Then why purchase it in the first place? And what stops a Malaysia etc. next…

No one knew about Indonesia until it happened

1 Like

Hi Sir , what are your views on promoter selling situation now ?

( As selling was not strategic )

and

when do you think situation will normalise in Indonesia ( due to Israel - Palestine war )

& breakeven of indonesia business ??

Its was pushed i to their throat by parent RBI, my way to look at it is, since RBI thinks management is good and has potential to turn india, give them indonesia too to make it turn around.

In fact they r doing pretty good job at that.

In terms of capital allocators, i think they r pretty much in good shape and Parent RBI is also known for good capital allocation

3 Likes

Just wondering why Parent RBI did not give Popeyes to this entity RBA (where it hold some stake, if I am right - 15%*0.4)and gone had with Jubilant Foodworks though RBA have franchise for Popeyes in Indonesia. In past, if I remember correctly RBI had 40% of promoter company not sure what it is now after Everstone sell. Thanks!

avoid these meat franchises which have high cost structure. Rather look at Specialty Rest. Thye have a Indian brand management , lots of hit restaurants bars, cloud kitchen and amazing variety and quality and most importantly making profits despite heavy renovations in India and around the world. this one is a good one . they make profits and thats important. we have been sold the middle class scaling story because of Jubilant Domino success. cant be repeated for RBA … Go with quality and where the well to do dine and order in

2 Likes

Looks like an interesting business.

India at 450 stores, going to 700 by FY27.

Assuming it’s done evenly= 18.8% growth coming from store addition.

Moreover, majority of the stores are laid out and hence they should start maturing which will lead to good SSSG growth. Taking 6-8% of SSSG, the India business will grow at 25-26% with interest costs and description increasing around 20%( SSSG allowing operating leverage) and SG&A expenses increasing moderately.

India business looks very promising, could surely achieve profitability in near time.

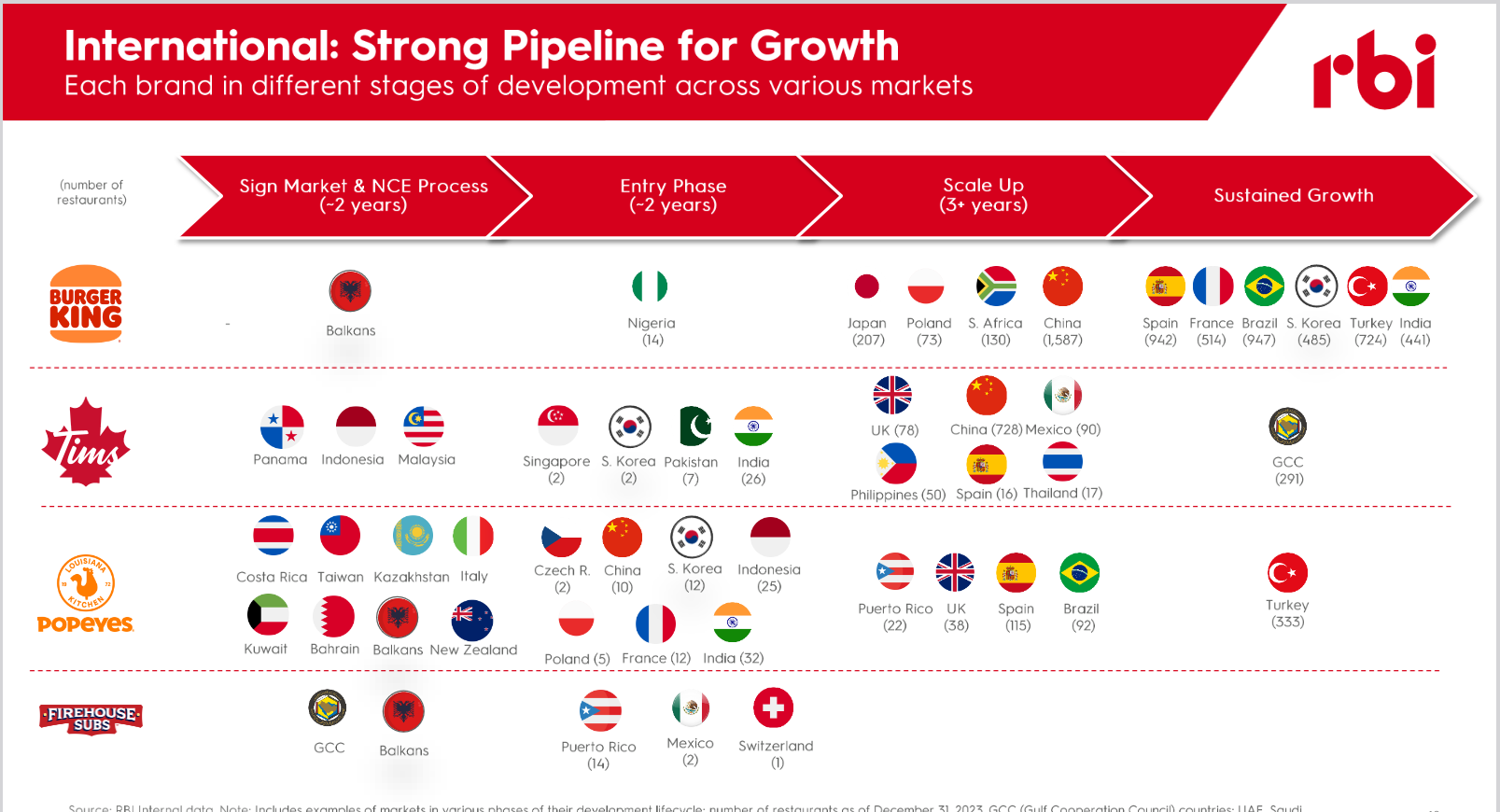

Indonesia business a bit worry, BK Indonesia won’t add any cafes and will consolidate the business, which is really good in the long term and is an example of strong capital allocation, however the headwinds are a worry. Don’t know how long will they stay

Popeyes too a bit disappointed. from ADS to 50 million to 40 to 23. Expected it to be a big growth drive with 2x ADS of BK but doesn’t seem like it.

4 Likes

Restaurent brands Asia.pdf (48.5 KB)

Yes, in the recent con call, it was mentioned that RBI sits on board of RBA and owns a stake in RBA

It is under promoter category. Earlier, 60% of promoter entity was held by private equity firm - everstone capital but they sold out so I think it is shows holding for RBI only.

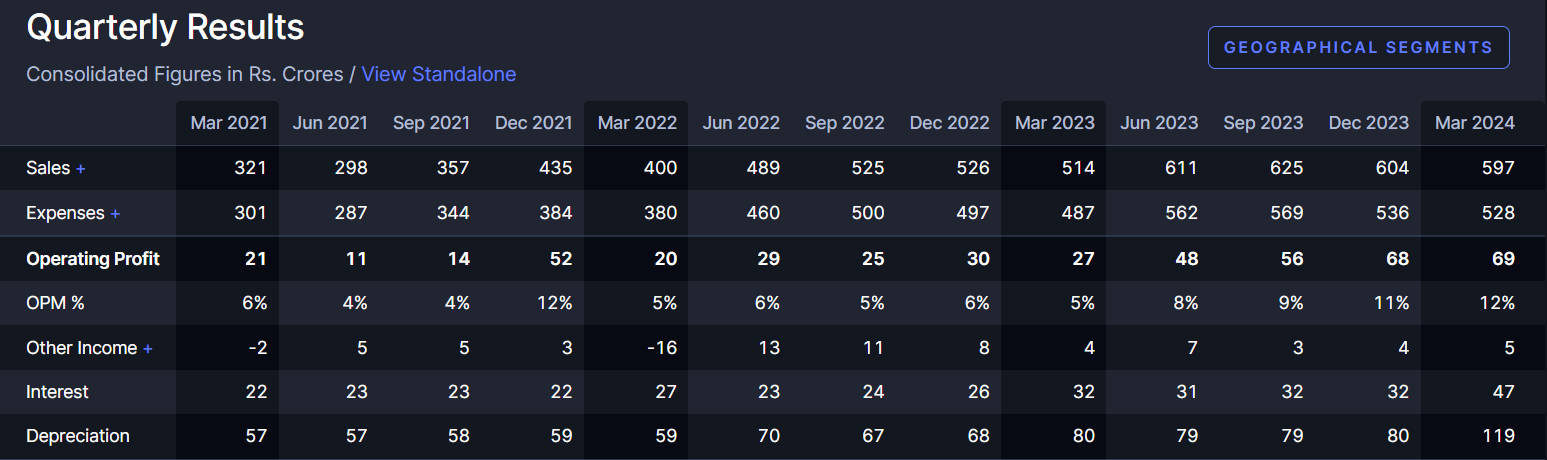

Over the last 2-3 quarters, even while all domestic QSR brands have shown de-growth at the unit level, RBA has shown improvement in kpi such as SSSG, while continuing with their store expansion plans.

And thus I have recently done a deeper analysis of the business…

It seems business is at a good pivot point after 10 years of domestic operations, having built 455 restaurants over this short period. The McDonald’s franchise Westlife entered the market in 1996, almost 14 years before RBA, and has 397 restaurants in West and South India.

Improving traffic through a value strategy… The value strategy has resulted in lower AOV (Average order value) but increased SSSG (Same store sales growth) and ADS (Average daily sales).

While simultaneously increasing their gross margins… achieving through supply chain efficiency. Gross margin reached 67.7% in Q4FY24 from 66.4% the previous year, with guidance to reach 69% by FY 27. Westlife has gross margins of 70%.

EBITDA level profitability was achieved in India, but geo-politics delayed profitability in Indonesia.

Operating leverage plays out in such businesses… as marketing costs although remain stable at 5%, other fixed costs get distributed over a much larger base with scale.

Continued expansion through FY27 to meet 700 store target… to reach this, 80-85 stores per year will be opened for the next 3 years, a 16% CAGR through store addition. If SSSG recovers, top-line growth of 20-25% is achievable.

Debt… mainly for the Indonesian business, the India business has been grown by raising capital through equity. The outstanding borrowings in the books of PT Sari Burger Indonesia as of March 31, 2023 is Rs 165 cr.

Equity dilution… is present

Negative cash conversion cycle… has led to a 10x growth in cash from operating activity from March 21 to March 24, benefiting growth through internal accruals. The company also showed positive FCF in the current year (both at consolidated and standalone basis).

Indonesia business… has been the reason why the business has been given lower multiples. The company has guided that no new capital allocation will be done in the business in FY25. This should help weather the current slowdown in the country while improving unit economics, thus reducing drag at the consolidated level.

Closest competitor, Westlife… has shown operating leverage play out in the last 5 years, along with FCF generation while focusing on growth. The return matrix has also significantly improved. When compared to Westlife, while RBA was much behind in the business lifecycle, the improvement in returns appears sharper.

Beyond FY27… When store addition slows down, it could be fair to say that the company can achieve unit growth and profitability at least in line with Westlife, i.e., ADS of Rs. 155,640 (currently at Rs. 117,000) and Restaurant operating margins and Company operating margin of 22-24% and 15-17% respectively (currently at 19% and 14%).

Valuation - Available at P/S of 3x, while Jubilant, even after the de-rating trades at 5.8x, and Westlife is given a 5.5x multiple.

As the business cannot be evaluated on earnings I am taking CFO as a comparison matrix. The OCF generation of RBA and Westlife have been similar in FY24; thus the P/OCF of RBA and Westlife are coming to 16x and 38x resp. Even if West life deserve a higher multiple due to stronger brand recognition of Mc Donald’s there could be some scope for re-rating for RBA if it continues on this growth trajectory.

Branded business… have proven to be high ROE and ROCE businesses over the long term; like FMCG, branded pharma, branded hospitals, Titan, Trent, etc. by taking market share from local players. These businesses have longer gestation but led to a deep brand moat, resulting in higher returns and FCF generation.

Jubilant was the first entrant within the Indian QSR segment (1995) and we have seen that play out.

Based on the above theory and the improving financials, I believe that the business is becoming a good candidate for stock re-rating and earnings led growth if the slowdown in QSR segment eases out…

20 Likes

Agree with you completely. It’s a very good bet on the Indian space.

One doubt though, how do you evaluate the Indonesian business and its scope in the future? It’s clearly the one that’s dragging the business down. Its revival can lead to RBA finally breaking out

Indonesia business will largely depend on its economy. These brands normally grow with growing middle class.

1 Like

True Indonesia business has been a drag on the consolidated business so far.

But if u see they have managed to EBITDA and Cash breakeven, get to +ve SSSG (which they achieved in Feb), thus helping it stop the pressure on the consolidated P&L. Decision of not adding any new allocation into the Indonesia subsidiary until the geo-political situation improves, also neutralises the risk to balance sheet. This decision would also help improve KPI (at unit level) as the existing stores mature. They have also done some 20% cost rationalisation at corporate levels; hence the effect closure of 15% under performing BK restaurants on fixed costs, should be taken care of.

I believe if the above continues, the Indonesia business will be overlooked and India business might get it’s required re-rating.

3 Likes

Yes and the Indonesian economy is also not a bad story with urbanisation, real gdp growth, and positive demographics. If the anti US sentiment eases out, they can leverage their under penetration in the country.

2 Likes

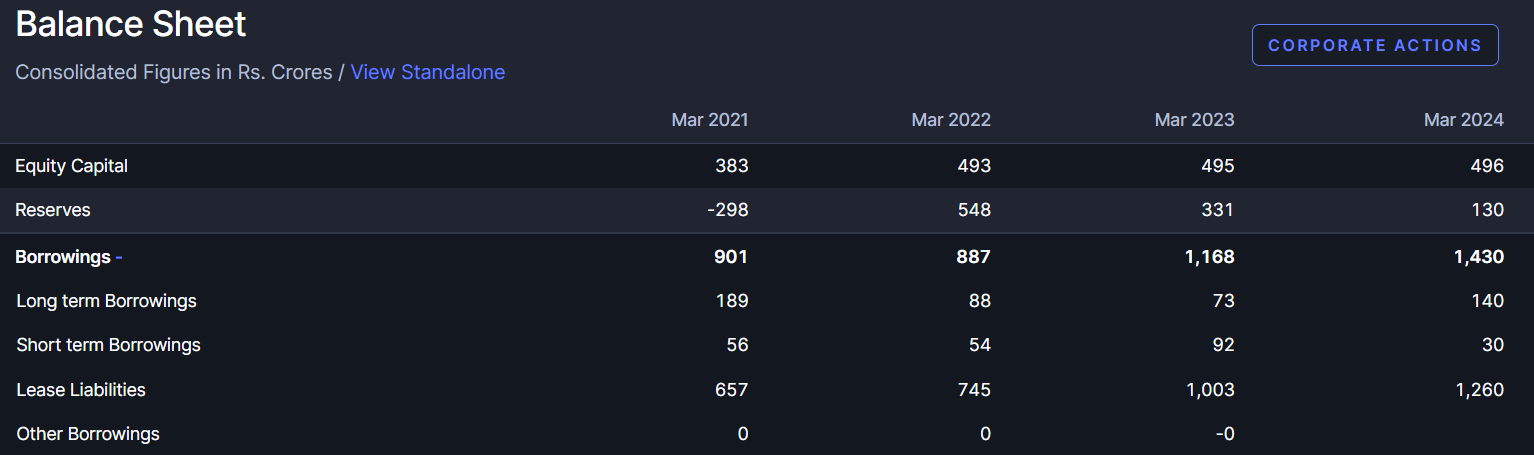

I am new to this company, and need guidance from fellow boarders to understand their debt position.

As per the balance sheet on screener, they just have 170cr of debt. Rest is just the leasing commitments:

Then why the interest cost is so high?

47 cr for last quarter, and 141cr for full year.

1 Like

on account of IND AS 116 accounting where they have to derive interest and depreciation from lease payables payables separately.

2 Likes

You have to look at pre Ind AS numbers as lease is counted as debt in post ind AS numbers. While lease is an operating expense for this kond of business.

2 Likes

I understand that lease is shown as debt. And thats why my question is – why is interest payment so high?

1 Like