I think as COVID curbs are easing in India Burger King India i.e. Restaurant Brand Asia too should report better sales in fourth quarter, only spoiler might be higher inflation on food items e.g. edible oil, sugar, coffee etc.

Following is the news on Restaurant Brand (USA), (Burger king India parent) about latest quarter results…

Restaurant Brands (NYSE:[QSR] stock rose 1.4% after the [Burger King parent] beat quarterly revenue estimates at its restaurant chains after Covid-19 curbs were eased in Canada and the United States.

2 Likes

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=15ac8786-8b21-47b4-9547-8897bde85bc4

The exchange has sought clarification from RBA on share price movement. There must be a background to this query in terms of potential news. Any idea what is being referred to ?

QIP was about 129 and it seems after getting alloted some fund has sold it . There was a huge volume on the day when the war started and all shares dropped . Not sure whether it is some fund or retail .Indonesian business is not so good compared to India business because of less margin and very high competition . It needs to watched how management will execute and how 1500 cr is used .

Don’t understand why any fund would buy at 129 only to sell at around 110 the very first day of listing of new allotted shares?

Doesn’t make any sense to me. Insights welcome.

2 Likes

Have made a report on Burger King ( restaurant brands asia)

https://t.co/Vx4j3Lccdd

visit the link to view the report

8 Likes

Why is parent company launching other brands through different companies?

1 Like

Can you mention more details like which brands and through which companies?

Please check parent website www.rbi.com

Search for India and you should be able to get news items

https://www.rbi.com/search-results/?SearchTerm=india&category=&page=1

Question is why will someone payup for this company who is just a franchisee for one brand for 10 years and has a recent past of capital misallocation (acquisition of Indonsian) at behest of parent company.

2 Likes

Agree but sadly what other option we have in QSR space other than these franchisees? That is if one has to invest in QSR.

Jubilant is also a mere franchisee but has been a 40x in a decade or so…

Regarding multiple brands of parent with different franchisees…same is case with Yum brands also …they make sapphire and devyani compete in India…

Jubilant was a 40x on the back of almost a single Domino’s brand so far…

Now why do parent does this …i think it is simple as a parent I would want to derisk that is one…other reason is if I have a franchisee with pressure to expand say burger King brand for next 5 years, i very well know they cannot handle the pressure to expand Popeye…for that I would chose another franchisee which has that bandwidth and jubilant has that along with proven track record of Domino’s and near saturation on its capex…

As an investor, I have option to either ignore this space completely as all these franchisees have same status or invest with this known liability…

The only concern I see here for burger king is the Indonesian acquisition and I am not able to make out much of it…it had simultaneous name change of company along with it to Restaurant brands Asia…so what’s the vision for this franchisee I am not sure… although I think it’s one of rare franchisee in which the parent holds significant equity…if I am not wrong?

Another important general aspect is that these are franchisees not limited to single parent…as I can see from a Jubilant example which would cater to multiple parents…so would be good to know how this aspect is handled in each one’s contract…and would it help these franchisees to have some sort of upper hand with parents subsequently? Although I don’t see them ever having upper hand with any parent…

Disc. Invested in QSR space and hence biased. Above thoughts only for academic purposes and no buy/sell recommendation

7 Likes

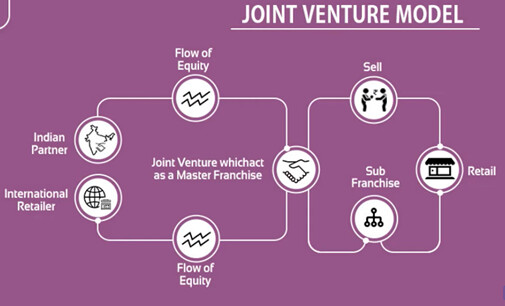

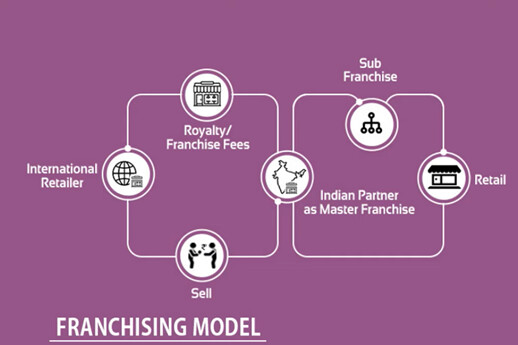

First of All. Burger King India (Now RBA) is JV of RBI with Everstone Capital. Its not Franchisee Model like Devyani International & Sapphire Foods. Here Parents have skin in the game.

Here Co’ survival, growth, profitability and failure as well are directly belongs with parents. So JV model is much safer than Franchisee model.

On question about rest of the brands, Burger King is their most successful brand and so they go with direct business in Burger King. Why they are giving their others brands as franchisee/ JV (Like Tim Hortons/Popeyes) to other cos because the wanted to grow their foothold in Other geographic to earn more royalty (In case of Tim Hortons they are planning JV also with Apparel Group and Gateway Partners). So, They will earn only royalty. In case of RBA they will earn Profit+ Royalty (as they running the business itself via JV.)

So In Long long run there will be no surprise if one fine day they merge even Burger King Russia in this business — just for Example. Even i have contra view on what other thinks for RBA. I see strong growth with Best management for Famous Brand “Burger King”. Even in India QSR space i am most bullish on Burger King. In starting years they don’t even need to be profitable in bottom line (even as investors we should not look at/ expect positive bottom line rather we have to look for cash generation). Because they are in Expansion mode. They are EBITDA positive + cash positive. Depreciation will keep bottom line negative. But They will grow Top Line+ EBITDA +Cash in exponential way. Market will sure look at it.

What i not like is share capital expansion. It will dilute our return. if management from here not dilute share capital more than we have next multibagger of QSR Space.

*Biased and invested

6 Likes

Thanks for highlighting differences, i also see this as unique franchisee where parent has significant equity…what I did not know is that burger king is not doing business in India as a franchisee but rather a JV…

In this context, could you pls help understand above difference of why a JV earns only royalty and another JV earns both royalty and profits?

To me - it should be either a royalty or profits (except of course a royalty + dividend in case parent holds equity in its franchisee)

I was thinking over this equity dilution in quick time and regularly so far in case of burger king and one reason could be that their contract demands significant expansion without ever increasing debt equity ratio beyond 2…it currently stands at around 1…so as a safeguard and prudent management, it makes sense to dilute equity to fuel expansion (in this case even foreign acquisition) via equity when markets are doing good…

However, I would be fine if such dilution is for indian expansion but if it is for acquisition, then you don’t know when this cycle would end and as small investors we would always be guessing what acquisition next…would be great to know your thoughts on this important aspect…

Lastly, since I see you have so beautifully explained different type of QSR model in India - I do not understand why would RB parent would go on a contract with itself? (As RBA is in essence its own subsidiary via significant equity and if they would share profits as well)…a contract with itself does not make sense to me …

Thanks

Disc. Same as above

1 Like

Best Video by Anish Moonka of JST investment. I am sure it will clear your doubt about JV Model & Franchisee Model.

1 Like

BK is still a growing brand in India when compared with established brands like McD.

Giving RBA all the brands which are yet to be established is a perfect recipe for disaster as all three capture different taste profiles.

I would rather like the mgt to focus on BK for now.

Disc Invested and Biased

1 Like

I don’t think RBI is a shareholder. Promoter is Everstone capital which is master franchisee for Burger King in Asia through QSR Asia Pte.

1 Like

There seems to be a lot of confusion on this thread as to who owns burger King India. QSR ASIA PTE(promoter) is a JV between the parent and everstone. Screenshot is from annual report(Pre- QIP). Company has exclusive Master franchise agreement valid till 2039.

With regards to the Indonesian acquisition here’s an old article that might help. Those interested can read and arrive at their own conclusions

https://asia.nikkei.com/Business/Business-deals/Everstone-Capital-said-to-eye-exit-from-Indonesia-s-Burger-King

3 Likes

Thanks for sharing, parent seem to have about 14% equity stake. Also, Everstone exit from BK Indonesia looks similar to how Blackstone gave exit in Mphasis to one of their fund by purchasing from another of their own as they also couldn’t get suitable buyer…but in this case the purchasing is done via a listed company…

Also, in 5-6 years they may look to exit even India business…with such a history of shareholding changes across the globe, you never know when the parent also sells it’s stake…would be nice to have your & others thoughts on shareholding & Indonesian buyout…

Disc. Invested hence critical.

@Investor_No_1

Few thoughts

One might see strong topline growth over the next few years due to high store addition but i am not sure about SSSG in the long term. You ll appreciate that every time a new QSR store opens in an area there’s usually good momentum for the first 2 years. There are a lot of people who wanna try it and this is specially true for non- metros but what drives sustainable SSSG growth is repeat customers. Not sure if that’s happening for them. Personally i don’t know anyone who likes their burgers but then again I have spent most of my life in Mumbai. Would be helpful to hear others perspective on this.

Moreover, from whatever I have understood through their concalls, most of their customers see BK as a value for money brand.Management keeps highlighting the importance of Stunner menu (50 Rs an item) Most of their stores are in areas where GDP per capita is lower than the national average. can they get customers to spend more on regular Burgers? Also what happens to their gross margins if inflation persists? can they pass it on without effecting sales?

Despite these doubts I might have taken a position at current levels had it not been for the Indonesian acquisition.BK Indonesia wasn’t doing well and now the onus is on the Indian entity to steer the ship.

Investing here means taking a leap of faith and trusting the management to deliver. Not ready to do that yet.

One last thing- below snippet is from the QIP. Not sure what to make of it but might be worth asking the management in the next concall.

Disc: Tracking

8 Likes

I am posting here Snaps from Aug 2021 Con Call. where Kapil Grover (Chief Marketing Officer) nicely explained about their “Barbell Strategy.” Just go through it, you will find that their strategy is best as they use stunner menu to attract customers. so whenever customers come via directly footfalls in restaurants / online purchase they just check premium products with stunner menu and many of them will sure purchase or want to try premium products like Whooper or King’s Special menu. Also in his explanation you will find that how they step by step evolving brand penetration via marketing.

1 Like

I was thinking about the recent capital allocation by BK India promoters to buy Indonesia BK…as someone shared, it looked like an exit provided to the same PE (different fund)…just like Mphasis/Blackstone case…

No promoter would kill their own company by buying out new ventures if they cannot be viable…and I think BK India may have reached its limits now…To get a rough idea if at all we may see such acquisition in Asia (as it is now Restaurants Brands Asia) - can someone share if they know if the same PE has invested in any other Restaurant Brands’ brand (Burger King, Popeye etc.) in any Asian country?

If yes, then at later stage they may look exit from it and that can be a capital allocation risk for listed Indian entity. If not, then any big acquisition chances maybe less…

Disc: Above thoughts are purely random & hypothetical. I can be wrong in all my assessments & thesis above

Dont know about restaurant brands but they got Domino’s Indonesia. Picked up stake in 2014. Not sure if they have exited. Found this article Everstone to review exit plan for Indonesian food portfolios - Nikkei Asia