Catching the bottom is a more predictable event than falling off the top.

I say it’s more about technical analysis than fundamental analysis. I personally use the 200 EMA on a monthly chart to see a greater picture.

The question comes, when will the price will reach 200EMA? In other words, when will the next crash happen?

There are people who waited since 2011-12 to see the price come to a reasonable level. And all they got was, that they missed one of the best bull runs in the past decade.

The sincere advice would be to keep investing small chunks of your income in the market, but keep yourself hydrated with cash in case of a market crash.

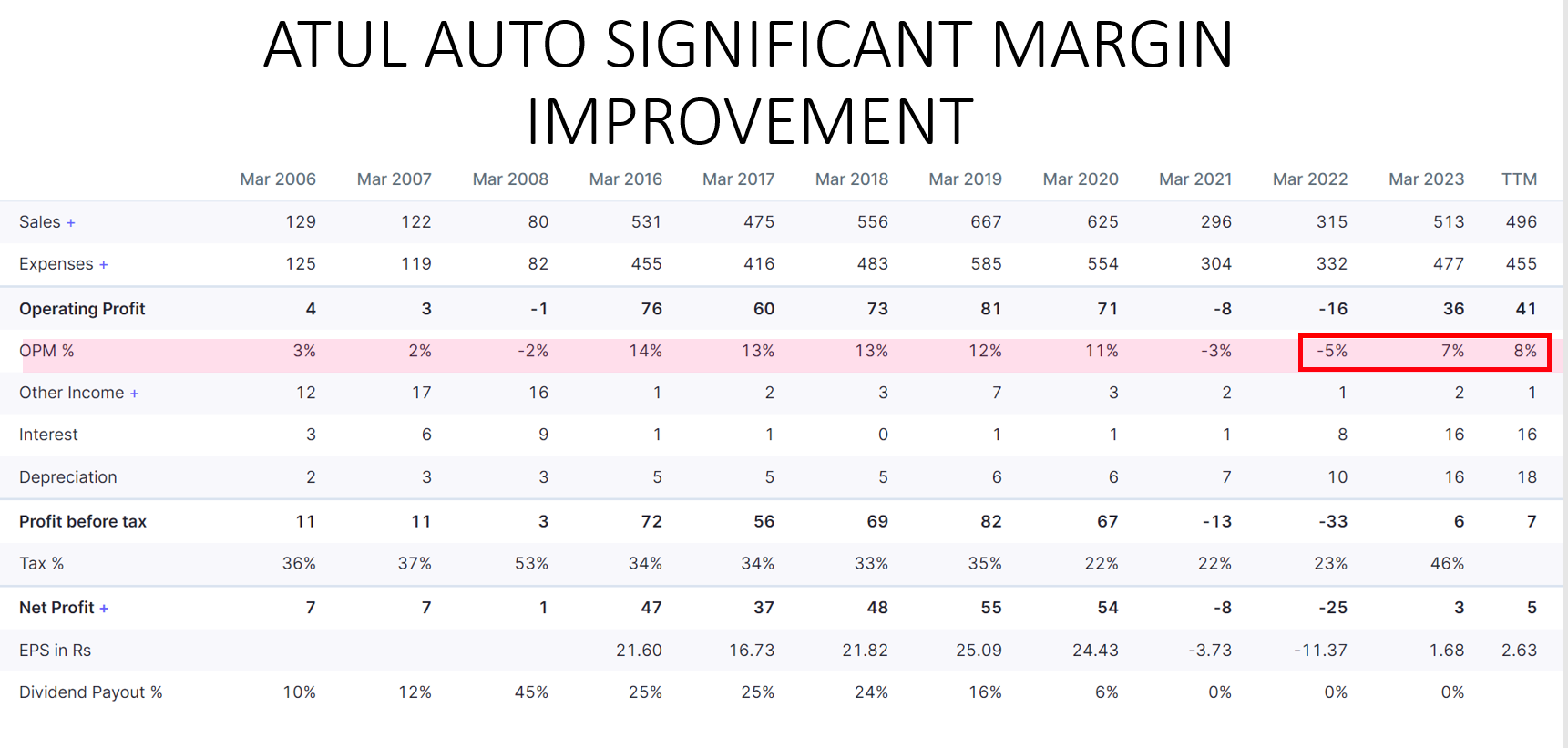

I think a lot of people made serious money from 2013-17/18 bull market. 2012-13was really a pessimistic time. Most of the companies had all time low margins in FY 13. You can check that.

An article I came across about high hopes from shrimp industry due to consumption from China. India could be a beneficiary. You can download the article from the link below shrimp.pdf (5.0 MB)

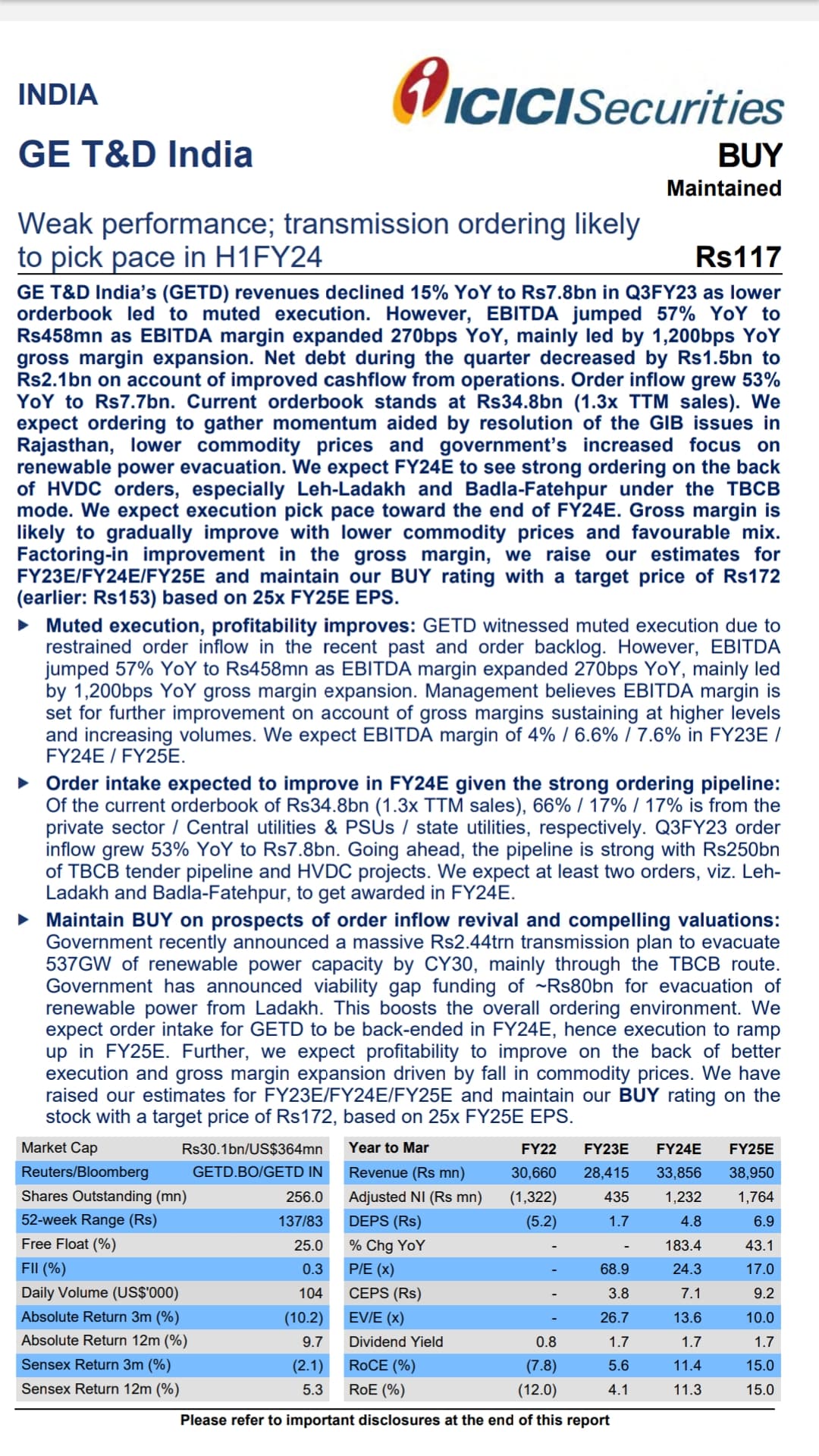

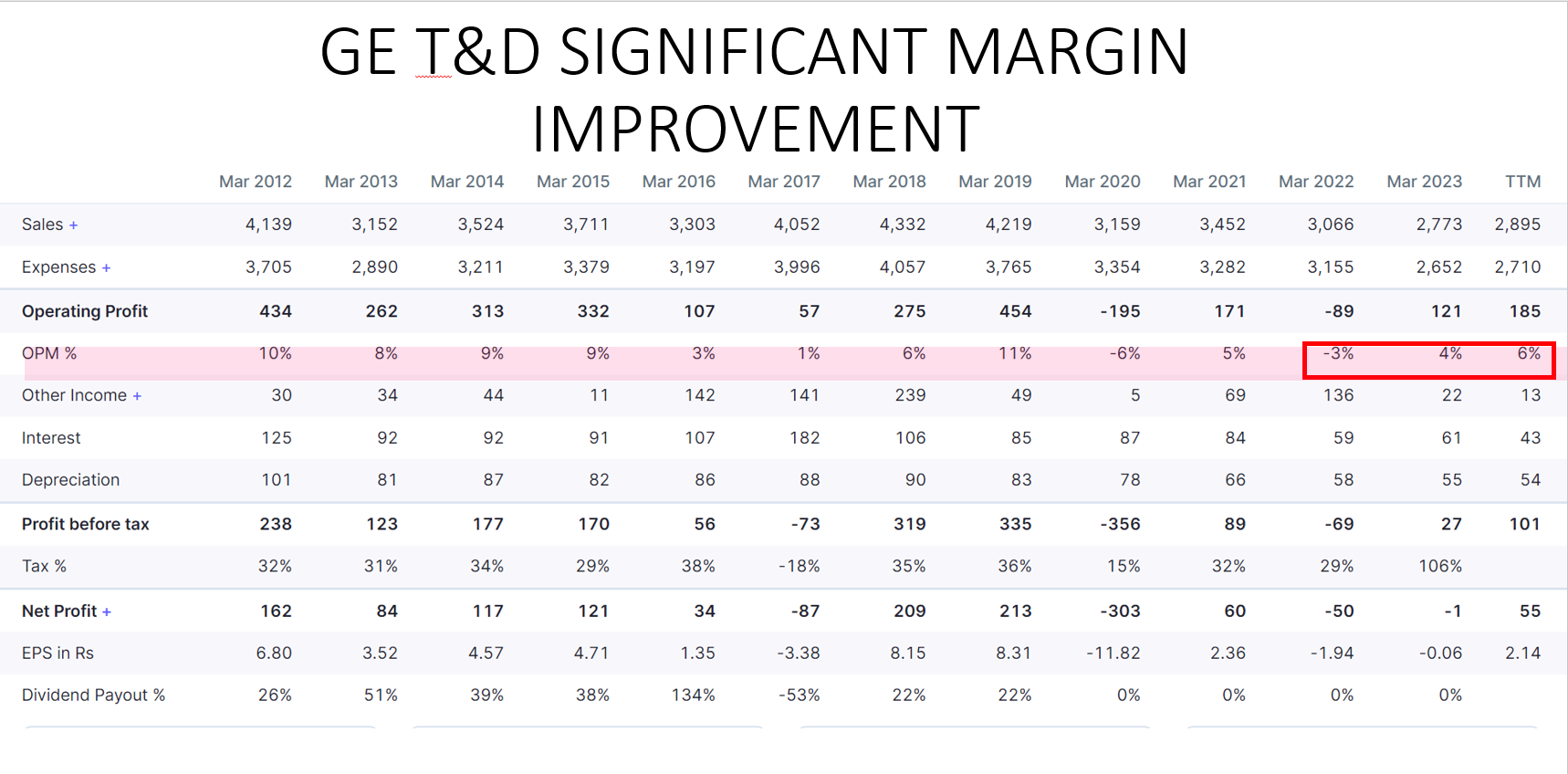

GE T &D, also one of the company beaten down in last few years. I could not find a separate thread for this company. But I believe it fits well in this thread. Brokerage reprort from ICICI securities. Will be coming with a detailed writeup soon.

Full report in the link below. Ge T and D brokerage report ICICI sec.pdf (302.6 KB)

balaji amines seems to be a good candidate for bottoming out.

the demand from the pharma and api side seems to be picking up (according to the latest concall).

new expansions are going to come online starting from this year for the next 2-3 years, the capacities coming up this year are better margin compared to the current product profile.

balaji specialty, the subsidiary has significantly higher margins than balaji amines, planning to introduce new products (first time products in india).

technically seems to have formed a bottom, waiting for further technical proof.

I started this post last year in December. So its a good idea to take note of the companies that I posted about since then and how they have done. Is the pessimism still prevailing and was it a good idea to buy them at these times. Disclosure: I personally may have allocation in all the companies I talk about.

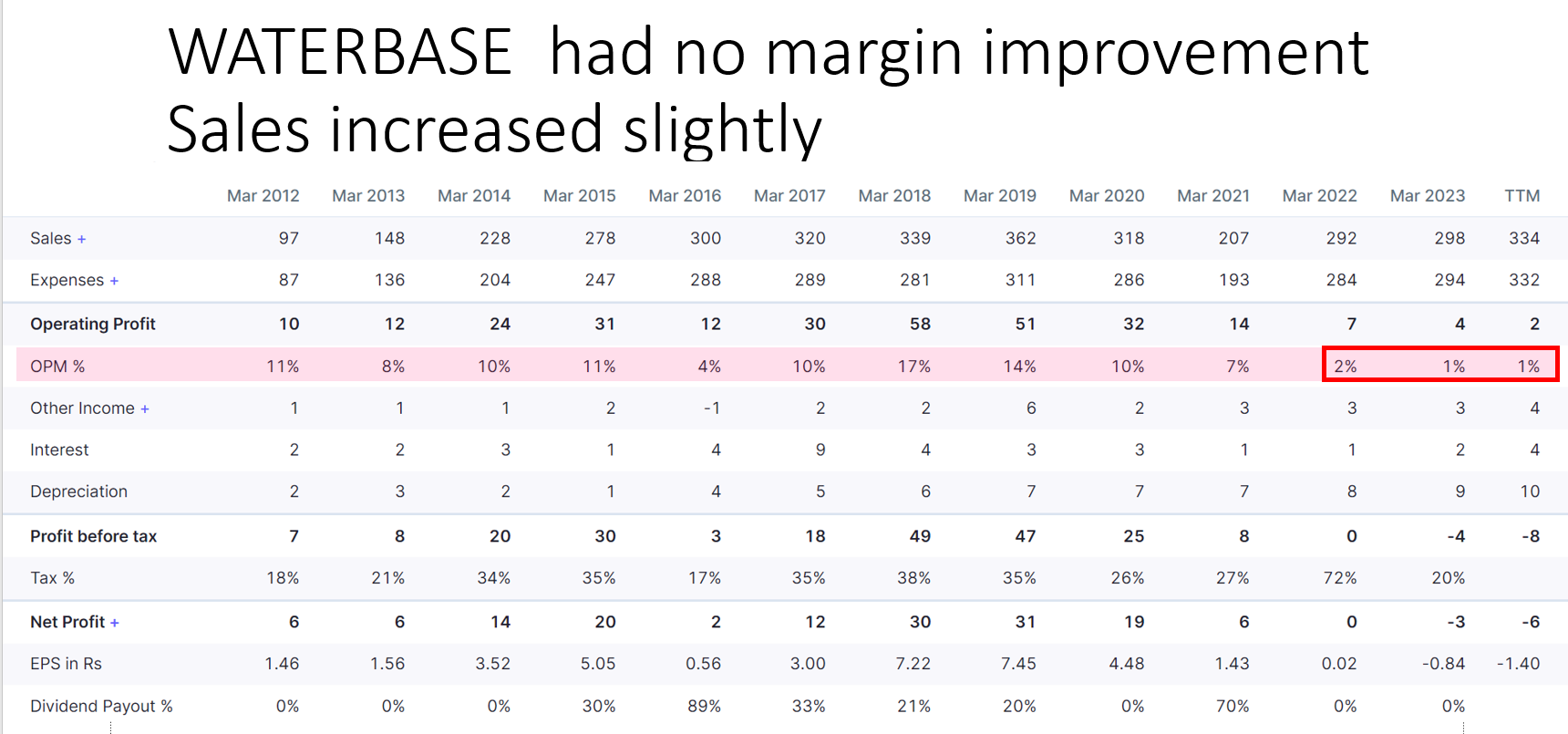

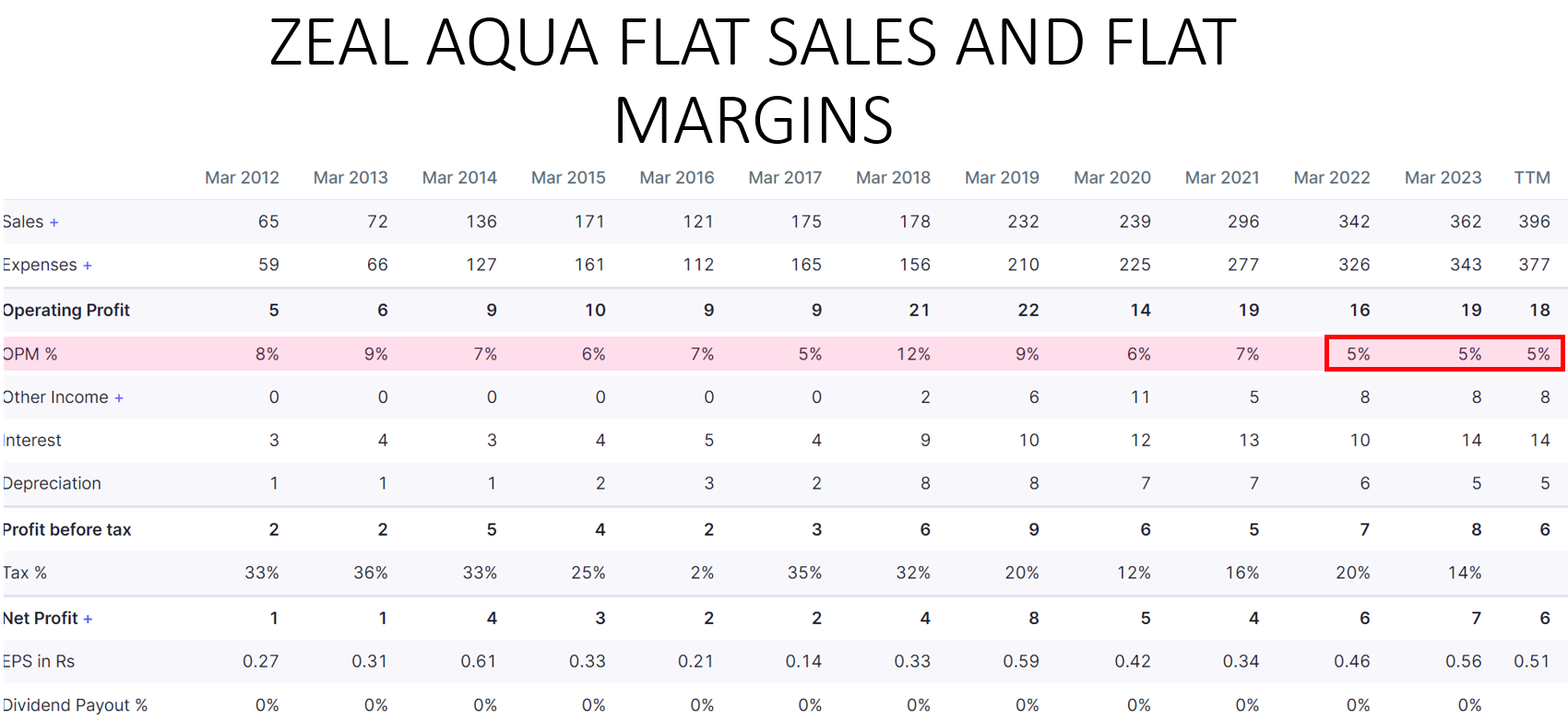

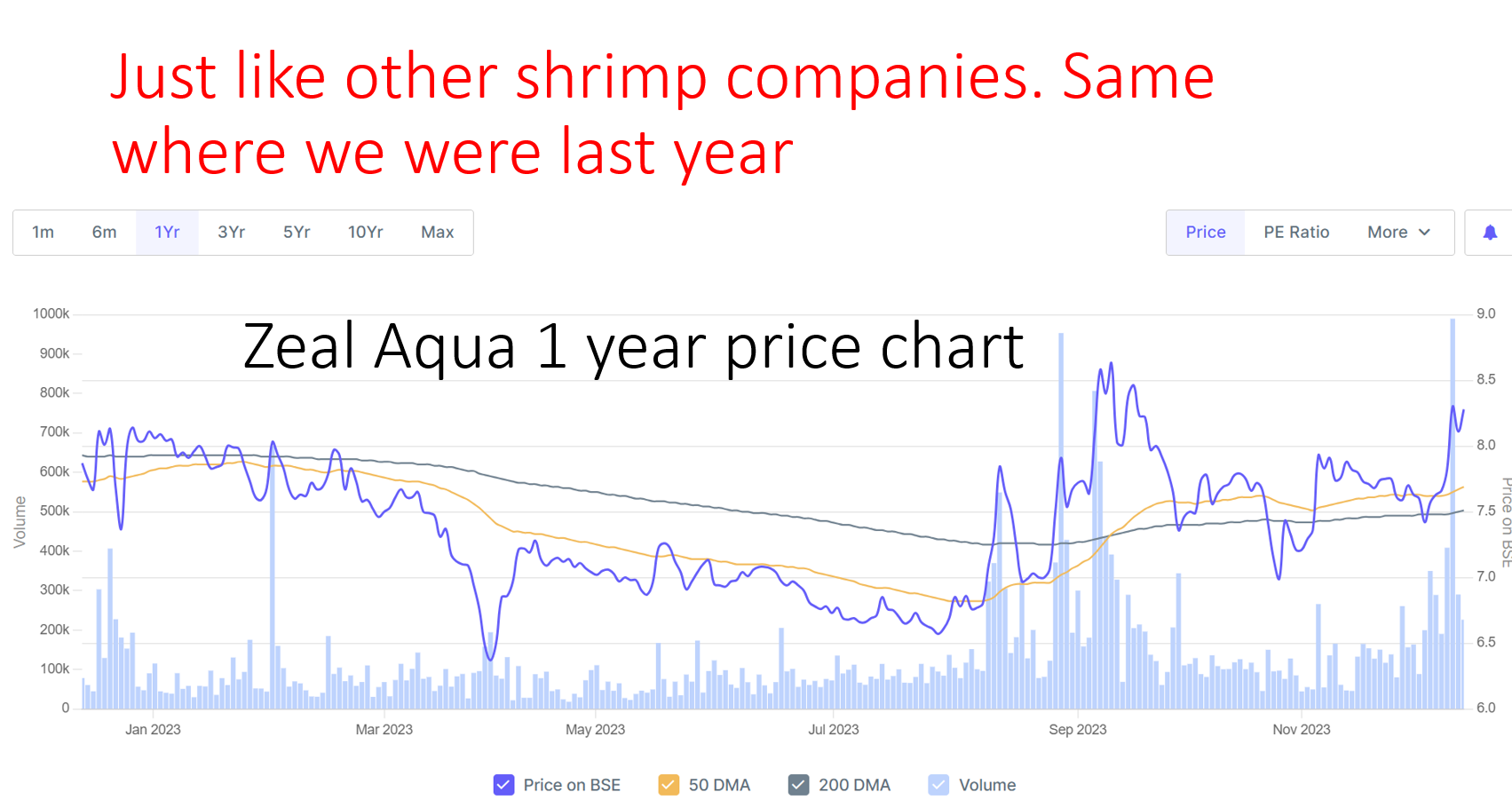

So lets start with the HOPE sector of most investors that is Shrimp.

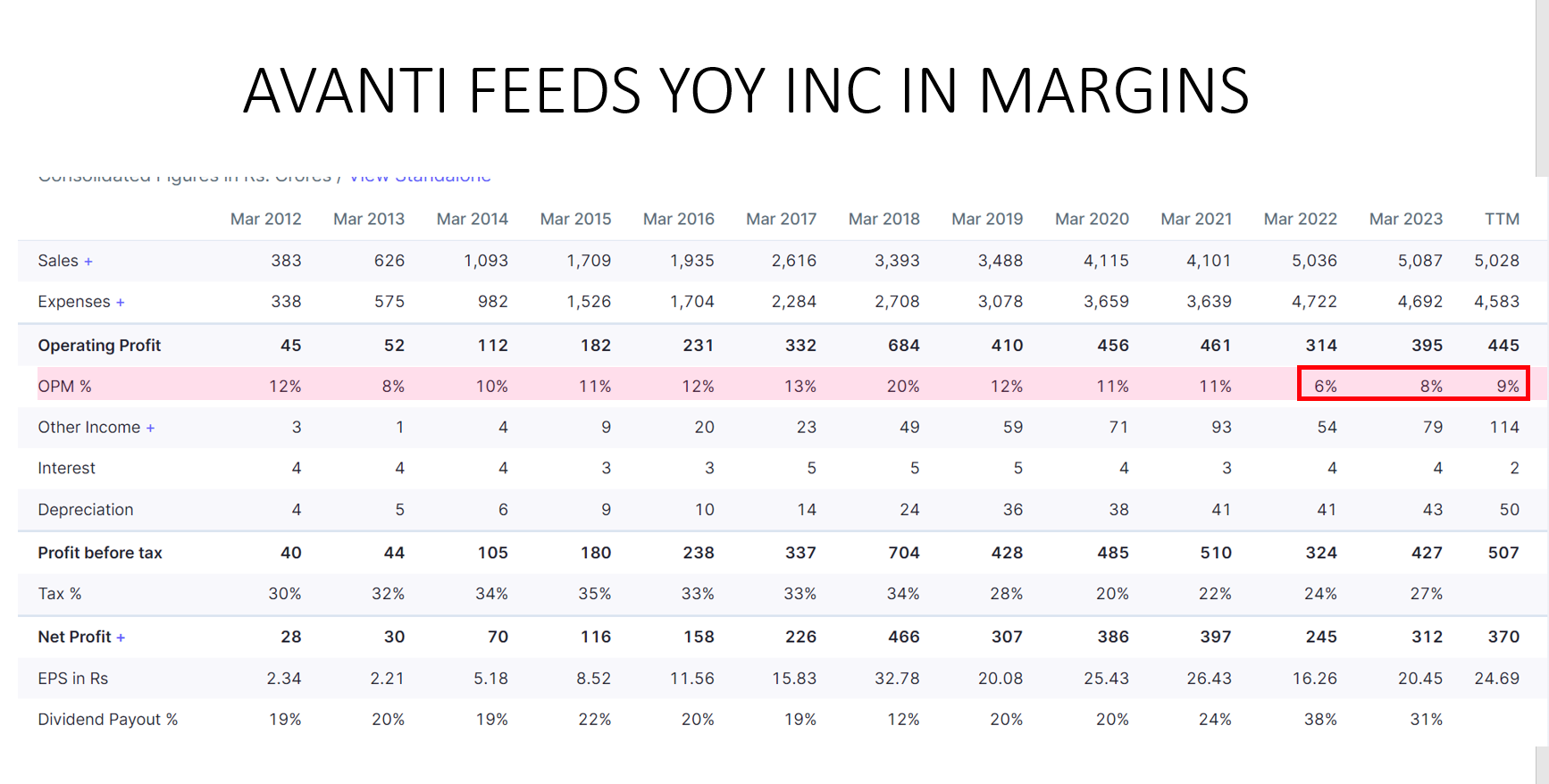

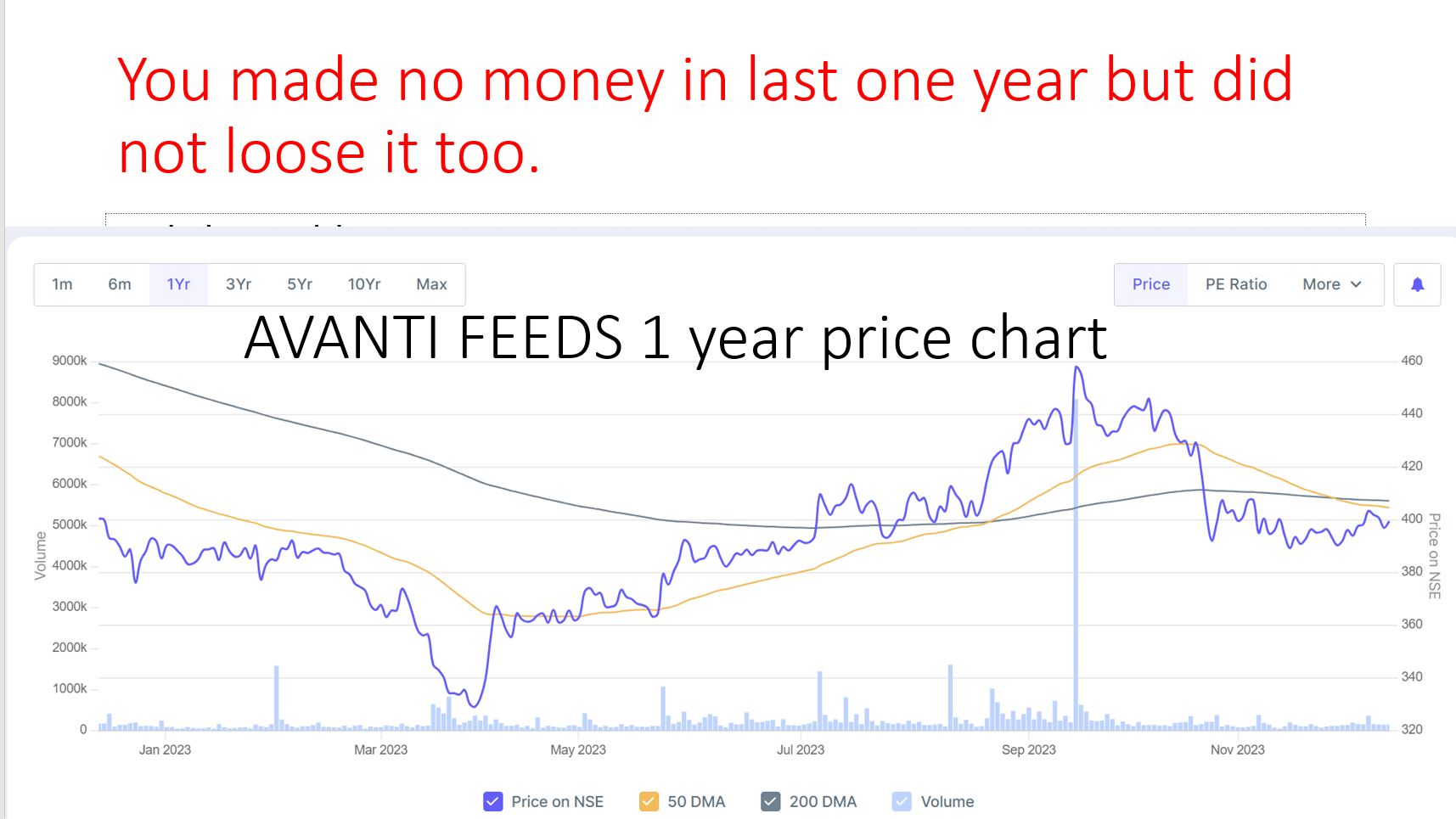

Avanti Margins have improved however sales are similar. @harsh.beria93 has done some amazing work on Shrimp industry. Other than reading up on google and other sites. I definitely look forward to read up on his work.

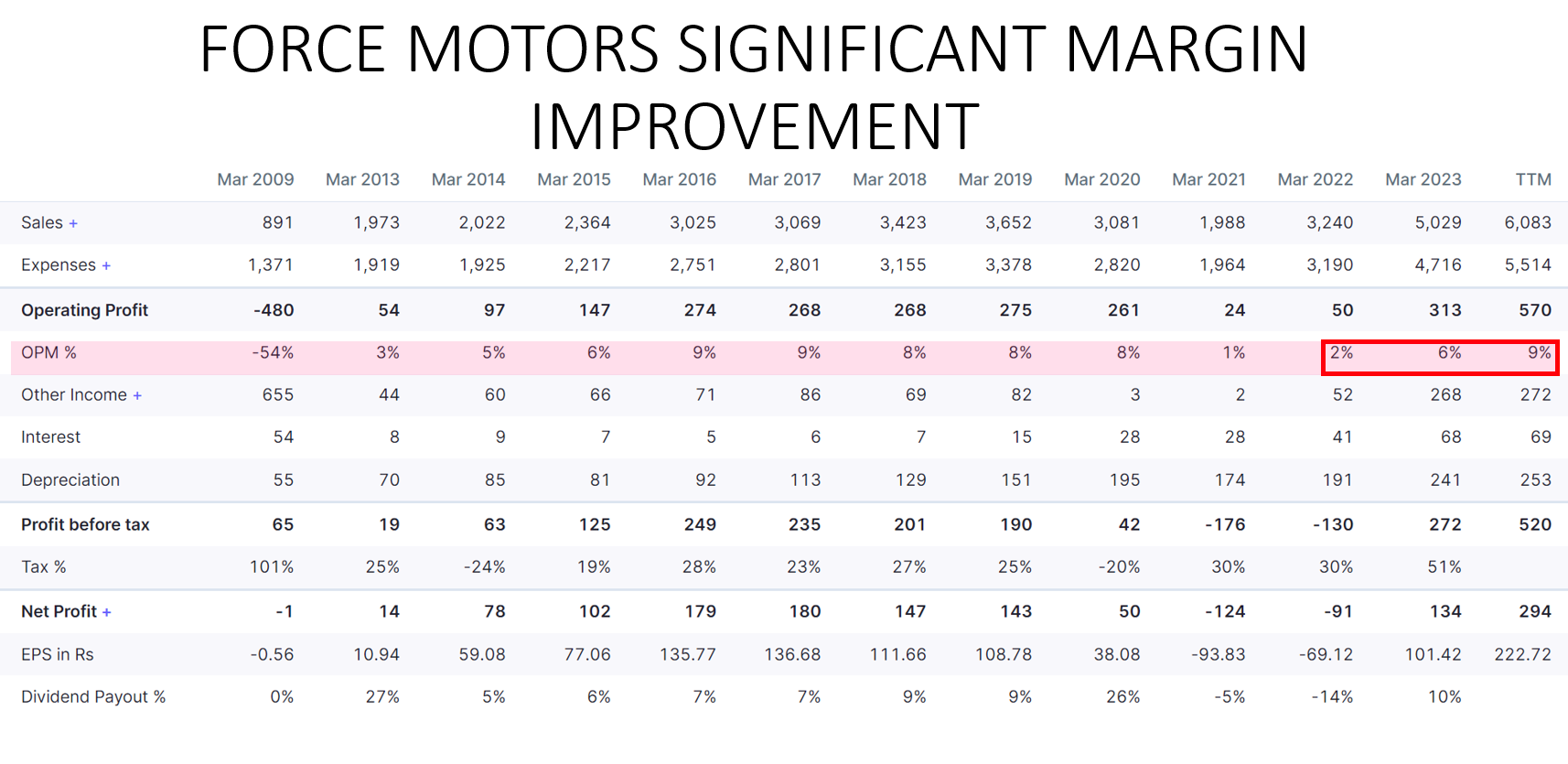

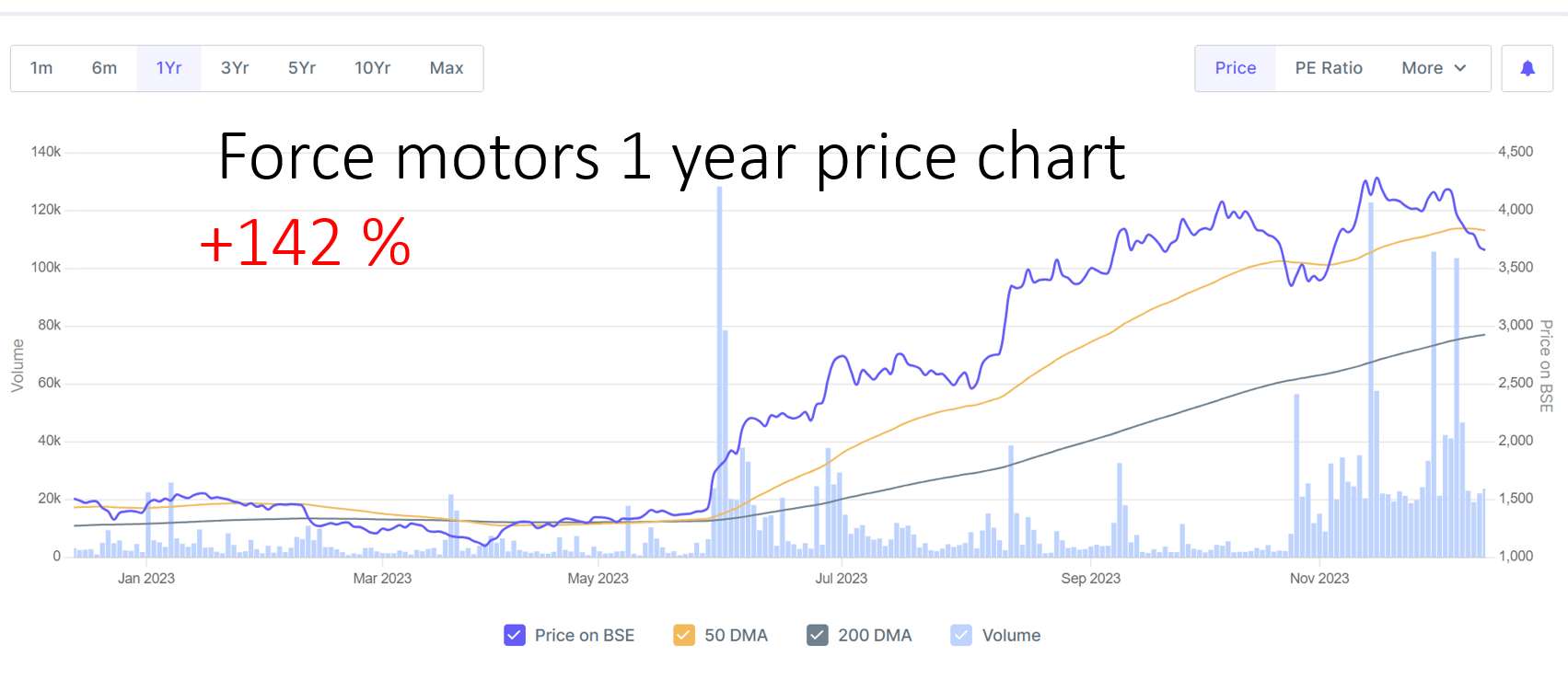

Next was Force motors. @Investor_Mohit has also done some work on this one.

Sales have also improved. I expect this company to do well in coming year lets see.

Sales have also improved, I expect things to get better and operating leverage to play. If I remember their MD said that right now their capacity utilisation is 25%. And the Anchor was shocked. If things go well this could be a game changer.

I also wrote at length about National Peroxide. You can read it on the company specific post , and the company did extremely well and benefitted from drop in Natural Gas prices. I have sold my Natperox Shares post record date to be eligible for NPL Chemicals stock. I am waiting for it to list.

Obviously there is a lot more subjective and objective work that goes in researching and just low OPM is not the recipe, but its reversion to mean is definitely one of it. There are some sectors and stocks going through pessimism. I will probably post about them soon. Other than that I am extremely grateful to all the contributors at this platform. Cheers!

Agrochemical companies and Bulk chemical companies are the only space where i am finding pessimism… But given the challenging industry situation, it may very well be justified

As per Paris agreement GOI has not authorised any new coal driven power setup for a long time. The growth in coal based power is purely by stretching on existing capacities which can have limitations. Adani power has been acquiring old non efficient plants and trying to get them up and running as new coal based plants are not sanctioned anymore.

As for textile there is significant chance of disruption due to robotic/ automation in developed world. They are building robotic sewing machines that work 24x365 and push out huge quantities of apparels. The low cost apparel manufacturing option may soon end.

“To ensure completion of projects, New Delhi has begun a review of 38 coal generation plants whose construction has been held up for years, moving to resolve issues over equipment and land acquisition delays, the two officials said.”

Nevertheless you are right finally country interest will be above any agreement.

Has been fraught with challenges in the last couple of years which is reflected in the price and valuation (P/B)…

1/ Insider trading case in early 2022 against promoter’s son (Udit Todi)

2/ Surge in raw material price (cotton)

3/ IT raid in late 2023

4/ The two brothers at the helm (Ashok and Pradeep Todi) not getting along

Now,

Udit Todi has been given a clean chit in the insider trading case

Cotton price has cooled off

Per the grapevine, brothers Ashok and Pradeep have divided the empire (split by brands)

IT raid is the only big known unknown

Looks like the stock price has bottomed out and any positive news will help. Will welcome opposing views

")