Some take on valuation

9 Likes

2 Likes

Flattish(or slight de-growth) growth but extremely detailed presentation.

CAMS.pdf (1.7 MB)

2 Likes

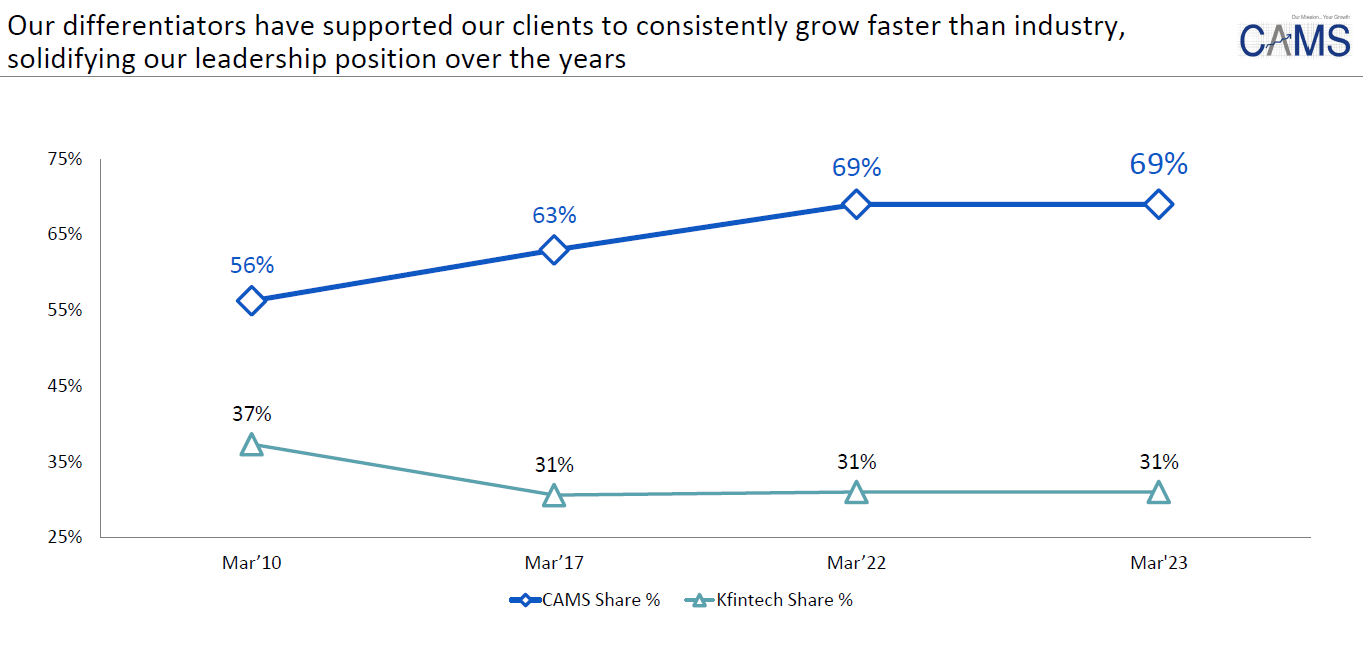

I was going through presentation of both CAMS and KFINTech. We now have both as listed players. It seems like both claim that they are growing faster than market. Has any one done a comparison between the two? Would like to seek opinion from the community.

7 Likes

Interesting purchase by Goldman Sachs AMC (Singapore) 4.99% of capital. Not a promoter but I expect other similar purchase before a Strategic sale of the same happens. It is likely that this would be taken private post the strategic purchase.

Disc: Invested. No trades in the last 30 days

2 Likes

NAVI Mutual Fund is changing their Registrar & Transfer Agent (RTA) from KFintech to CAMS.

http://pr6.saymails.com/mfuindiasmt/preview.php?nc=vm&m=609&u=AAgGU10MVwo=

8 Likes

The optionality provided by various ‘other’ businesses is the main attraction in CAMS. I expect the core MF business to grow at around 8 % at the most. If there is a broader bull run, it will grow faster. The company has said they want to take the revenue outside of mutual funds to around 20 % of company revenues. This year the non-MF share of the business crossed 10 % for the first time, growing 9.3 % YoY for the year.

The Insurance repository now holds 5 million e-policies, a growth of 33 % over end-FY22. As of last quarter, CAMS apparently had a 33 % market share of this business. But the insurance repository earned less than a crore last quarter apparently. The main trigger for insurance will be the expected regulatory push which everyone is waiting for. There are apparently 40 to 50 crore policies to be dematerialized, and this will be a Rs.150-200 crore size industry as a conservative estimate. Here CAMS can charge for policy conversion and an AMC. Interestingly, Mr. Anuj Kumar said in the concall it may be difficult to charge for transactions, looking at what we see elsewhere in the financial digital ecosystem. This view is quite a dampener, as transactions were really the one supposed to be the big money spinner. (Conversion will be a one-time revenue and AMC will have its limitations. Transactions will be recurring and scalable).

The KRA business has more than 10 million records in its repository but does not earn any direct revenues apparently (at least not worth mentioning). Here competition has increased as more KRAs entered the market. BSE launched its KRA service from October last year. The e-NPS revenues were up 50 % but its size is quite small in absolute terms.

The Account Aggregator business added 20 plus sign ups, taking the total customer count to 79. The company bought out Think360.ai which can process Android SMS data and bank statements to give consumer insights. But the revenue model for AA is yet to properly evolve.

The Payments aggregator license has been received in February 23, but this is also a very competitive field, and I am doubtful how profitable this would be in the long run. The company says it has shown 27 % growth in revenues and “unprecedented” merchant additions.

The AIF business is the one which is doing the best, apparently brought in 2.9 % of the company revenues, which comes to around Rs.28 crore.

All the subsidiaries put together have brought in Rs.43 crore of revenue for the year FY2023, this is Rs.3 crore less than the Rs.46 crore brought in last year in FY2022. At current price the company trades at a market cap of Rs.10,000 crore and P/E of 36.

Until the insurance regulation kicks in, or a broader bull run, not much price action can be expected.

(Disc: Holding)

17 Likes

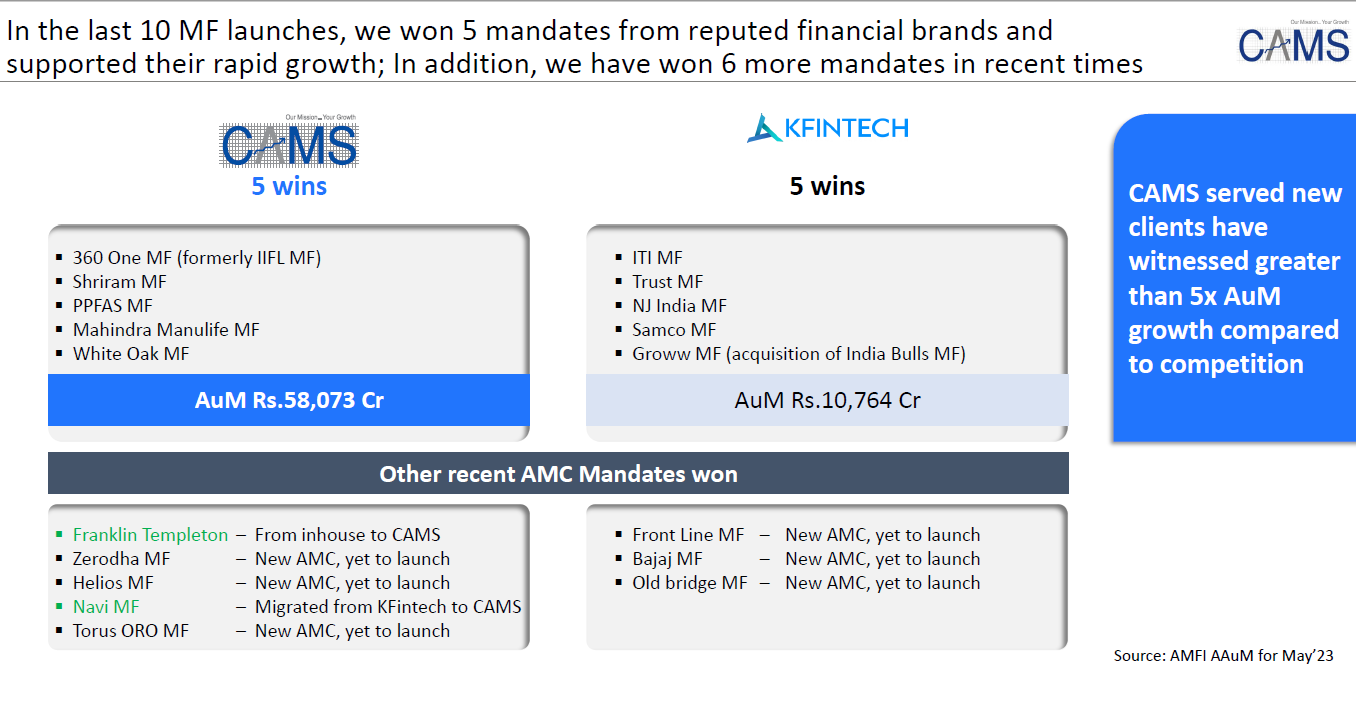

Interesting…CAMS adds two new comparison slides to their PPT:

10 Likes

CAMS served new clients have witnessed greater than 5x AuM growth compared to competition

These are either new AMCs or smaller AMCs except PPFAs, so the AuM is low for them, and the AuM becoming 5x or 10x is not big in absolute number of crores. Also, what would have CAMS mentioned if those AuM did not grow.

On a different note, it is a little surprising to see so many new AMCs which have come and will be coming. Maybe interest in equities from retail via MF route is indeed true, maybe not to the extent it is portrayed to be, but looks like a theme as of now, with the usual caveats applied.

No investment, had a position before, interested.

2 Likes

What is the reason for lack of competition for CAMS? Is this moat impenetrable? Can a change in regulation upend their business model?

Is HDFC opening its own RTA? I don’t see HDFC MF investments in my All RTA report generated from mycams app. I don’t see them in mycams app or even in Kfinkart app

1 Like

3 Likes

2 Likes

4 Likes

The holdings of the promoter have reduced significantly… anybody here who can explain the reason behind it?

1 Like

Great terrain is associate (corporate structure) of PE firm Warburg pincus. Nature of PE firms to liquidate and monetise investment bets.

1 Like

464a83e8-759d-409d-a955-45adc2cb6531.pdf (266.3 KB)

Change in Management

CAMS Q2 Result,

YoY:

- Revenue at Rs. 275.08 crores, 13.5% on y-o-y basis

- PBT* at Rs. 113.28 crores, 16.8% on y-o-y basis

- PAT* at Rs. 84.51 crores, 17.1% on y-o-y basis, PAT margins @ 29.7%

QoQ

- Net profit up 11% at ₹84 cr vs ₹76 cr

- Revenue up 5% at ₹275 cr vs ₹261 cr

- EBITDA up 11% at ₹122 cr vs ₹110 cr

- Margin at 44.4% vs 42.1 %

My Take

Growth is muted, as compared to CDSL. Would expect better Q3 results on account of:

- Zerodha AMC and 3 other Mutual Funds wins

- CAMSPay UPI and KRA

- Think360AI (Generative AI Play)

Disclaimer: Invested 5%

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d3dc33ac-36e7-4cf2-8e87-79df765c9447.pdf

6 Likes