Yes, I did see that earlier. Dominoes risk may not come into picture as Indian listed entity is Restaurants Brands Asia (with parent having equity stake) and Dominoes belongs to a different parent.

But you never know if the PE need Dominoes exit and Restaurant Brand parent sell their stake in RB Asia and they end up buying Dominoes Indonesia with simultaneous name change to Brands Asia or something else

Disc: Again hypothetical, but what else we small retail investors have to understand future capital allocation strategy of this company?..unless company gives some statement on this strategy and abides by it in future?

1 Like

this is something that they have mentioned repeatedly in many concalls. Nothing unique here.Most QSR chains across the world at some point employ a version of this so called barbell strategy. Every QSR is trying to get the max out of the customers wallet so Having a strategy is fine but is there any indication that it is working? Have they successfully been able to upsell? BK Cafe could be interesting if it works but too early to say

3 Likes

Nice comparison…I think Indonesia acquisition has dented stock performance by huge margin. Had not been for this acquisition, BK would have performed lot better…

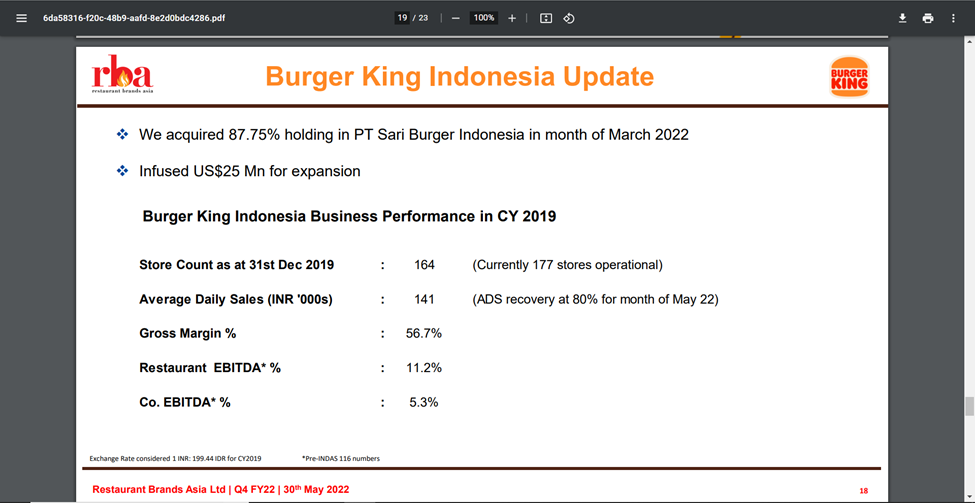

Would be good to have similar data for BK Indonesia, if available…Thanks

1 Like

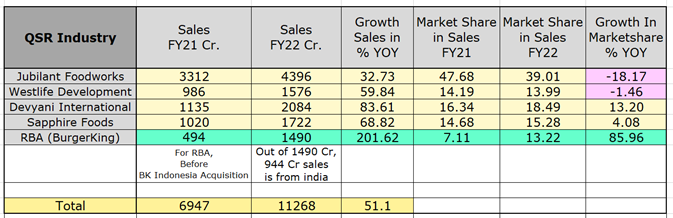

How did its sales become 200% from 500 to 1500 for RBA? That’s an extraordinary claim by RBA when others are less than 100%! When did people’s habit in the narrow QSR market shift that markedly to BK?

Please check all results. Co’a balancesheet & Recent developments.

Hi Chirag

Kindly corret me if I’m wrong, I think Market share of burger King would be around 8.6% of Indian QSR market, as we are calculating Indian market share of BK peers.

If you calculate only India sales of 944Cr. it have market share of 8.4%. but we have to now see RBA as consolidated sales. So, in FY22 they had 1490Cr sales. & total listed QSR sales of FY22 is 11268 Cr… So this make RBA’s market share of 13.22%. Even i believe that Indonesia acquisition is good for co as Indonesian business has more realization than India business.

See Indonesia’s growth. what i did not like about this acquisition is they diluted share capital in a big way. so my only concern about this co is whenever they need fund they will dilute share capital by this our return will also get affected.

2 Likes

See here we can compare both India & Indonesia Business.

I am expecting minimum 750 Cr of Sales from Indonesia in FY23.

1 Like

Solidarity PMS has initiated new position in it.

4 Likes

Burger King Indonesia has acquired franchise rights for Popeyes and plans to open 300 outlets in Indonesia in next 10 years.

IMO it’s a positive news for restaurant brand investors

For India, I think Jubilant foodworks has the franchise rights for Popeyes.

9 Likes

As per Credit Rating Report -

Favorable capital structure and adequate liquidity profile –

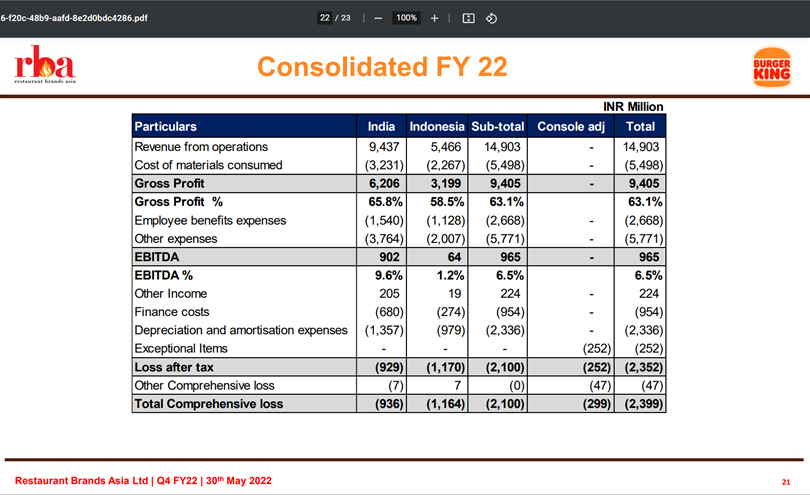

The company’s net worth in FY2022 at a consolidated level remained strong at Rs.1040 crore, boosted by recent QIP placement of Rs.1402.14 crore in March 2022.

The external debt is only for the Indonesian subsidiary, which remains limited at Rs.141.9 crore.

The capital structure at an aggregate level remained strong, depicted by low gearing of 0.8 times as of March 31, 2022. The liquidity position also remained comfortable, aided by healthy unencumbered cash balances and considerable liquid investments of Rs.679.5 crore at a consolidated level as on March 31, 2022.

Liquidity position: Adequate

The company`s liquidity position remains adequate, given at a standalone level RBAL does not have external borrowings(except lease liabilities) and, thus, has no scheduled repayment obligations while on a consolidated basis there is term debt of Rs.141.9 crore on its subsidiary’s books.

Further, on a consolidated level, the company has healthy liquid investments in the

form of liquid mutual funds and unencumbered cash and bank balances which aggregated to ~Rs. 679 crore as on March 31, 2022. The company has aggressive expansion plans for its India operations, however, the same is expected to be funded by internal accruals and liquid investments available on books.

A small scuttlebutt.

The mgmt has been beating up their drums regarding rolling out of the app. Installed and tried to use it today.

- App stopped responding several times where I was stuck with a white screen. I can’t imagine how much load would selecting a few items would put on the app such that it crashes several times. I backtested the load by running several much heavier apps like insta, spotify, youtube etc. separately and verified it wasn’t a phone/internet issue.

- The same OTP was being shown as invalid at least 5 times before it got accepted the 6th time . Yes. THE SAME ONE!!

- Another poor observation : I wasn’t able to see Burger King on swiggy and even zomato discounts were too low (usually they offer 40%-60% for most items). Even if you’re trying to divert people from third party apps to your own app, the process should be gradual and you shouldn’t delist from swiggy(bangalore) so fast. The baap of QSR dominos is still available on both 3rd party apps and their app is much better than us.

6 Likes

can anybody tell me that why depreciation is too high ?

Screener BSE link shows as moved.

One can use this:

1 Like

Agree to disagree, I have been using their app continuously in allahbad a month back. And the ease of scrolling and the UI is too good. may be there was a one time issue with you.

and regarding their offers, its quite alluring - not giving any direct discount or cashback , rather giving extra burger or fries or shake as per your cart. this helps them also as they make almost 66% gross and this gives customer a very good feeling of getting real discount. so imo its a good cycle and system that they had created will help them get direct customer insights ( J-curve effect)

3 Likes

Sure. Thanks for sharing.

Although I recently completely exited . I don’t see profitability and positive earnings from old stores will not be visible for long enough to generate even mediocre 15% margins in 5 years. Find other businesses not QSR limited much better. This was a learning for me as I was drawn to unprecedented rise in number of stores. Constant 60% discounts on zomato was no prize as well.

1 Like

In a series of complex transactions, yet again due to happen…this time no acquisition but the PE selling its stake…

Any idea if Parent Burger King would still hold equity after the Everstone exit? Also, who could be prospective buyers?

This exit was bound to happen, never thought it would be so quick…cannot understand this PE owned businesses…our traditional Indian business houses owned seem much simpler and better…

Disc: Invested hence critical. Not eligible for any advice

Everstone Capital plans to sell Burger King stake in India and Indonesia | Business Standard News (business-standard.com)

3 Likes