Good day to everyone at VP. This thread is inspired by the deep value style of investing, in which the idea is to buy at pessimism, look at companies that are overlooked, currently out of favor and are making new lows. A lot about this was covered by Mr @ndharmawat on youtube CFA society India “Buying the pessimism”. A wonderful presentation. This thought process has also been what Howard Marks as always been talking about in his books and Memos as well, primarily - “Mastering the market cycle”.

Even @jitenp has talked many times in his framework that it looks like best time to buy companies were when their operating profit margins were all of a sudden negative or much below the mean.

Lets go ahead.

Two cents on bottom:

- The bottom is made when the point of maximum pessimism is reached

- The news headlines are bad

- A stock may consolidate near bottom for a long time.

- Not everything that goes down, comes back up, though it happens most of the times (Reversion to mean)

- It is impossible to catch the exact bottom

So it is imperative that a smart investor must be attentive to cycles, and be continuosly look at -out of favor and overlooked opportunities. A patient behavior goes a long way in such type of investing.

I will now share few of the sectors/ and few companies where the pendulum has swung the opposite way, where I feel next reversion to mean opportunities may rise.

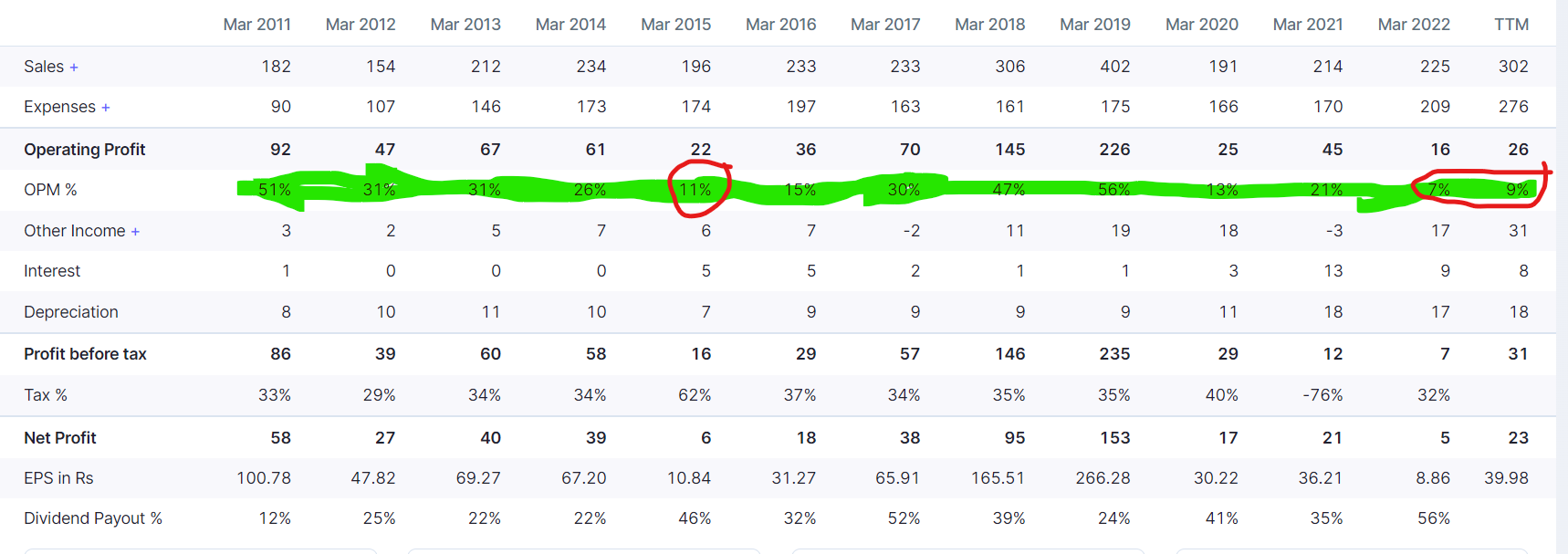

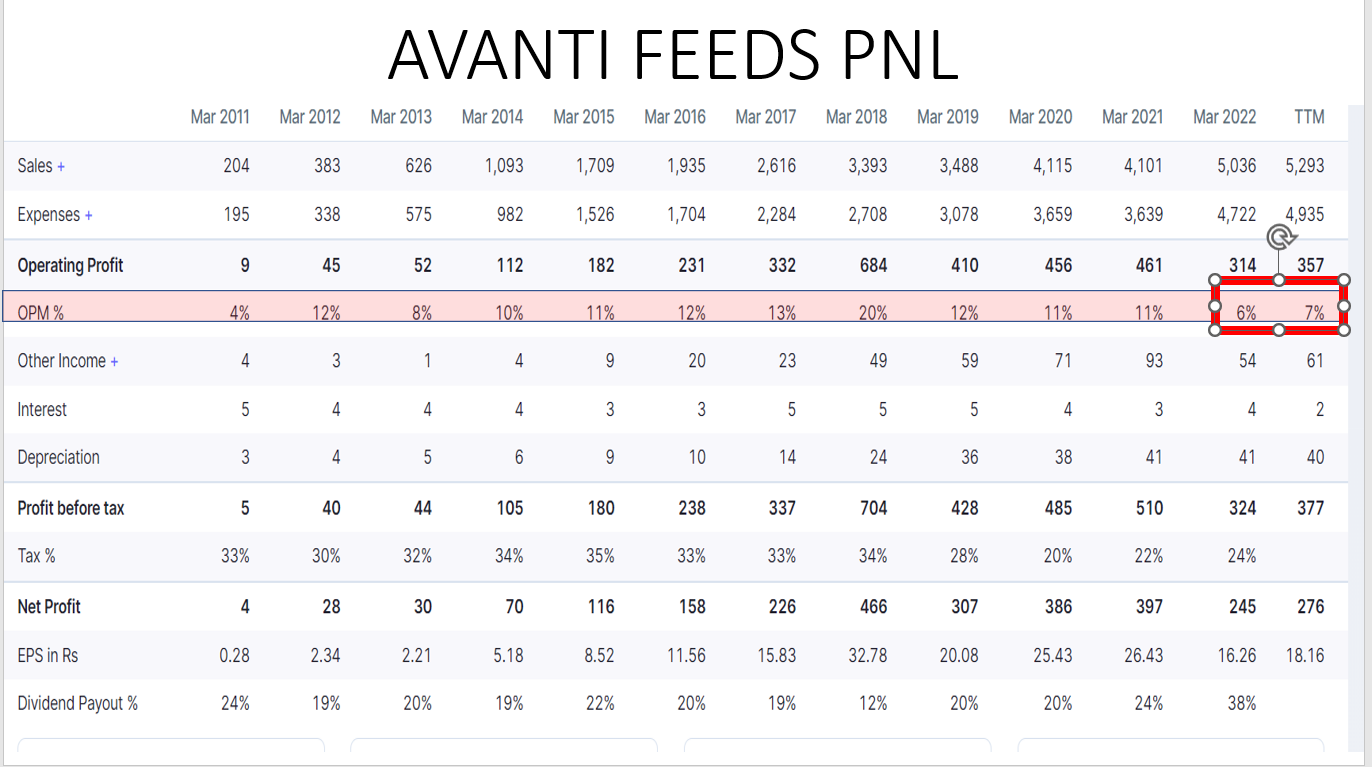

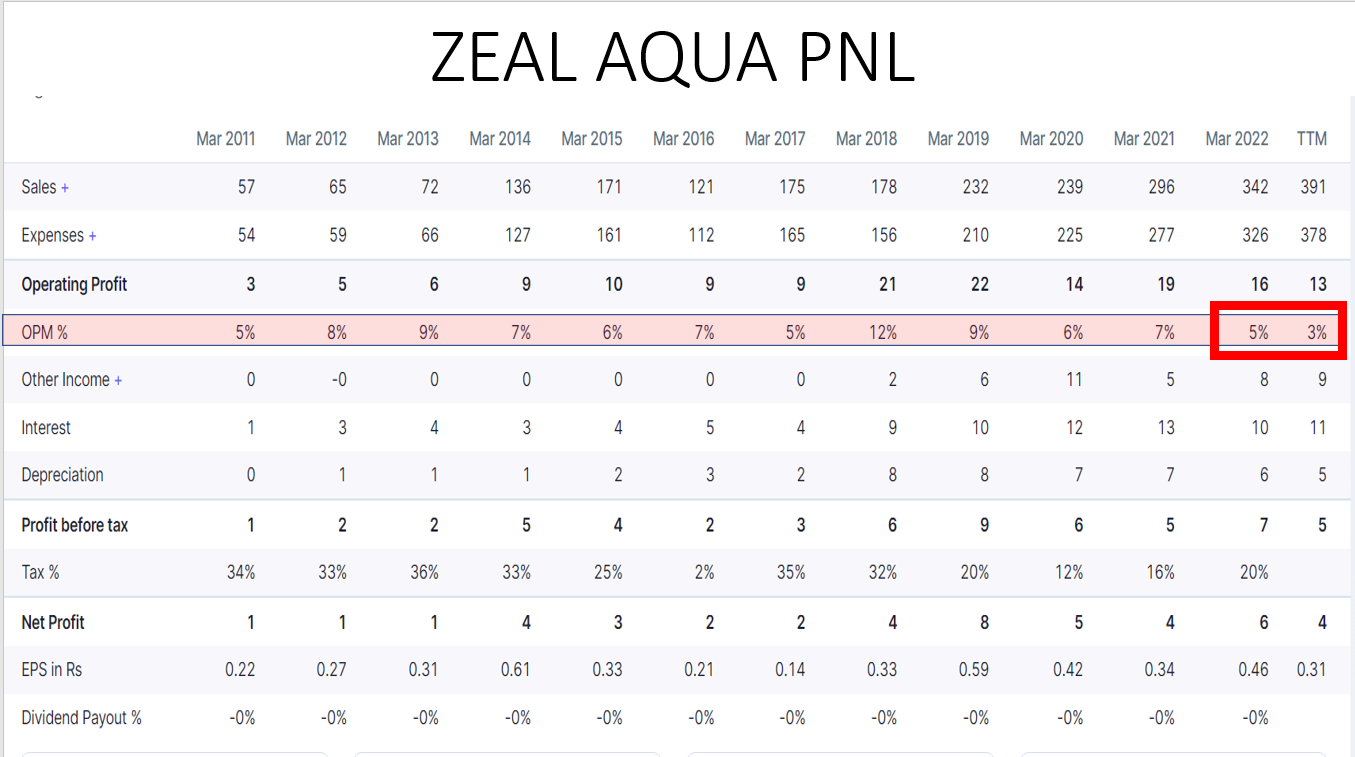

- Shrimp Industry.

Shrimp industry is supposed to be the next big thing in terms of export for our country. The primary raw materials are Soya and wheat. After going through their best times from (2013-2018), things were reverting to mean from excessive optimism. Some of the companies such as Avanti, Waterbase became darlings of the market. When things were getting normal- the covid hit. The demand went south. Inventory kept piling. Many debt laiden players globally shut their shop. Post covid as demand started to come back, inflation prices soared phenomenally leading to further pain. Shrimp indusry is one such industry which started to go south post 2018 and has not recovered. Today the state is such that some of the companies in trailing twelve months have shown weakest margins, when compared to their long term as well as short term medians. Few companies where I am looking are Avanti feed, Waterbase, Coastal Corp, Apex Frozen

I will be writing on other sectors and companies, following this thread. Please add if anyone has other things to look at or comment on whatever has been said.

Disclosure: Invested in waterbase