how has this been historically with the well established peers?

I have been tracking this business for quite sometime and here is my thought -

While the overall strategy of expanding and operating this business looks fine to me as already articulated by @akhilgulecha the moot question still is how different is BK from McDonald’s and what prevents McDonald’s from taking away BK’s market share. At the end of the day, people don’t care for the brand name BK as long as one gets similar quality products at lower prices.

I happen to accidentally visit and compare price and offerings of McDonald’s with BK and found McDonald’s offerings (similar products) priced lower to that of BK. Rather than comparing different QSRs a detailed comparison of McDonald’s with BK is more of an apple to apple comparison here. It should not be difficult for McDonald’s with its brand and distribution reach to take away BK’s market share in the coming qtrs/years. The recent results of BK seems to indicate a slowdown in SSSG which reaffirms my thinking.

1 Like

What about the taste differences even if the items are the same? People who like BK’s taste will go there, and not to McD, even if McD prices its items lower than BK, and offers same quality. I cannot recall the taste difference between Coke and Pepsi, but they have been in business for decades. So can an argument exist for all these different QSR businesses to coexist and grow?

No investment in any QSR, interested in the broad theme.

2 Likes

A popular investor vineet Bhatia is heavily invested in BK…and he shared how company is working to give unique taste to customers.

3 Likes

Hey Rohit.

Any source for this. Thanks ![]()

1 Like

Itna bhi popular nahi hu sir, but my investment thesis has been widely published in F2F

4 Likes

Good to see you here sir! I saw your F2F episode and it was great to know your experience and the insights you shared. Alok Industries case was amazing!!

2 Likes

In terms of the menu, BK has mutton which is not on KFC/McD menus. BK has created a menu at the intersection of McD and KFC - Burgers, Wraps, Nuggets, and Chicken Wings including Boneless and Grilled Chicken. (Plus a little nudge into Taco Bell territory with Veg/Chicken Tacos)

The domination of non-veg items in the menu is bound to give BK a higher per-order value and they should in fact make sure they are priced higher than McD on most items to have the premium factor, other than some value offerings which they can retain to compete for the lower-order value customers.

On the question of people preferring one brand over the other, I feel like each brand will develop its loyal customers and over time price will not be such a big factor, just as McDonald’s offerings have gone far beyond the low-price value items and into McCafe + Gourmet burgers category.

While a smaller point, I also feel McDonald’s success so far could become a positive for other brands as just being located in the same food courts/malls could see other brands gain from McD’s waiting time

3 Likes

For any QSR, there are fixed costs at the corporate level (rent, office salaries, sales & promotions, app development) as well as other initial costs that do not rise linearly with rise in revenues (initial training costs, new equipment, one time fee for opening up new store, etc). Hence, operating leverage should play out after a certain scale has been reached. Jubilant Foodworks is a good example of that in India. Dominos India EBIDTA grew much faster than their revenue growth in the past decade. The overall numbers are skewed because of their investments in Sri Lanka and in Dunkin Donuts.

You can look at Burger King itself. In the latest quarter, a 20% increase in revenues has resulted in a 34% increase in Restaurant level EBIDTA and a 48% increase in overall EBIDTA. You can see that Corporate and General expenses have reduced from 6.3% of sales in Q3 FY23 to 5.4% of sales in Q3 FY24 as Sales have increased. This is operating leverage at play.

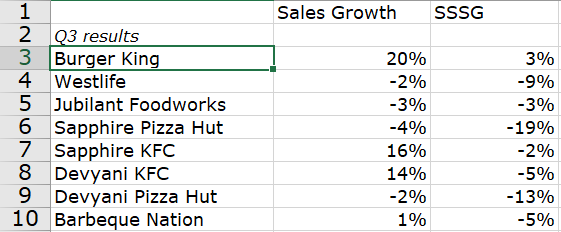

@iyeron I don’t think I agree with your hypothesis. McDonalds is definitely a stronger brand but I don’t think selling cheaper products is the only way to take market share. There are multiple factors which determine where people go to eat and price is just one of them. Product quality, Variety of products, ambience, location, marketing, deals and promotions, brand loyalty, etc are some of the other factors that also influence decision making. If it was so easy for McDonalds to take away BKs market share, why do the numbers indicate otherwise so far? BK has grown from 0 to almost 1600 cr (FY24) of sales in less than a decade. Even in the latest quarter, BK has shown positive SSSG as opposed to negative growth shown by Westlife.

Q3 update -

Q3 numbers look great for RBA. They grew the highest out of all the QSR players, with the only one to achieve positive same store sales growth. McDonalds, on all fronts has underperformed when compared to BK. The Pizza brands are really struggling, with KFC showing good positive growth. For the kind of growth most QSR players have shown, they trade at really absurd valuations.

RBA has a much smaller base, trades at lower valuations and has significantly much larger headroom for growth (they have pan India rights). I am optimistic about its growth prospects in India. Their Indonesia business did see a slight slowdown, but considering it is a new market for them we can give the management some time to show execution. Indonesia will need to be monitored closely to make sense of the prospects there.

13 Likes

A quick look at the numbers (as per screener) over the last 2 years (FY21 to FY23) for the two indicate otherwise.

For very similar top line: -

| Westlife Foodworld | Restaurant Brands Asia | |

|---|---|---|

| Sales CAGR | 52% | 43% |

| OPM | Expanded from 6% to 13% to 17% | Expanded from 2% to 6% & dropped to 5% |

| OP CAGR | 2.5 times | 2.12 times |

| Latest ROCE | 14.76 from the earlier levels of 5-6 | -6.87 from the earlier level of -7.3 |

| Latest ROA | 5.73 | -9.92 |

| Asset turnover | 1.17 | 0.84 |

Similar performance is seen for the 9M of FY24 despite Mcdonalds facing flood issues etc. in its geographies

1 Like

Vineet_Bhatia Would very much appreciate if you could please share links to this video. Thanks

1 Like

@Vineet_Bhatia while looking at mcap/store have you considered only india stores or included indonesia numbers too?

Also, are you still a buyer in this? considering indonesia numbers too, mcap per store currently is around 6 Cr. I have considered "BK India Stores+ BK Cafe + BK Indonesia + Popeyes Indonesia " individual numbers to calculate total stores and have not added debt currently.

Thank you for sharing the link, very much appreciated

1 Like

You can easily search on youtube by my name and vivek bajaj, thanks

That time only india stores were considered. I would still say look at market cap per india stores and discount everything in indonesia as its not broken even yet.

India stores have become cash positive.

Disclaimer: still invested, as thesis is still playing out well, have lot of levers to play here.

8 Likes

QSR company:

in a country like India

offering value fast food meals + coffee cafes

around 450 stores

available at 5k market cap

looks no brainer

Disclosure: invested

6 Likes

I feel that big QSR brands wont do as well in the near future atleast in India, as a stock time and again they might if there’s a bargain but it wouldnt be a big wealth creating sector…I feel the golden days for big QSR chains are behind them…

— I think historically there have been giant winners in this sector like McD,Dominos etc which leads to a sort of a bias. The notion is because they have worked so well in other countries,India is untapped and hence a lot of potential etc…that line of thought

— The other is with the prevalence of Zomato/Swiggy the delivery moat that these big QSR’s like dominos enjoyed is gone. It is a level playing field for everyone .Plus the competition is much more intense…So many new burger/pizza/biryani brands if you do a search on swiggy/zomato.

It is a crowded space right now . and because of this Zomato was a no brainer at around 50 rs not so long ago…

8 Likes

With regards to above posts from @akhilgulecha & @Anand1989 the younger demographics who consume such items frequently may be once or twice a month tend to experiment more by trying out different brands/tastes each time while the older demographics who consume such things once a while may be once or twice in 6 months largely tend to stick to their liking (taste).

Thanks for your comments, my convern has been should we discount Indoneisa or flag it as a risk of capital allocation?

When everything was going so well in India, Indonesia happened. It was considered as not a good capital allocation by many when already India presents huge opportunity of investment. Was it done to provide exit to sister PE not sure…

Can we trust amd hold long term a company with unpredictable capital allocation? Your thoughts welcome on Indonesia investment.

Disc: Invested a very small position. Had trimmed sometime back when needed funds.

they have mentioned no more BK stores in Indonesia in near future + cost cutting.