Better results in this environment,Maintaining gross margins at 66%.

Store opening count on track.

Seems that profitability is just around the corner.

Disc-Invested since IPO listing day.

investor presentation-burger king-jan2023.pdf (4.2 MB)

Better results in this environment,Maintaining gross margins at 66%.

Store opening count on track.

Seems that profitability is just around the corner.

Disc-Invested since IPO listing day.

investor presentation-burger king-jan2023.pdf (4.2 MB)

In such a event, does one get X shares of Jubilant (say) for every Y share of RBA? or we need to exit?

Let them announce it officially. If it turns out as a merger then you will get shares of Jubilant Food (if they acquire them). But if they don’t merge then shares of RBA will continue to trade.

Seems like similar news of selling by Everstone parent group are resurfacing again in market, better wait for official news from RBA. Link to old news

Moving onto the other question in terms of merger/acquisition, we can take an example of Hero’s investment in Ather. Even though both are in same line of business, Hero has bought up 40% of Ather to get the EV edge as they know it will be the future. Similarily here in our case if Jubilant has to acquire Burger King I don’t think they will do so to kill the brand when it is so close to breakeven ( End FY24 ) or maybe to get the rights of Popeye’s.

Just to summarise, let’s stick by and see how this pans out instead of speculating on a repeating news ![]()

Happy Investing !

is anybody attended the AGM? Please share highlights.

Q1-Investor presentation, Good revenue growth in India business but subdued store opening s in last 3 months.

RBA-INVESTOR PRESENTATION-Q1.pdf (4.3 MB)

I did a small scuttle but. I interacted with a Zomato delivery boy in Ranchi, Jharkhand. Here recently Burger king new store opened, and he told me that sales of burger king is very good. Infact, it’s beating KFC near it. I have seen more crowd in general in front of Burger King as compared to KFC near it.

Also, I personally liked burger king Burgers more than KFC’s. And

Any idea who will be the new promoter of RBA?

Restaurant Brands Asia: Bulk Deals

SELER

![]() QSR Asia SOLD 25.353% @ 119.1

QSR Asia SOLD 25.353% @ 119.1

BUYERS

![]() ICICI Prudential Life BOUGHT 6.8718% @ 119.1

ICICI Prudential Life BOUGHT 6.8718% @ 119.1

![]() Plutus Wealth BOUGHT 6.0633% @ 119.1

Plutus Wealth BOUGHT 6.0633% @ 119.1

![]() Quant Mutual Fund BOUGHT 2.8296% @ 119.1

Quant Mutual Fund BOUGHT 2.8296% @ 119.1

![]() Tata Mutual Fund BOUGHT 2.5264% @ 119.1

Tata Mutual Fund BOUGHT 2.5264% @ 119.1

![]() Franklin Singapore BOUGHT 1.6696% @ 119.1

Franklin Singapore BOUGHT 1.6696% @ 119.1

![]() Goldman Sachs BOUGHT 1.3137% @ 119.1

Goldman Sachs BOUGHT 1.3137% @ 119.1

![]() Amal N. Parikh BOUGHT 1.0287% @ 119.1

Amal N. Parikh BOUGHT 1.0287% @ 119.1

![]() TD Emerging Markets BOUGHT 0.8085% @ 119.1

TD Emerging Markets BOUGHT 0.8085% @ 119.1

![]() Plutus Wealth BOUGHT 0.8084% @ 119.1

Plutus Wealth BOUGHT 0.8084% @ 119.1

![]() Societe Generale BOUGHT 0.3436% @ 119.1

Societe Generale BOUGHT 0.3436% @ 119.1

![]() Dovetail India Fund BOUGHT 0.3254% @ 119.1

Dovetail India Fund BOUGHT 0.3254% @ 119.1

![]() Citigroup Global BOUGHT 0.2122% @ 119.1

Citigroup Global BOUGHT 0.2122% @ 119.1

![]() Nomura Singapore BOUGHT 0.2122% @ 119.1

Nomura Singapore BOUGHT 0.2122% @ 119.1

![]() Avendus BOUGHT 0.1697% @ 119.1

Avendus BOUGHT 0.1697% @ 119.1

![]() N V Investments BOUGHT 0.1697% @ 119.1

N V Investments BOUGHT 0.1697% @ 119.1

RBA was trading at discount becuase of this overhang of promoter sellling , may be it will catch up with the like of Devyani , Jubiliant …

With no promoter skin in the game, can they really have a clear and focussed stratergy to achieve the required scale and improvement in margins/profitability?

Anyone has any views on what this could mean?

The promoter in our case is a PE Firm which has a definite term life for any investment as opportunity cost is a big thing for them. In our case , I am believing it to be a good overhang which is holding the prices at this level as compared to McDonalds they have rights all over India+Indonesia.

Do read this detailed thesis from one of my mentors and your answers will be answered ![]()

Hope this gives clarity.

Noticed same case in Patna. Here too random delivery guys told that customers are preferring Burger King over KFC.

While everyone likes BK… please note their real competion is from McD . And McD is in a totally different value propostion with full family offering inclusing parties and far easier Gen Z produxts .

Also BK is exposed to indonesia where profit margjns are low and risk is high due to cost

Strong results on the numbers front once again, record revenue and EBITDA for India, and reasonable revenue growth in Indonesia keeping in mind the closure of underperforming stores. Co remaining on track for number of stores guidance for BK India and Popeye Indonesia is also encouraging.

For BK India - Product line-up boost with a wider chicken menu (Bone-in and Boneless wings, Nuggets), value for money offerings - Whopper promotion and 99 Rupee meal, BK Cafe present in all new stores (with a low base in terms of ADS contribution at the moment) may collectively help margins, ADS and in-store traffic growth

Indeed, numbers and the management commentary are good. The only concern is the promotor selling their stake…

Wow @puro , you have done some good scuttlebut !

On the promoter selling - Ashish ji, the way I prefer to see it is that the stake sale overhang will no longer be a factor in limiting the upside if the numbers remain on track. Also for a company that is now a ‘mid-sized’ Smallcap (5000cr+) there is now a solid institutional holding.

And on the scuttlebutt - Thank you, my work outside of investing (Poultry industry) is helpful for a few companies like RBA ![]()

I had written this short note on RBA for internal discussion purposes. The notes released by Solidarity are great and cover most of the thesis needed to understand this business. I’m sharing a few additional pointers on why I like this business -

Great Track Record

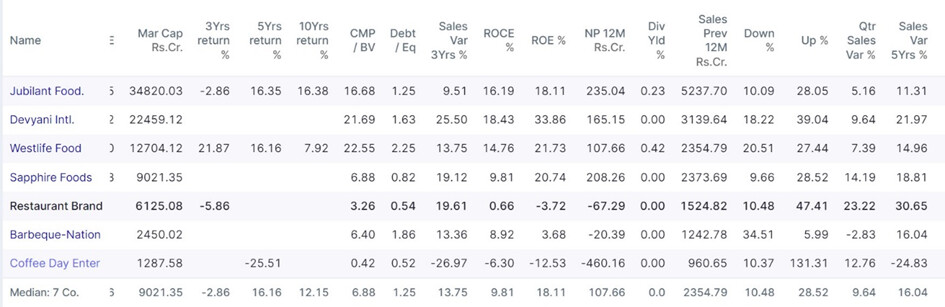

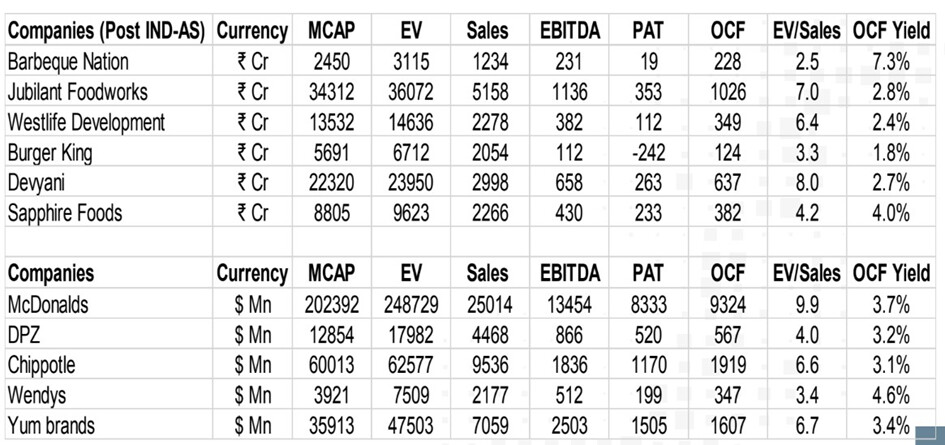

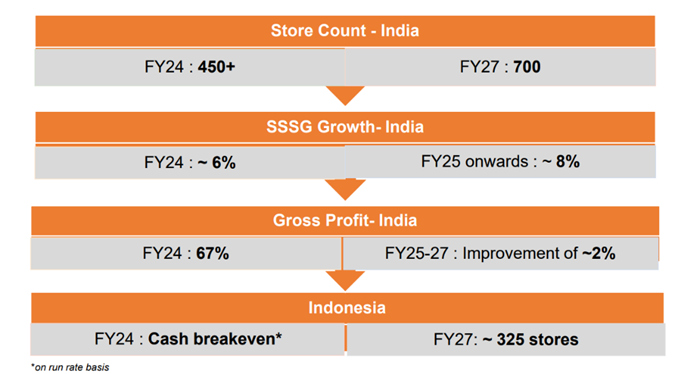

In spite the fact that Burger King started operations only in 2014, the company has already grown to over 400 stores and 1439 cr. in revenues. For comparison, Westlife Foodworld (McDonalds) has been in India for over 25 years and has revenues of 2278 cr. with 370 stores. BK India has grown its revenues at 31% CAGR for the last 5 years, highest in the QSR industry.

I also feel BK has “cracked” the code required to be successful. Their menu, taste, pricing, location, etc. seem on point. While doing scuttlebutt with my friends and visiting BK stores and malls, I have seen the acceptance this brand has gained, something other QSR players such as Pizza Hut, Dunkin Donuts or Subway have struggled to do. Their value pricing, localization of flavours and quality of product has found an immediate audience in India.

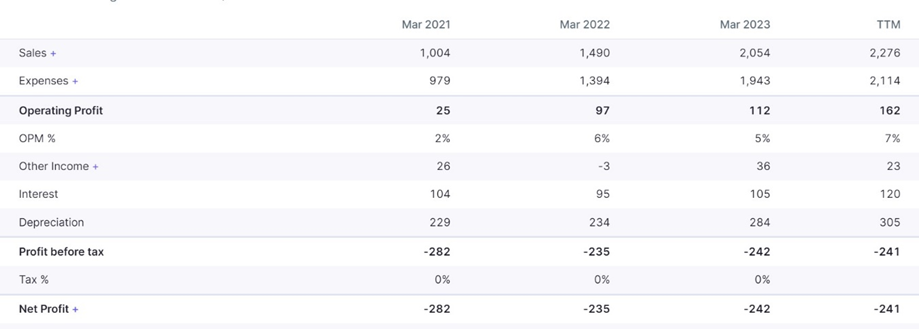

BK also has excellent unit economics at the store level, with ~66% gross margin, almost on par with McDonalds. While there is operating profit, it is PAT negative today because they are in their expansion phase so there’s high interest and depreciation costs. QSRs have significant fixed costs at both, restaurants, and corporate level. As the number of restaurants reach a critical scale and the revenue per restaurant increases, a large share of the incremental revenue should flow through to profits driving exponential profit growth.

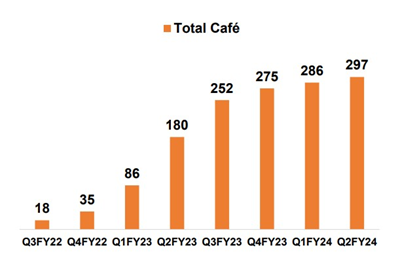

They started BK Cafe in 2022, and it has already scaled to 297 cafes. BK Café sells higher margins products such as coffee, muffins, tea, etc. It has gross margins ~75%, thus leading to improvement in overall margins.

QSR is an attractive industry

Eating out is a multi-decade structural growth story. The number of meals per month consumed out of home increases with GDP growth and rising per capita income. This is an affordable category people want to explore.

There are two reasons I prefer Burger King over other QSR players –

1) Pan India rights – Except Jubilant, no other QSR player has rights all over the country. This automatically means that the total addressable market for Burger King is twice that of other QSR companies. Not only that, but they also have the optionality of a fast-growing Indonesian market as well.

2) Low valuation – For some reason, Burger King is also valued at the lowest when evaluated on Mcap/Sales. This may be because the company is still loss making, or there are worries about sale by the PE Promoter. However, this is surprising to me because BK has grown the fastest among all QSR players and should continue to do so in the future.

While there is competition coming in from new entrants and local players, I think it will be hard to compete with a brand like Burger King. Any new Burger joint will have to spend highly on marketing, supply chain and product innovation, whereas Burger King has the advantage of being a well-recognized global brand. They can enter any new city and the brand will already have visibility there, something local competition will lack.

Brand like BK, McDonalds and Dominos are still aspirational for most of India, especially kids and the demand for them will always be higher than any non QSR player.

Management

The bet is not on the PE firm but primarily on Rajeev and his team, who have shown great execution so far. He also has significant ESOPs in the company, so the incentives are aligned.

BK Indonesia

RBA raised 1402 cr. through QIP in 2022 to acquire the Indonesian business. This unit’s operations are run by a separate team and hence should not dilute any focus from India operations. Even though I would have preferred that they stick to India, considering the immense growth potential here, the Indonesia opportunity can be an optionality that can add a kicker to the returns with limited downside.

Valuation

I have done no fancy DCF or valuation of RBA. The bet is primarily on the huge opportunity size, good track record, growing industry, a strong brand name and extremely long runway for growth. There is immense opportunity to reinvest the cash flows generated and low risk of disruption. India has over 8000 cities and towns, and there is no reason why there can’t be a Burger King in all of them. They plan to open 700 stores by 2027, and hopefully should continue to open at least 80-100 stores every year post that as well.

RBA currently trades at less than 2x Mcap/Sales. This company has grown at over 30% CAGR consistently in the last decade and even if they are able to grow at 20-25% in the next decade, there is immense potential to make money not just through sales growth but through re-rating as well. This in one of those rare business that ticks all the boxes of long runway for growth, excellent track record, strong brand and decent valuations.

Key Risks

As per the Master Franchise and Development Agreement with BK Asia Pacific (holder of rights of Burger King), the company is obligated to open at least 700 stores by 31st December 2027. If the company fails to do so, BK Asia Pacific has the power to terminate the company’s development rights or the Master Franchise Development Agreement. Also, the company cannot have a debt-to-equity ratio of more than 2:1 at any time.

The promoters of the company are the PE firm Everstone Capital who are looking to exit the company. They did a sale last year and only own ~15% now. Any change in ownership could result in change of management. The bet so far is on Mr. Rajeev Varman and his team.

The entity is loss making at PAT level. Consistent monitoring will be needed to ensure that the unit economics are strong, and the company does turn PAT positive in the near future.

Disclosure - Invested