The objective is to arrive at a more holistic framework for evaluating businesses with “Emerging Moats”. Businesses not fully-discovered by the market yet, or discovered, but not-fully-valued yet, businesses that we think has the potential to scale majorly from here. The framework attempted is NOT for Mature businesses.

Those of us who got our hands dirty the first time round around Business Quality (BQ) evaluation seem naturally enthused at another formal go at it. We know the IMPACT it had on prodding us into looking/investigating a business - at a far far more granular level.

For the benefit of new VP Members and those who might have missed paying attention earlier to our BQ/MQ efforts, here are quick reference points. Also for anyone interested, but not familiar and starting from ground zero, going through the threads, responses and counter-responses will be very instructive I can assure you.

- Business Quality Value Drivers - Apr 2012

- Business Quality Value Chain - Oct 2014

- Business Quality Insights - Mar 2015

Those who want to jump to the meat of earlier work straightway, here it is

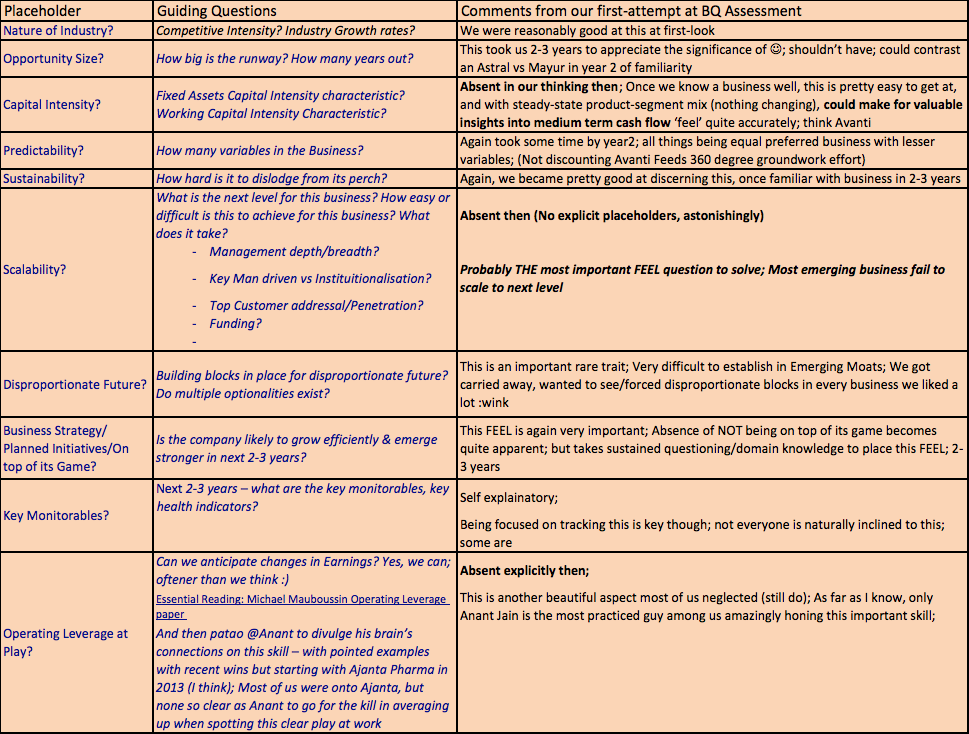

VP-Business-Quality-Insights.pdf

We covered some six businesses (Astral, Mayur, Ajanta, Shilpa Medicare, Kitex, Avanti Feeds) from the VP Portfolio - as you might have noticed, some of them we had already held for almost 4-5 years, had multiple engagements with through extensive Management Q&As, seen them (so to say) walk the talk. Yet when it came to filling up the BQ Template we came up with, it proved very very tough ![]() , believe me. The mind just wasn’t trained to think the BQ way!!

, believe me. The mind just wasn’t trained to think the BQ way!!

The first valid objection was that these had the major benefit of hindsight, there was probably inherent bias (which it had plenty, now we know). We should showcase an exercise for a new business we come across, which we did follow-up with.

MPS Business Quality - Nov 2015 (link to a pretty lengthy video, almost 2 hours I think).

We fell flat again. Got carried away (most probably due a suave Management) and majorly ignored SCALABILITY of a niche player even as we were convinced of a durable competitive advantage.

Till 2015 (when we finished the first published draft), I had only seen businesses going in one direction - up, up & up ![]() . And then we started seeing a Mayur faltering, and then an Ajanta, and an Alembic. That Reversal to the Mean is a Law, that even seemingly flourishing businesses succumb (something invariably changes in industry, regulations, technology, competitive dynamics, and the like) became emphatically clear to me.

. And then we started seeing a Mayur faltering, and then an Ajanta, and an Alembic. That Reversal to the Mean is a Law, that even seemingly flourishing businesses succumb (something invariably changes in industry, regulations, technology, competitive dynamics, and the like) became emphatically clear to me.

So then, earnest search started for businesses that can defy the Reversal to the Mean LAW (@deepinsight calls these the rarest of the rare). We then came up with this

Self-Reinforcing-Business-Models-Scrutiny-Framework.pdf - June 2016

Self-Reinforcing Business Model discussion

Bajaj Finance was the business presented.

This time the objection was that this was probably too cumbersome, too heavy. If I remember correctly, we couldn’t get too many enthused to carry out an equally detailed exercise on other businesses they liked/admired. Then it struck me that perhaps we needed to go back to basics - simplify - how do I explain/elucidate on the basic business model at the core of a business we like, and then build up from there to BQ,and more refined exercises.

In a moment of inspiration, before a CCL Products Management Q&A, I came up with this, which I thought was really simple to create - for anyone who thinks he knows a business well. All one had to do was first describe what you know about the Market place - customers, how you reach the Customer, who are the Players. And then you describe the other half - what you know about the Product - product positioning, production, technology; and that was it!

Business Model Canvas

And again there were objections ![]() Ha ha

Ha ha

It’s a complex exercise we had undertaken. And despite some crucial insights gained in all these off-and-on exercises right from 2012 as you can see, there are huge gaps (holes even) in our grasp and analysis, we were too liberal with assigning the final verdict (A, A+ and normalised valuation ranges) as we now know - again with perfect hindsight ![]()

However, THIS IS a very very valuable pursuit. If we make bold to participate, persevere, and see through this exercise - our understanding of businesses will mature significantly. Yes, we need to bring a lot of sustained focus - improve on the template, plug the gaping holes, consult available business model literature, pick the brains of colleagues/Mentors we admire, exemplify through businesses we like…and yes, I know, SIMPLIFY!!

An astute observer - some senior VP Member - can’t remember who right now - had a terse comment to offer. Donald, simplicity, or the ability to abstract, comes only after a lot of hard detailed work. Persist with the hard work!

Our job is cut out. I am excited to embark on this journey! Are you?