Finally, next week some funds flow in, after OK from Yes bank and Govt depts

Does anyone know whether the exchange have an option not to suspend the trading in case of non filing of results. Also what should a retail investor do in such cases.

Does anyone also think there might be more issues coming from the forensic audit?

What will happen post Feb 3rd? Can someone with knowledge please explain?

Similar thing I think already happened with Manpasand beverages about a month ago. They did not meet the listing requirements. After warning, they managed to publish all results within a month, their backlog included since AR FY19 also, but did not pay the fine. Now, it is being traded first day of every week till about 2-3 months more before trading stops.

NSE ticker changed to add “BZ” showing regulatory risk flag about 3 weeks ago. BSE showed no change. Exchanges should send more info directly to holders, since they already send trivial things like daily trades etc.

Do not know about the re-listing requirements but they should be able to meet some requirements and came back.

Thanks to comments from fellow boarders I divested majority of my holding, still feel they will manage ok, just that gains are pretty low for the risk.

Disc: Actually I had fully exited but added back a small quantity in between my 2 previous posts.

Today this hit LC again. Is there any value left in this company? They are replaying their debts. Any chances of survival here?

I thought this was suspended, but apparently not!

Read somewhere that they will not disclose results of investigation till deal making is going on, I forget the parties interested. And till the investigation is deemed complete they cannot publish results. So, here we are in the dark, only punting is possible, if your money is not that precious to you. No way of finding out the finances and intentions are not even remotely investor friendly. Get away asap and stay away.

Disc: exited the little position of previous post, soon after.

PS: Investigation report leak

Hi James,

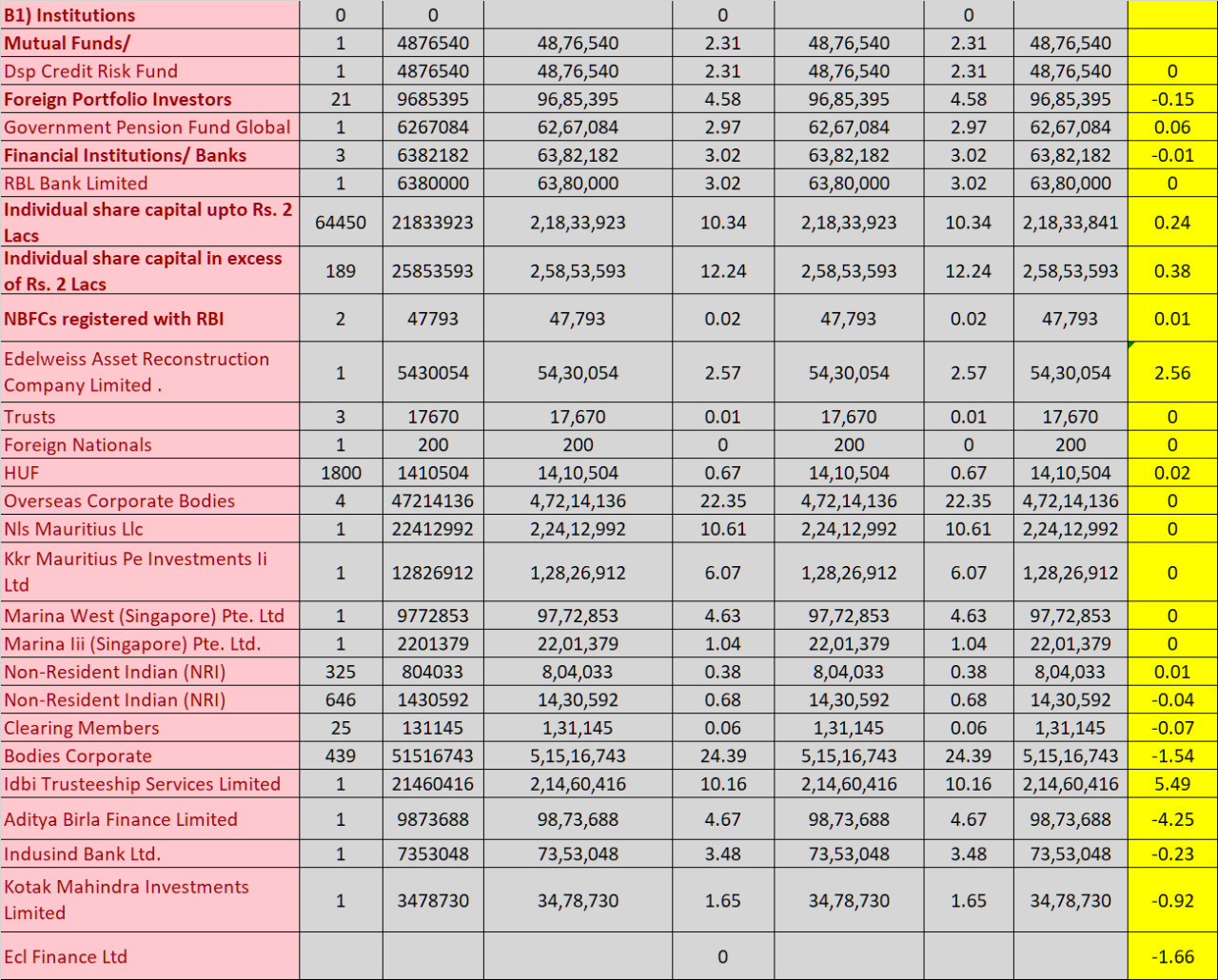

Thanks for sharing this information. I wasn’t able to find any info on the internet about the change in shareholding.

Can you share your source as well.

Thanks

This is from excel where I compared the last 2 Share holdings. To get both, you can check in BSE site.

Also, I am new in Investing and have been trying to sell my CCD stakes from last 2-3 weeks. However, every Monday when I submit by bid at 9:30 a.m. the cirucuit has also hit for the stock and I end up seeing my stock going down and down.

Is there any way to sell my CCD stock in this scenario.

I was able to exit some such positions (stuck in LC) by placing an AMO (after market order) or GTC (good till cancelled), one day before, so place one on Sunday/Saturday (check when ticker is enabled). This is while using Zerodha Kite. AMO are enabled for the next day exactly after 4pm on the preceding day (but excluding Friday, when considering the weekend, is what i have noticed).

Do this at the earliest possible time to be in the head of the queue. Pre-open will start at 9am, price discovery trades start at 9:15am.

2 Likes

1 Like

Investigation Report Synopsis — http://www.bseindia.com/xml-data/corpfiling/AttachLive/01990559-a064-496d-acea-a0cd04a20789.pdf

2 Likes

3 Likes

This forum is silent meanwhile company has done wonders in turnaround and stage is set for multi bagger returns. Debt reduction with less than 2k Crore now which is likely to further go down as per plan which is hinted in annual report. https://coffeeday.com/PDF/AnnualReport_2021-22_CDEL.pdf Management believes that the change in shareholding is temporary in nature and the shares pledged will be released back to the Company. … The subsidiaries of CDEL are in the process of disinvestment of their assets. The company is confident that the subsidiaries will repay these advances in due course. …These standalone financial statements for year ended 31 March 2022 have been prepared on a

going concern basis in view of the positive net worth of the Company amounting to Rs.30,673 million as of 31 March 2022, significant value in diversified portfolio of investments held in subsidiaries / joint ventures / associates, established track record of the Company to monetize the group assets as demonstrated by sale of stake in Mindtree Limited, sale of Global Village Tech Park owned by its wholly-owned subsidiary Tanglin Developments Limited , sale of stake in Way2Wealth Group entities profitable resorts operations and consequential ability to service the obligations… Some events will trigger it to cross all time high

4 Likes

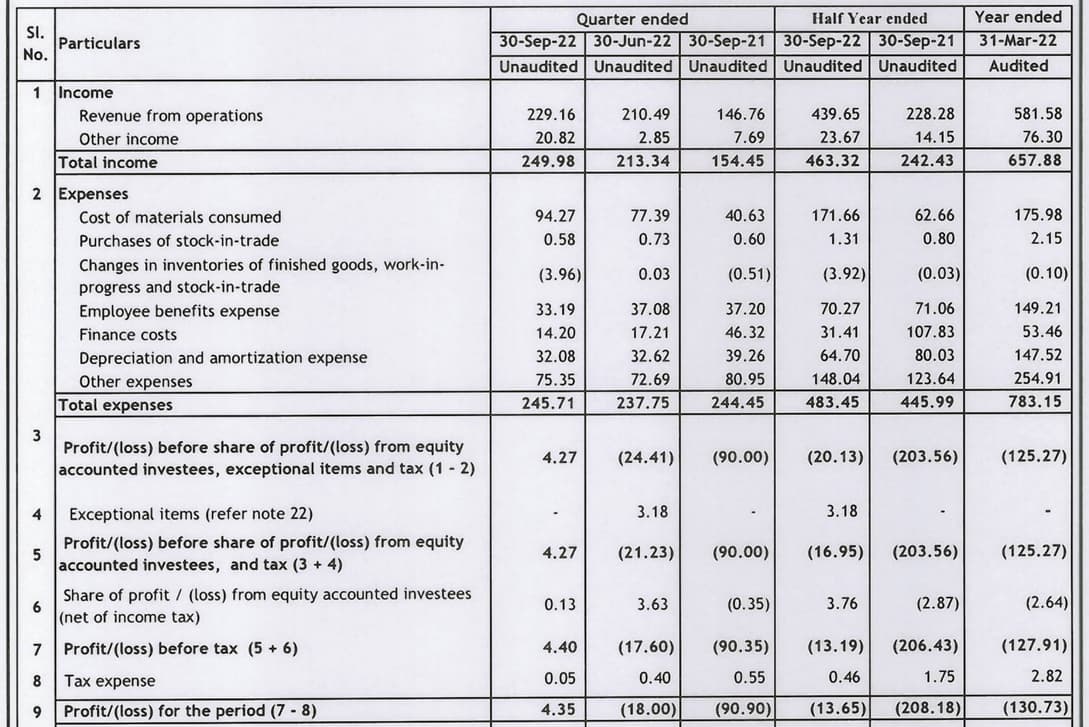

Company reports good progress on turnaround in Q2 with increase in topline and bottom-line in black. Will show vertical climb in valuation like it fell from highs in next few quarters given valuation of QSR category

2 Likes

My first post here fellow investors. Comments & Criticisms invited. Thought I’ll start with something simple, a beverage firm.

Disclaimer:

No buying or selling advice, but I am invested.

CCD, Coffee Day Enterprises, My reasons to get-in.

-

Though Coffee is extremely common in South, it is however, an Aspirational Drink for other 3 regions. CCD’s sector, QSR, in India, is expected to grow at 20%+ CAGR in the next decade, with the changing food habits & an exponential rise in disposable incomes of the Middle Class.

Many within the present 15-30s age cohort, who’ve seen MBA-Chaiwala, ChaiS Bar, Chayos etc as their go-to hangout place, some of whom would eventually gravitate towards a higher-brand, ready to pay that little extra as Premium. Consequently, they’ll either go to CCD, city-level boutique Coffee-Shops, Starbucks(scant presence, high prices) etc. Similarly, the 30-60s age-cohort, which has basically grown up on CCD & is emotionally attached, will continue to keep getting back to it. So, the growth-potential for CCD, if/once it survives & starts posting profits remains high. -

There is a significant Debt reduction(~7800 Cr to 1800Cr). Though a lot of stores/assets are gone, but QSR Segment doesn’t run all stores in profits either. 80/20 Rule is of high significance in this space. Tata’s during their 2021 buy-out proposal were against running up of some of their subsidiaries, which over the months, CCD has tried to get away with. A step in the right direction. Meanwhile RIL acquired Subway-India, thereby spilling signs of Buy-Out possibilities in QSR space. No point ruling CCD’s own takeover (murmurs of D-Mart/RIL/Tatas), given the zeitgeist of present economy, though remains a wishful thought.

-

Till last Qtr, accounting for reserves, CCD is discreetly profitable, with only depreciation eating the profits in reality. With a book-value of around 171, if the firm simply sticks to survival/profit route, it has all the reasons to aspire for those levels.

Either I win, or I don’t loose approach.

CCD will either be bought(a win) or will survive & revive for a better growth, aspiring for it’s book value, a 3x from here. If one can patiently wait for 2-3 years, this under-rated, undervalued gem can still make a lot happen over coffee!

Assuming we understand the events that happened around 2019, Coffee Day Enterprises, ie. #CCD, #CafeCoffeeDay has the folliwing potential. Would encourage people to ready/watch why CCD collapsed at the first placem to understand what is already priced-in.

5 Likes

What will be the long term impact of this order by Sebi?

Will the CCD (CDEL) will be able to recover 3400+ Cr from MACEL?

From my personal perspective, I think, this will act as a catalyst for CCD.

2 Likes

I am banking on their turnaround performance and subsequent raising of capital or acquisition or strategic investor which they mentioned. Recovery looks doubtful to me, whatever happens will be added bonus

1 Like