Prima facie results look bad and because of 25 crore one time expense which they have to pay in this quarter , Q4 also will have hit. Key is topline growth and vending machines growing by 5% in quarter, top line growth of 4 quarter in a row. They have to find mechanism of raising money or buyer as underlying brand and value is there. Holding with conviction

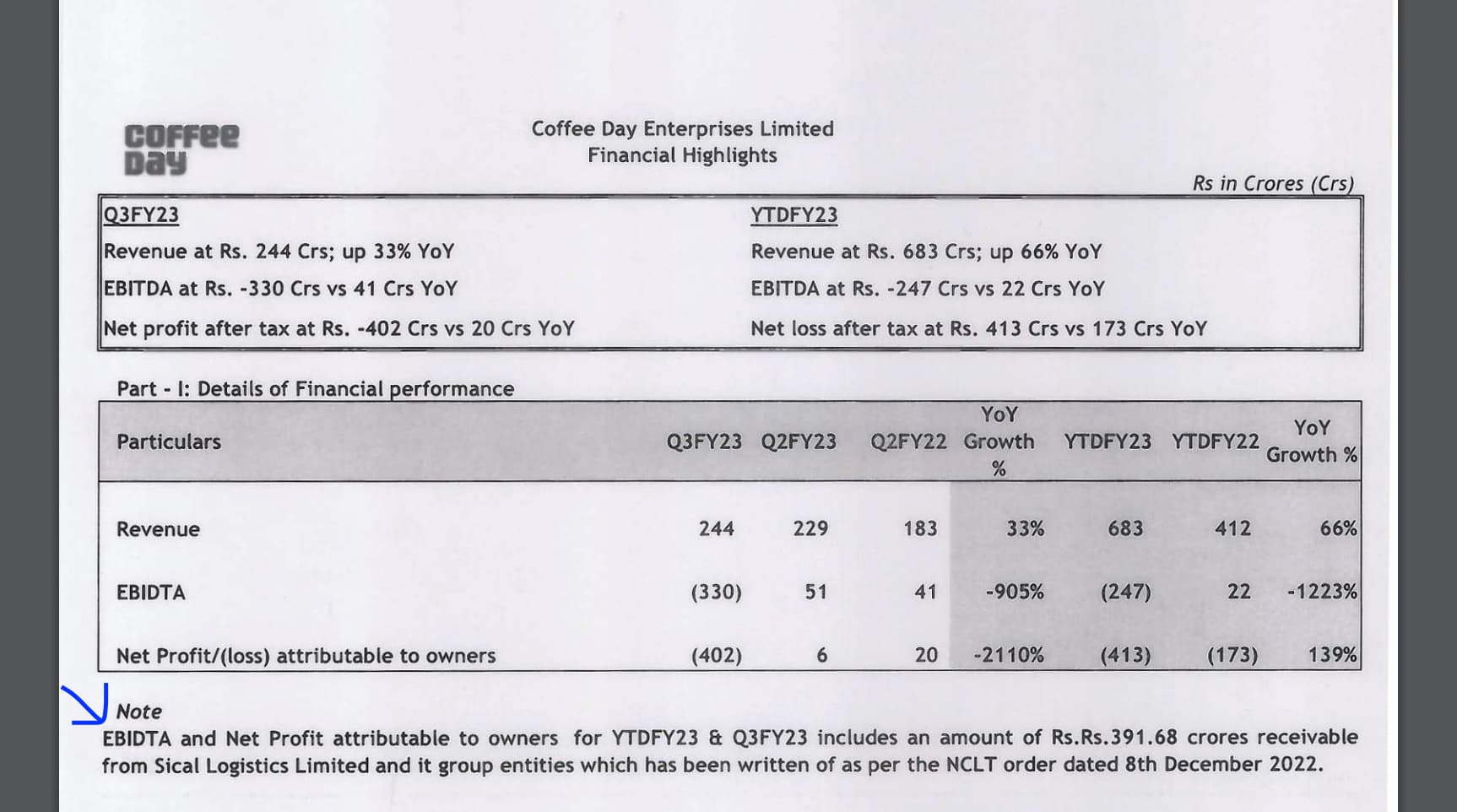

there is also a note in results:

EBIDTA and Net Profit attributable to owners for YTDFY23 & Q3FY23 includes an amount of Rs.Rs.391.68 crores receivable

from Sical Logistics Limited and its group entities which has been written off as per the NCLT order dated 8th December 2022.

Loss shown in this quarter is due to this adjustment?

I calculated BOOK value and it’s coming around 7rs and 2rs, there’s a loan of 2,288crore to MACEL and 1,055crore advance although these are shown as current assets but the amount is totally unrecoverable as stated by SEBI too, and the goodwill shown at 360 crore is shown as 2019 value as stated by auditors of the same coampny.

so if you make the loan adjustment, book value will come around 52rs

if you make adjustment for advances as well as goodwill (-50%) than book value will come around 2rs.

These all are tactics applied by companies to show the books as full of value but inside its something else.

3 Likes

Blackstone deal second tranche is awaited, 4 quarters in a row increase in topline, MACEL has assets though I agree recovery is anyone’s guess. The bet is on megatrend of coffee consumption, reputed name, increasing topline and bottom-line if we leave one time hit in the quarter. QSR commands 10x revenue as valuation and book value is hardly the yardstick here… Need to delve deeper to see value …

1 Like

Yes MACEL have assets but in last 3 years CCD have been able to recover only 100cr as of now and as stated by SEBI they don’t think CCD is really serious about recovering their money beacuse through MACEL a lot of fund was also transfered to VG Siddhartha and his family, There is really something bad cooking in the company i am saying this only after reading their Auditors Disclaimer in Annual Report, so this can be a high risk high reward bet, and maybe i am just assuming the worst case scenerio and i hope to be wrong.

If we go by Balance sheet as of September 22, book value will come around negative 4rs,

adjusting for Loan+ advances (to MACEL) + (50% GOODWILL AMOUNT)

2 Likes

NFRA Orders on Stat Auditors of Cafe Coffee Day Group…

Penalty on Firm 1 Crore,

Penalty on Partners 20 Lakh

Debarment of Firm 2 Years

Debarment of Partners 5 Year

2023041290.pdf (6.7 MB)

1 Like

CD overall top line crosses 300 crore first time in 12 quarters though operating revenue is flat, EBITDA of 113 crore, PAT of 39 Crore and turnaround remains a work in progress however results are encouraging and upside will be huge in times ahead. Stress is still there and expecting progress in that in view assets … Extract from reports List of susidiaries with significant invesment by parert overall, so underlying value of assets and net worth both good. Business while considering the

amount invested in the subsidiaries, the Management of the Company has considered the erstwhile shareholding pattern prior to dilution as the Management believes that the change in shareholding is temporary in nature and the shares pledged will be redeemed back by the Company (refer to Note 17 of the Statement). However, these shares have been transferred to such lenders before March 31, 2023. We have been informed that the lenders have not sold any of the shares invoked and consequently have not made any adjustments to the loan outstanding. Accordingly, the Management believes that it is not possible to attribute any sale value to the invoked shares https://www.bseindia.com/xml-data/corpfiling/AttachLive/3fad923c-2208-4819-8f41-2f7bcfdb4485.pdf

1 Like

Expecting debt issue to resolve in a few months with improving business and favourable political dispensation in the state. Waiting for AGM too for more clarity. Negen captial covers in newsletter last week why coffee is a great business

Welcome to the high-caffeine, high-reward world of coffee business – where the smell of success is often confused with freshly ground beans.

Coffee has captured the imagination of the world and now it is India’s turn, where the old generation love their Tea, but the younger GenZ firmly prefer their coffee.

So, what makes the business of Coffee so Lucrative?

1- The Gross Margins!

It takes barely 5 rupees to create a cup of Coffee and it gets marked up to 250-300 rupees.(Thats the Game, Set & Match - in a nutshell).

And the beauty of it is that, people are very much ready to pay 250-300 bucks for Coffee.‘Tea’ has a specific problem as a business prospect, that the sasti ‘Tapri wali Chai’ tastes WAY BETTER than any fancy cafe Chai.

2- Coffee is addictive.

Coffee drinkers tend to be regular customers, buying a cup of Coffee daily or multiple times in a day.(Case in point - We have put a XTC Coffee Machine from Dwija Foods in our office and I see that our people LOVE to drink this Coffee, regularly, sometimes 3-4 cups a day).

3- Coffee is scalable

Coffee is one product where people have many options, Espresso, Cappuccino, Americano, Fraps, Artisinal Coffees, Flavoured etc - all of which cost nothing to make and sell for very high prices.So, you got great margins, addicted customers and a great number of SKUs… all one needs to do is keep expanding and keep opening more such stores.

The Indian Angle

Coffee consumption in India is WAY BELOW the Global average, and this number is increasing consistently.On average, the per capital annual coffee consumption in India is extremely low at 100 grams.The Global average was 2 Kgs in comparison, in 2019.

Basically, India’s Coffee consumption trend is staring at multiple decades of growth ahead as it catches up to the Global average, as the GenZ rises.

Ps- Did you know that the Philippines consumes a staggering 3.6 Kgs of Coffee, the highest in Asia.(Despite having such high consumption, the Philippines demand is growing 14% annually).Vietnam is second at a consumption of 1.8 kgs.As mentioned above, India is at a paltry 100 grams, its ridiculous to be honest

1 Like

coffee maybe great does’nt mean anything

That morning coffee you swear by may not do what you think it does, neuroscience study finds

Revoke of 5 crore Rs worth shares by promoter today …baby steps hoping to see clear plan of debt resolution by AGM, its already late as per the precious AGM announcements…

1 Like

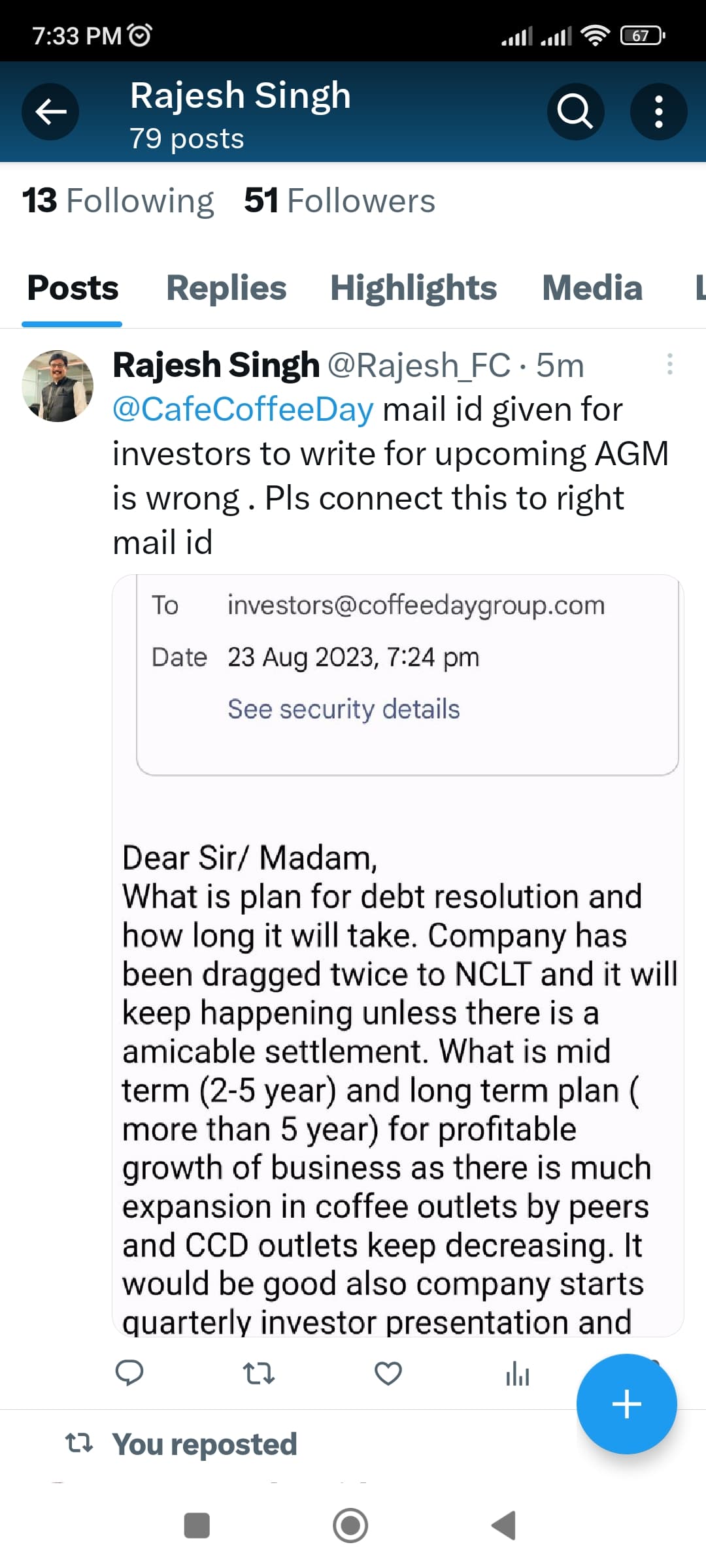

Mail id given for investors to AGM is wrong

Tweeted on CCD profile , they have been dragging feet on bank debt for long and if no clarity by AGM will sell

This will also be last investment in any stress assets

Growth companies with high ROCE mega trend are far better value creator with less stress

Will participate in AGM

2 Likes

1 Like

How does the company look to you after the recent developments?

In today’s AGM, they have made a promise that by next AGM Bank loan restructuring will happen and strategic investor will come in. They had made this comment last year too though

2 Likes

Yes its a very risky bet, burnt fingers of many, no institutional holding, and legacy issues of its own.

Plus promoter has been offloading shares too, but i reckon thats a distress sale:

-

Biggest problem for this company was and is Debt.

But over last 5-6 qtrs management has been consistently reducing the debt, and what i would consider unmanageable level of debt of i had to look at its BS couple of years ago, is i think come down to the levels, which could be managed by the company, if they get their act right. -

They have been selling their nom core assets to reduce debt.

-

Roc, and ROE is horrible but thats understandable as their problem is turning corner, and to deal worh debt.

-

Recently company has posted profits, and it has large chain of coffee shops, and is a well known brand in india.

-

There is a possibility that this may play oit as a revival story, if they get their act right, or ultimately could be a potential take over candidate.

I think they have a few litigation cases on going too.

Would love to learn from learned members about their prospective on the stock.

If they deal with their debt as they have over last 5-6 qtrs, and turn corner , i believe valuations are offering huge rewards vs the risk.

Opinions sought?

4 Likes

Completely agree with the narrative

All eyes on the recovery from MACEL

Your words depicts the current scenario very aptly.

Any investors at current level are like lone person in the middle of the sea without navigation, you never know when the bad tide will come and topple you down but you can’t stand still, keep the head down and row in the direction which you think is right hoping to reach the expected destination.

Disclosure: Started a tracking position recently.

1 Like

I sold it last month after two years…moved funds to eco recycling -megatrend of decade scalable business huge addressable market, trustworthy promoter already a multibagger and mega multibagger ahead in view of caoacity expansion , 10x topline guidance in 3 years.