMS KRA revenues more than doubled, and it added 25 new financial institutions and FinTechs as customers during the quarter. The PayTM issue will provide additional tailwind to this business, increasing the outsourcing of KYC requirements by all entities in the financial ecosystem to reliable external partners like CAMS.

The addition of multi-currency capabilities to fund accounting is another big positive, as it increases of the TAM manifold. Technically, this has a market not only in the GIFT City zone but CAMS can offer fund management services even to entities abroad like in global financial hubs, who are willing to outsource their back office to India.

As non-MF businesses achieve scale, margins should improve further as costs will not rise in the same proportion as revenues. Meanwhile in the MF space, the SIP mania shows no signs of slowing down.

22 Likes

Thanks Chandragupta for sharing your insights.

I believe that the stock has limited but steady growth potential of 10%+ compounding returns for a very long time, which in my opinion is a very good outcome.

Following are my reasons:

-

Slower PAT growth: 3 years (FY20-23) has seen PAT growth of 19%, which might be difficult to replicate going forward as the levers that helped have weakened - (a) Rapid growth in new retail investors post pandemic will taper from its peak, (b) rally in asset prices due to lower interest rates will be difficult to replicate in higher interest rate environment, and (c) non-MF business which is growing faster will put downward pressure on margins until they hit the required scale to become margin accretive.

-

Case for PE de-rating: Due to slower PAT growth, we may see PE multiple de-rate from current LTM 45x.

-

Secular growth drivers: I expect 10% minimum return basis following back of the envelop calculation - over the long term (Mar 2010-Mar 2019), MF AUM has grown at 16% CAGR and NIFTY delivered 9% CAGR. This implies that the volume growth has been around 7% (16%-9%). This in a way reflects new investors coming in, higher investment per investor, etc. Going forward, the growth will be slower given a higher base, hence we can assume a 1% reduction in this secular growth, implying 6%. And the NIFTY CAGR can also be assumed to be 1% lower over a long term, thus 8% CAGR. Thus, we can expect MF AUM to grow at 14% CAGR. Management highlighted that typically revenue grows at 4-5% lower than MF AUM growth due to tiered pricing structure (lower pricing for higher AUM). Thus we can expect revenue growth to be around 9-10% growth. On this we can expect some additional growth by non-MF business which is growing at 20%+, thus overall revenue growth can be higher than 10%. On this, we can expect operating leverage (although weaker than before). Hence, EBITDA and PAT can grow at 10%+ too. Thus, we have sufficient margin of safety to absorb any PE derating.

On top of these, as Chandragupta highlighted, the company can increase its TAM by serving foreign currency funds. Also, earnings predictability is immensely high in this business. And with good business models and good management, neither investors nor management can fully foresee all the amazing opportunities that might open up in the long term because we don’t have the crystal ball to predict the future ![]()

Hence, I find totally worth it to hold on to wonderful businesses and ride both the strong and not so strong periods.

Disclosure: slowly building position in the stock

10 Likes

Computer Age Management Services Limited Q3 FY ‘24 Earnings Conference Call February 07, 2024

-

Unifi is a very prominent PMS provider based in Chennai and has aspirations to operate a mutual fund. They were one of those 10, or 11 entities that had applied for a license in the last about 18 months

-

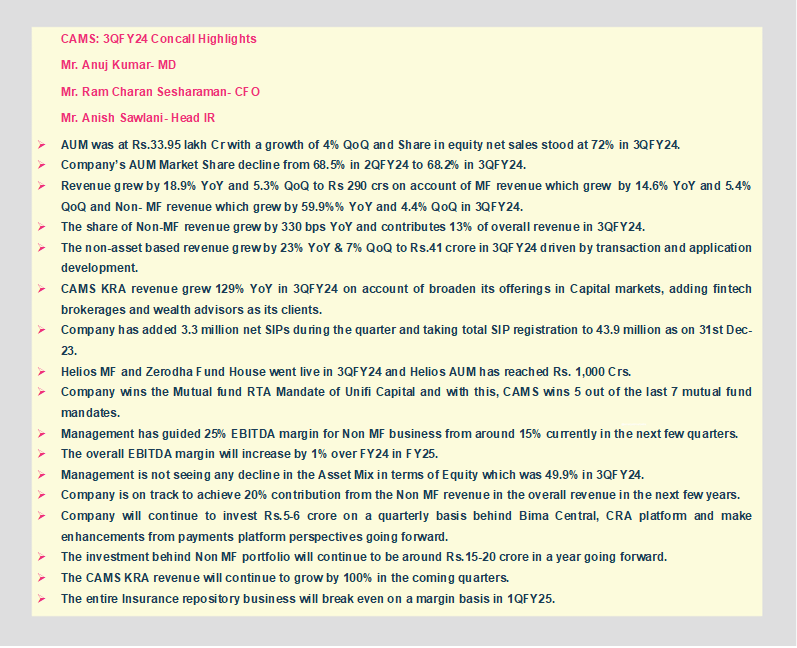

Mutual fund assets stand at about just short of INR34 trillion, INR33.95 trillion

-

Our overall market share stands at 68.2%

-

SIPs grew 29% year-on-year. The industry grew by 19%

-

Helios Mutual Fund and Zerodha, both went live during the quarter

-

Non-mutual fund businesses:

This has grown about 3.3%, so 330 basis points. The share of non-MF is at the rate of 13% now -

CAMS KRA:

Where you’ve seen that we’ve declared over 100% revenue growth at 129%. From an entity, which used to largely cater to CAMS service mutual funds, we’ve gone beyond CAMS service mutual funds across all of them. But now that alone, from a fintech brokerage, and wealth advisory perspective, all these entities need KYC and KRA services, and CAMS KRA has brought in a large number of customers in the last 12 months to both broaden our clientele and scale revenue -

CAMSRep:

Has gained entry, and you know that the non-life segment also now has KYC as a mandatory step before you purchase insurance. So we have won the mandate for Oriental Insurance to do KYC for them, digital KYC. This is a joint go-to-market and a joint offering between CAMSRep and Think360 -

CAMSPay:

We have won an exclusive partner status from LIC to execute customer account authentication. This is largely third-party verification of accounts of people who wanted to buy insurance and are stepping in digitally. -

CAMS, the overall revenue book grew just short of 19%, at 18.9%. Within the MF, revenue grew 14.6% year-on-year. Non-MF grew a staggering 59% year-on-year

9 Likes

From a Motilal Oswal Research Report dated 13 March 2024 available in public domain:

On AIF / PMS:

CAMS commands ~ 50 % market share among AIF / PMS funds utilizing RTA services

On ThinkAI

Data, Algorithm, and Applications are the three pillars of AI. The share of digital lending now accounts for 30 % + of all lending and fintechs, providing 95 % + digital lending solutions.

Among others, Think360’s flagship alternative credit scoring product, Algo360, is India’s leading alternate data solution, which powers income estimation and risk estimation based on device data. CAMS and Think360 bring exciting synergetic opportunities, (its “GenAI” capability completed its first engagement with an international client) to transform customer onboarding and drive smarter decisions.

Management expects this business to scale up exponentially given its low base. As of 9MFY24, this business contributed 1.6 % of the total revenue.

On Account Aggregator

The National Financial Information Registry (NFIR; announced in Union Budget 2023-24) aims to change the way credit is distributed and underwritten to new-to-credit (NTC) and underbanked borrowers. The focus is to facilitate cash flow-based lending and economic inclusion. The AA network went live in Sep’21 and is still in its nascent stages. NFIR, when integrated with the AA system, will have a game-changing impact on the domestic financial services industry.

On Insurance Repository

The potential e-insurance policy market size is ~ 500 m and the revenue potential is likely to be ~ INR 5b annually. Considering the competition, even if the prices deplete by 50 %, the market size is expected to be ~ INR 2.0-2.5b annually.

6 Likes

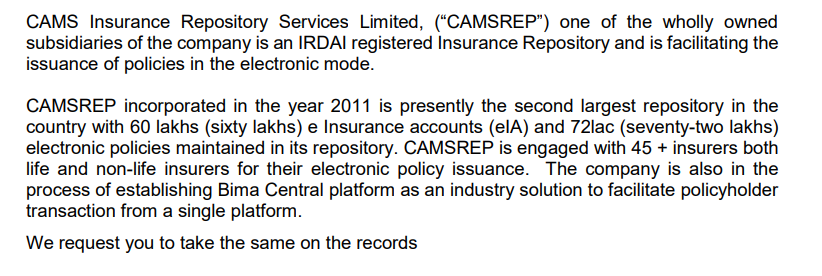

Insurance Regulatory and Development Authority of India(“IRDAI) has notified the Insurance Regulatory and Development Authority of India (Protection of Policyholders’ Interests and Allied Matters of Insurers) Regulations, 2024 which has mandated

the issuance of insurance policies by insurance companies in electronic form with effect from 1st April 2024.

How will this benefit CAMSREP and the Bima central platform they are trying to establish? Requesting senior members to share their thoughts.

Regards,

Suhag

1 Like

CAMS gets RBI approval to operate as an online payment aggregator.

2 Likes

Q4FY24 Results Update

There is a consensus regarding CAMS that growth is not secular but shallow cyclical owing to the dependency on MF based revenue which ebbs and flows depending on whether bulls or bears are in charge. Thus, it is heartening to see the strong results coming from the optionalities that CAMS has been working on to make its growth more secular. Highlights from the Quarterly results is as follows:

- MF based revenue

-

Asset based revenue has increased 21% YoY for Q4FY24 and 12% YoY for FY24. Non-Asset based revenue has increased 28% YoY for Q4FY24 and 20% YoY for FY24.

-

Equity component of the AUM stands at 52% for Q4FY24 (Q4 FY23: @ 46.1% / Q3 FY24: @ 49.9%). Equity component for FY24 @ 49.1% (FY23: @ 45.0%)

-

The non-asset based revenue for MF is not expected to be impacted by digitalization. As per management, about 8-11% of paper based transactions still come contributing to transaction fee. Furthermore, non-asset based revenue is expected to grow further as more and more call centres are opened, more and more people subscribe to CAMS APIs and applications. The company doesn’t see any big moderation happening in growth of non-asset based revenue given that the paper transactions continue to be range bound in terms of the percentage of total transactions. And the other components of this non-asset based revenue being on a upward trajectory even when digitalization happens.

-

AUM fee growth to AUM growth is expected to be in the range of 70%. Can vary a little but ultimately company guided for reversion to mean.

- CAMS Alternatives

-

Services provided to AIFs include data processing, reporting and MIS, reconciliations,

fund accounting services, corporate actions/tax-related support, investor servicing

and record creation, drawdown and collection management, and intermediary

revenue management -

Over 50% market share among AIFs and PMS which avail RTA services.

-

24% revenue growth YoY in Q4FY24 and 18% annually over FY23.

-

Good number of client additions (32) with positive reception in GIFT City (17 total). Total AIF+PMS is around 1000. CAMS services around 250.

-

Digital onboarding has increased, Multifonds allows for multicurrency fund accounting and reporting and is a good addition to services being offered by CAMS, Fintuple’s platform integartes custody services of banks, AIFs and PMSs which opens up avenues in FPI, forex and treasury services are some of the triggers.

-

Revenue in AIF business is not directly linked to AUM. Less than 25% billing is AUM linked, mostly it is linked to number of investors onboarded

-

AIF revenue is primarily annuity. Onboarding revenue and implementation revenue is minimal, rest is annuity in nature. Revenue may vary across the life of fund as new funds get launches and old ones fade away, however, CAMS sees around 1.5 bps of yield. Currently INR 2.2 Tn is the asset under service (which makes it revenue of 33Cr, overall non-MF revenue is 41Cr in Q4FY24)

-

View of management regd AIF market size (Q3FY23):

"AIF on the other side, have been significantly embracing outsourcing. You will see that from a total registered count perspective, there are almost 1,000 AIFs in the country, everybody may not have launched. We service about 200 of them. A lot of them may have outsourced or may have bought outsourcing services only for onboarding and TA kind of services. Now of course, you know that demat has become mandatory. So that and then fund accounting and other fund administration services, I would still say that the non-outsourced part is still quite large, it is sitting there.

*Most of the new funds that get launched are getting launched in a captive manner, which means *that they are priced and not coming to us, still they scale to, let’s say, beyond 100 investors or beyond a critical mark. So that, again, from an outsource versus non-outsource revenue perspective, you can say that we’ve perhaps touched less than 50% what is out there. Most of the large AIFs, of course, have outsourced. So they are customers, but there is a significant number, several hundreds of them, which can potentially become clients over the coming years. That’sfairly the addressable market for you"

- CAMS Pay

-

In Q4 FY’24, revenue surged by ~20% compared to Q3 FY’24, culminating in a year-end total revenue increase of 24% compared to FY’23

-

CAMSPay received the final authorization to operate as a payments aggregator, from RBI

-

Pioneer of UPI Autopay, payment authentication services (replacement of penny drop).

-

gone live with the authentication services for LIC and further planning to do Payment Gateway kind of work with Indian Bank, Bank of Baroda and Canara.

-

Greater than 50% market share in MF ecosystem.

- CAMS KRA

-

CAMS KRA continues to bolster its product superiority and is emerging to be a preferred KYC service provider – delivered a robust 90% YoY revenue growth in Q4 (28% growth QoQ)

-

Added 20 new financial institutions and FinTechs as its customers, significantly adding non-MF PANs to its stock

-

KRA’s seamless onboarding journey, powered by Think360’s Kwik ID KYC solution provides a compelling product suite to fintechs to build a frictionless journey

-

For KRA business, to close the gap with onboarding new PANs is critical. Company was earlier focussed on MFs serviced by CAMS but is now looking at the entire set of MFs, brokerages and large fintech as potential market (3x to 4x of earlier market). Within brokerages winning big would mean converting one of the top 2-3 brokerages.

- CAMS Rep

-

Only PDF issuance of policies mandated as per IRDA. So the immediate market unlocking that was expected is not happening. Company sees gradual ramp up over next 2-3 years.

-

Atal Pension yojana opened by regulators for CRA where Protean is the market leader. As per management, market pricing is thin in the segment and customer switching is not expected (focussing on onboarding new customers)

- CAMS AA / Finserv

-

expecting that in FY’25, account aggregator will also start making its presence felt in terms of making at least some increment to company financials, very small, but it will do that.

-

13% market share for customers successfully linked to AA ecosystem

-

Preferred AA partner in F&O account opening usecase

- CAMS Think (AI driven solutions)

-

Think and Rep won insurance KYC contracts from SBI General and Oriental Insurance

-

Received empanelment confirmation from India’s largest bank, State Bank of India, for its flagship product Kwik.ID and multiple other offerings

-

Commenced the AI and Analytics transformation initiatives at Moneycontrol

-

Deployed flagship alternative data enrichment and credit scoring product Algo360 for AngelOne, leading financial services firm

-

Partnered with CAMSKRA to embed KwikID’s industry leading KYC and onboarding capabilities

-

On pricing for non-MF Business: don’t worry too much about predatory pricing because a lot of CAMS’s competitors are stable, which means that one guy trying to just gain share basis asymmetry in price is something we don’t see often, prices have – in general, as consumption goes up, prices dwindle down. Across segments pricing is getting to a stable place as the number of transactions is increasing.

-

EBITDA Margins for non-MF business has crept upto 20% from 15% earlier. Targeting 35-40% steady state EBITDA margins in long term. Margins peaked in MF business. Overall margin guidance between 45 and 46% driven by operating leverage in non-MF business (7 cr quarterly investment in platform)

-

In terms of growth potential for non-MF, focus in on KRA, Pay and AIF in the lead.

9 Likes