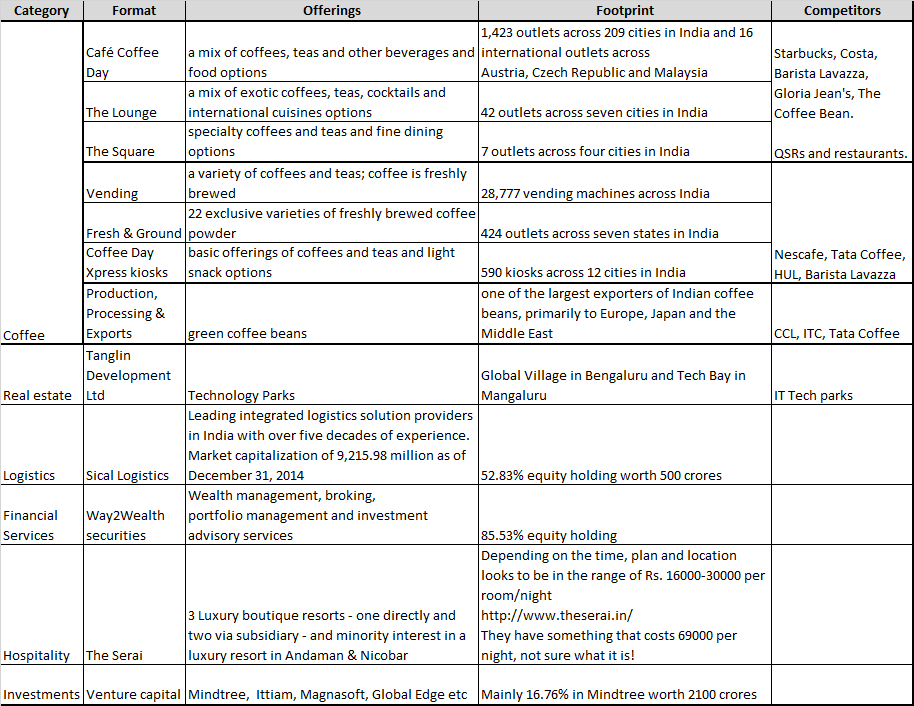

Café Coffee Day well known for its CCD outlets operates outlets since 1996. They are present in about 209 cities in India. They have a market share of about 46% and are the largest in terms of total number of chains. Café Coffee Day (CCD) has come out with an IPO for an amount of Rs 1150 crores with fresh issue of 35060976 shares valuing the company at ~ Rs 6756 crores approximately. Post issue Promoter Holding will stand at ~52.55%

Apart from this CCD owns about 16.6% stake in Mindtree. Their consolidated debt stands at 2762 crores.

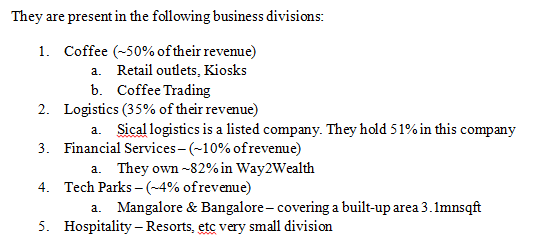

Logistics Business:

Sical Logistics Limited is a listed company and most of the financial information for this company is available in public forum. This company is available at a market cap of ~900 crores.

Techparks Business(Similar to NESCO):

They have 2 tech parks in Bangalore and Mangalore with a built-up area of 3.1mn square feet. This division does a top-line of around ~95-100 crores on a yearly basis. This is around 4% of their top-line.

Coffee Division:

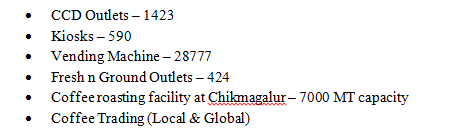

Coffee division #s:

The above table has the break-up of Coffee segmental revenues reported for this company. Of this 80% of the revenues are from retail outlets and these outlets operate at an EBITDA margin of ~20%. The other 20% of the revenues come from trading business which has an EBITDA margin of about ~2%.

So their retail coffee business is doing approximately 1000 crores/FY. Their retail coffee business is operating at an EBITDA of ~20% going by their EBITDA.

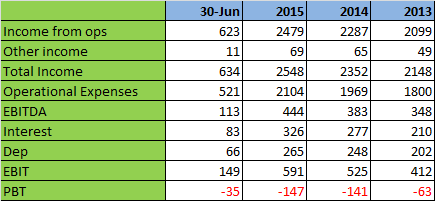

Consolidated Revenue from all divisions:

The company is planning to raise around Rs 1150 crores and the objective of this issue is to accomplish the following major heads:

1. Repay loan amount of about ~630 crores.

2. Set-up 215 new CCD outlets at a cost of 37lakhs/outlet – ~79 crores

3. Set-up 8000 new vending machines at a cost of 1.2lakhs/machine - ~97 crores

4. Set-up 105 new kiosks at a cost of 7.4lakhs/kiosk - ~7.77crores

5. Refurbishment of existing outlets – 60 crores

6. Setting up an additional 7000 MT coffee roasting plant capacity – 41 crores

Conservatively assigning Holding price discount for their investments in Sical Logistics & Mindtree:

- Sical’s market cap is 900 crores. They have a 50% stake. So at 1/6th (holding price discount), Sical investment can be valued at 80-90 crores.

- Mindtree’s market cap is 10,500 crores. They have a 16.6% stake. So at 1/6th (holding price discount), Mindtree investment can be valued at 338 crores.

- They have cash/cash equivalents of about 197 crores.

- Techpark & Financial services contributes to 4% & 10% respectively to their top-line. (150crores valuation on the optimistic side?)

At the issue price of 328/share the company is asking for a valuation of 6756 crores. Factoring in the above valuation for their other businesses, you roughly get the coffee business(retail + trading) at a market cap of 5815 crores. Add debt of about 2100 crores. The company’s enterprise value stands at 7900 crores.

Coffee retail business doing a top-line of about Rs 1000 crores, operating at 20% EBITDA has a market share of about 46%. Even if they manage to do 8-10% PAT margin (on the optimistic side), you get PAT of 80 crores(very optimistic #). Jubilant is valued at 100 PE. Most of the front end retail companies are valued at north of 70-80PE.

From here valuation of CCD is an individual’s call.

The big negatives here for me are:

1. Poor capital allocation – Their cash cow is their retail coffee business, they are pumping in money in to low RoE Techpark, Financial & Logistics business. They borrow to do this. Most of their borrowings stand at around 13-15%. So they borrow at this rate and invest in these low RoE business

2. No specific Niche – As an investor I am interested only in their 40% retail business. This IPO is looking to raise cash for their holding company ![]()

3. Their culture of funding growth(??) through Debt.

Thanks,

Ravi S