i will add here, they recently did offer for sale and whoever has particiapated in big way must have known and discounted the above one time exceptional loss .

disc invested

1 Like

The promoters sold the company, and the new promoters had to buy from retail investors (So called exit route). So their stake went upto 95 percent. And according to the rules they had to reduce the stake to 75 percent. SO it was a forced sale and not truly an offer for sale. Just putting everything in perspective.

1 Like

FLUOROCHEM, Monthly - This business got demerged out of erstwhile GUJFLUORO (currently GFL post demerger) in 2019 and has taken 18 months to go past the price it listed at post demerger. It has broken out of that on the monthly with strong volumes last month.

Fundamentally, the business is well covered in the Gujarat Fluorochem thread. The management seems to have demerged the specialty chemical business on purpose and appears to be more focused on the same going by the EC filings requesting clearance for almost 150 products, most of it for various fluoropolymers, end products of fluoro polymers like HDPE drums, LDPE liners, PVDF membranes, fluoro specialty chemicals in the pharma and agrochem space (some of the trifluoromethyl molecules -CF3 seem to have several applications in pharma drugs), LiPF6 which finds application as an EV battery electrolyte etc.

The valuation is almost on par with a peer like SRF but is way cheaper than a Navin Fluorine. I believe this lies somewhere in the middle and as the Fluoro specialty chemicals and fluoropolymer value-added product contribution increases (around 20% at present), the valuation multiple has lot of headroom to approach Navin Fluorine on a relative basis.

Some parts of the last concall (June '20 is the latest and there doesn’t appear to be one after it) I thought added more information on near-term dynamics of the business which should improve the margin profile.

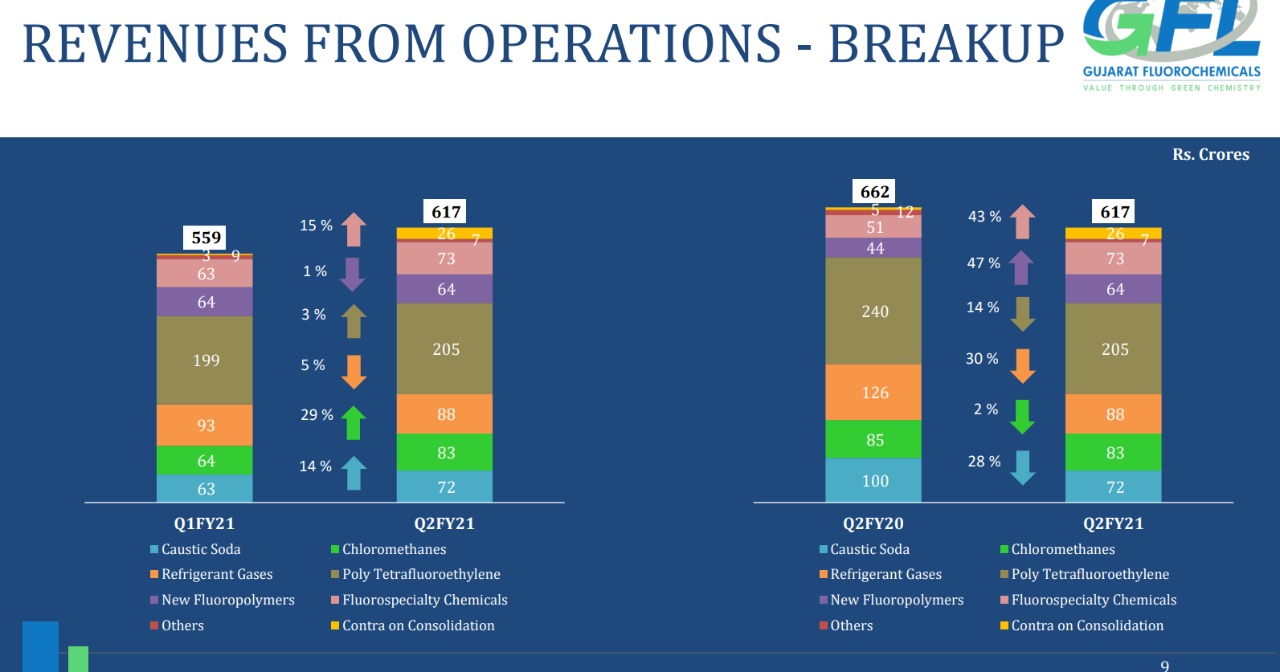

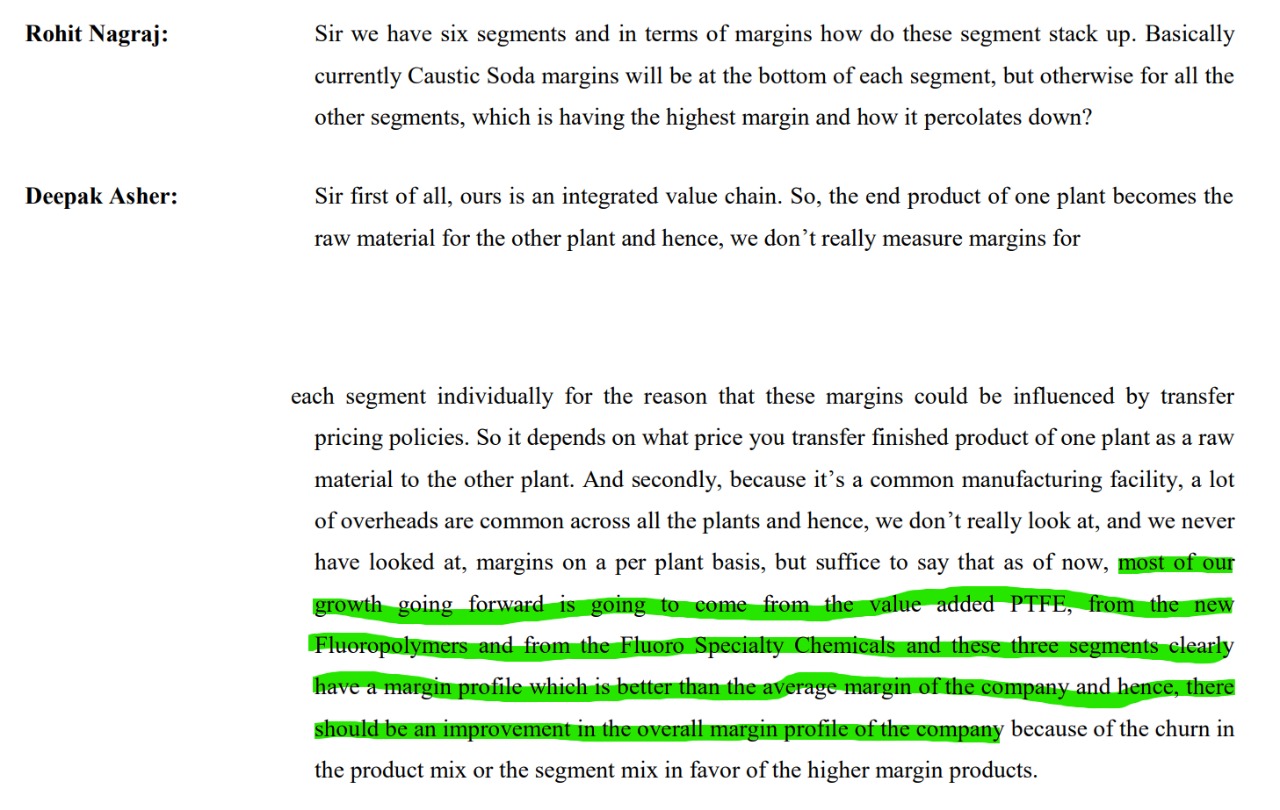

This is where management was saying most of the contribution will come from value-added PTFE, fluoropolymers and fluorospecialty chemicals

A lot of contribution seems to come from auto so a near-term upcycle in auto can contribute to better numbers in fluoropolymers (wire sheathing, dashboard plastics, gaskets, o-ring)

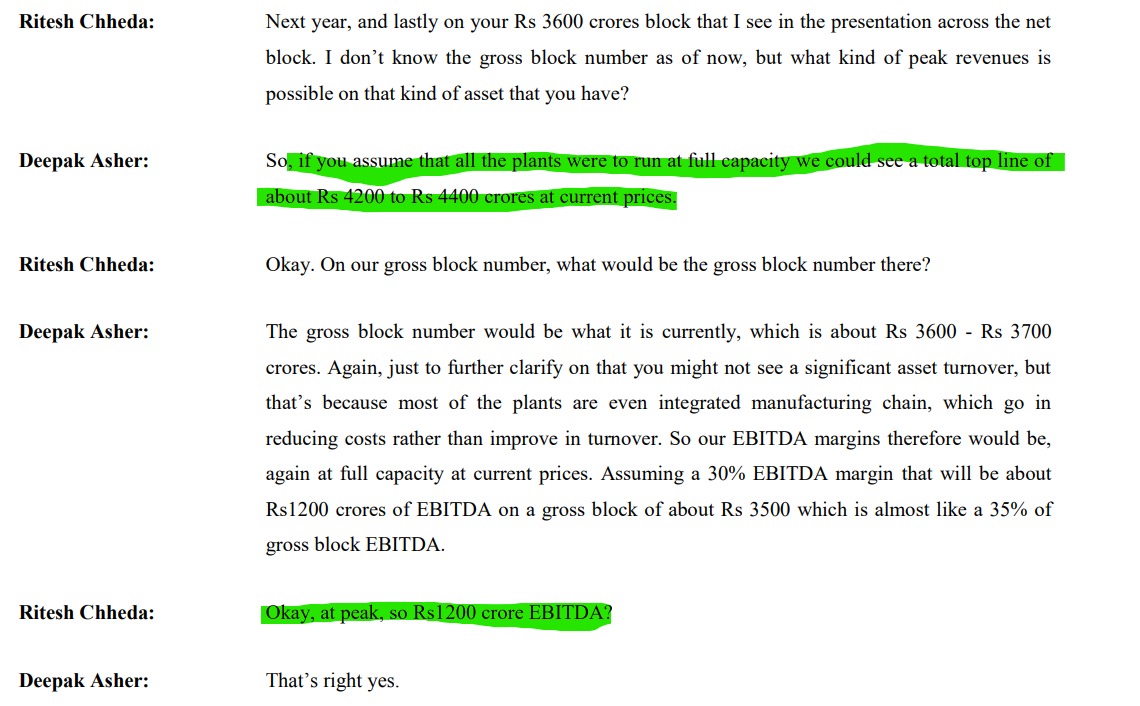

Current capacity can contribute to an EBITDA of 1200 Cr

This was the interesting part where there was a sort of a guidance on fluoropolymers (170 Cr to 700 Cr) and fluorospecialty chemicals (180 to 600 Cr) - Almost four-fold and three-fold increase

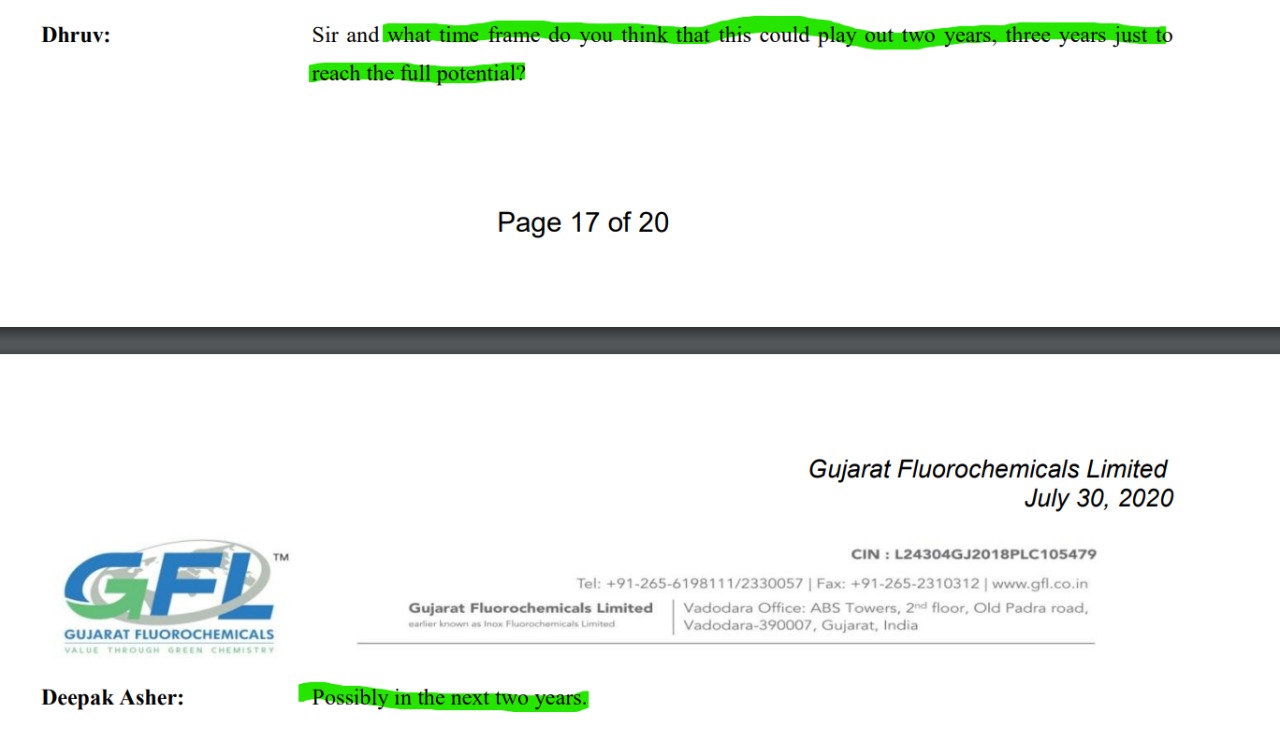

In a timeframe of 2 years

This could be a China+1 play. Management could also be looking at non-Fluorine chemistry for future growth.

Another interesting part in the above was the efficacy of fluorinated molecules in drug delivery. I checked this and there were couple of research articles on nature here and here. The latter especially speaks about trifluoromethylation (-CF3) and the complications in creating such molecules. There are several such molecules in the EC filing, so the company seems to have a strong R&D capability.

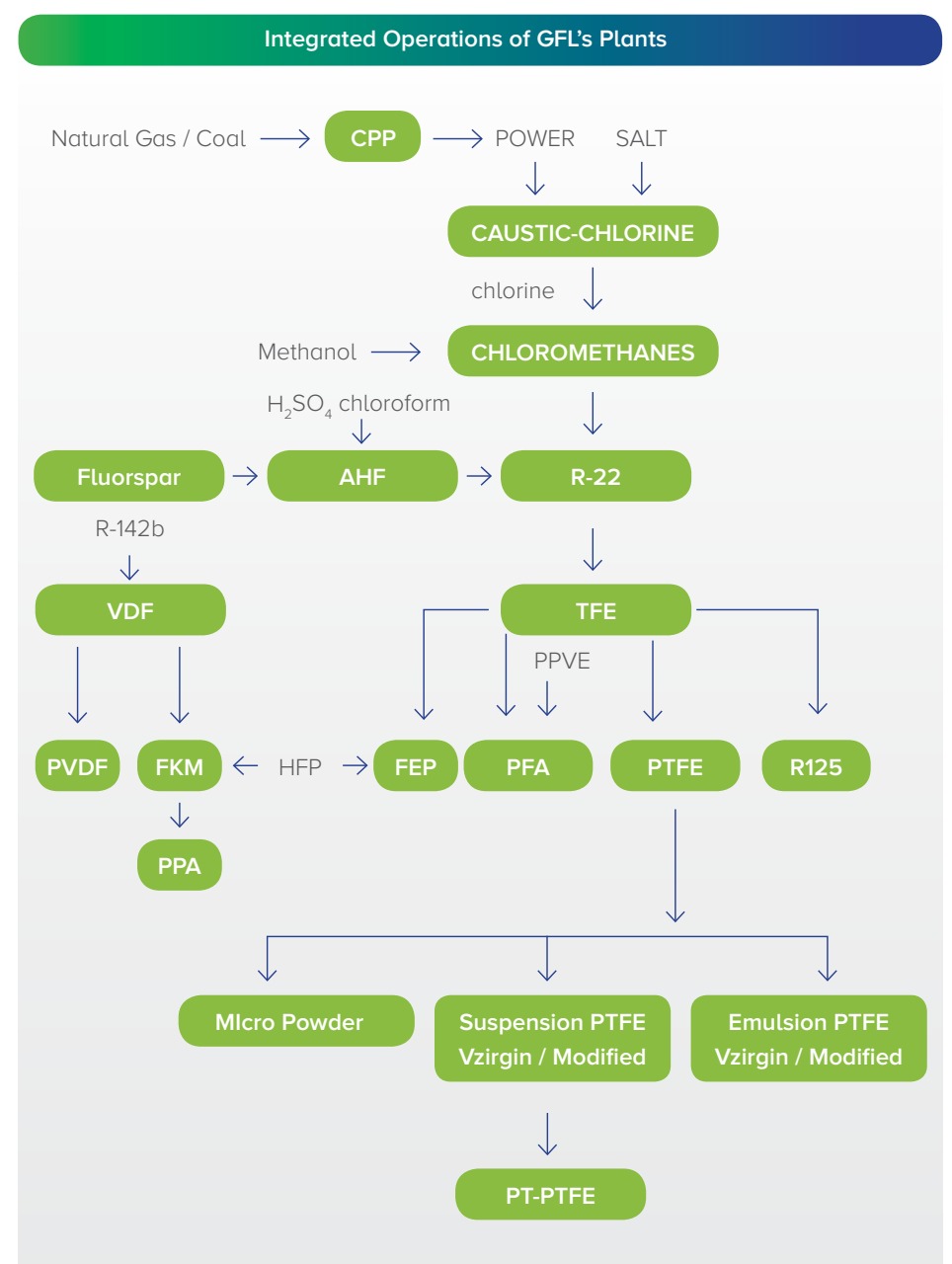

This is a true blue specialty chem company, taking basic RMs like fluorspar (from captive mine in Morocco), coal & gas for power, sulphuric acid, methanol and common salt and producing multi-step chemistry value-added products and intermediates.

Posting these here since the VP thread is for Collaborators only. Apologies as the technical analysis in this post is perhaps too little.

Disc: Have positions around 1200 after reading the VP thread and doing some own research

41 Likes

That thread has been opened for public.

Novartis monthly chart shows a breakout after a major consolidation for 20+ years. This level was last seen in 2000.

6 Likes

Daily chart of Jubilant foodworks with price making highs and volume making new lows. Margins are at peak levels. PE is 177. No explanation needed.

7 Likes

Chart # 5 - HimatSingka Seide

CMP 202 can achieve near term targert of 240 (50% retracement from 2018 highs)

Price broke channel resistance, 200 weekly MA and also crossed 38.2% fibonacci levels.

Company have completed major capex in last 2-3 years.

The management, according to concall, is going to focus on destressing the balance sheet and increasing capcity utilizations across all segments. Have already repaid ~250Crores debt in FY21. Terry towels capacity utilization continues to rise QoQ.

Update on previous chart - Jyothy Labs achieved mentioned target of 182.

3 Likes

1 Like

can the experienced board members clarify is this cup and handle break out in icici bank?? and the chart structure looks very bullish as per my understanding. reqeust the senior members comments.

disclosure: invested from lower levels

Thanks and regards

Yes, Its a nice cup and handle formation

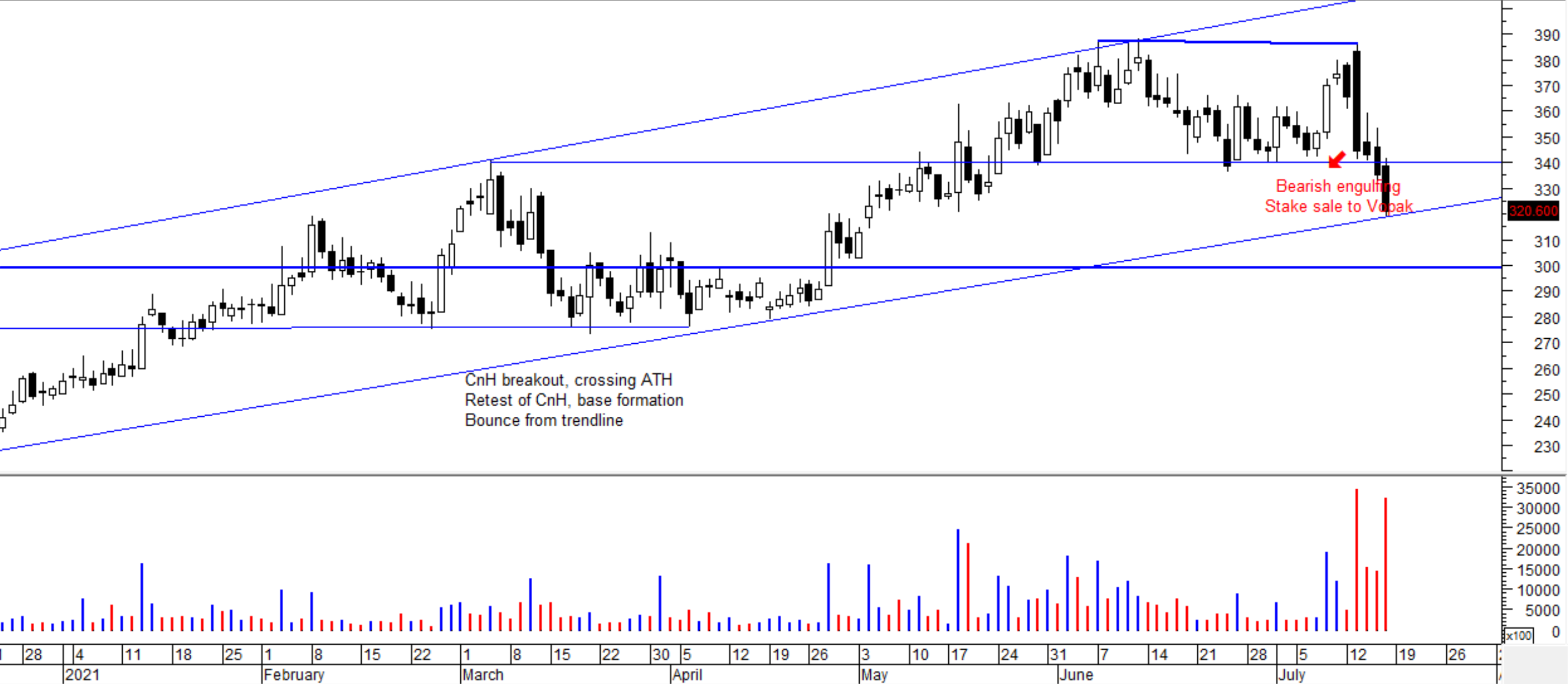

Update on Aegis Logistics. Below are the weekly and daily charts. The company’s announcement of JV with Vopak was not taken well by the markets. The price formed bearish engulfing candle with high volumes and is now at the lower end of the channel. The Vopak announcement seems strategically positive, but it appears that the deal valuations are not good. The company was expected to report acceleration in its earnings and deal valuations dont capture that.

Discl: Reduced my exposure.

8 Likes

This has broken out with good volumes on the weekly.

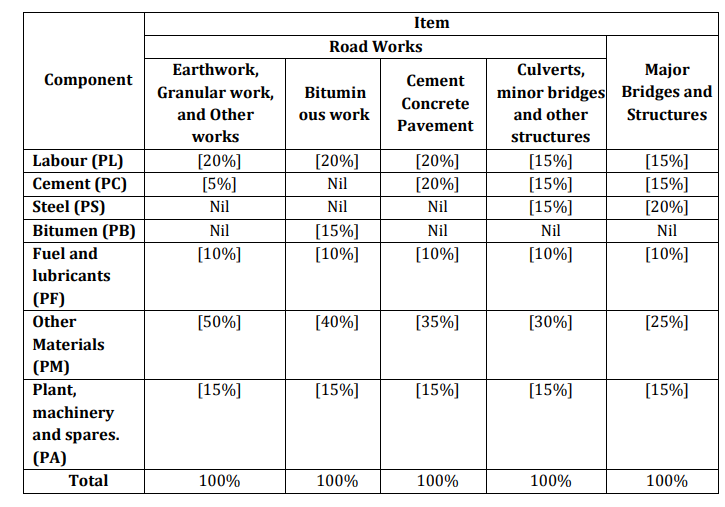

The business is most likely not affected by the lockdown going by this

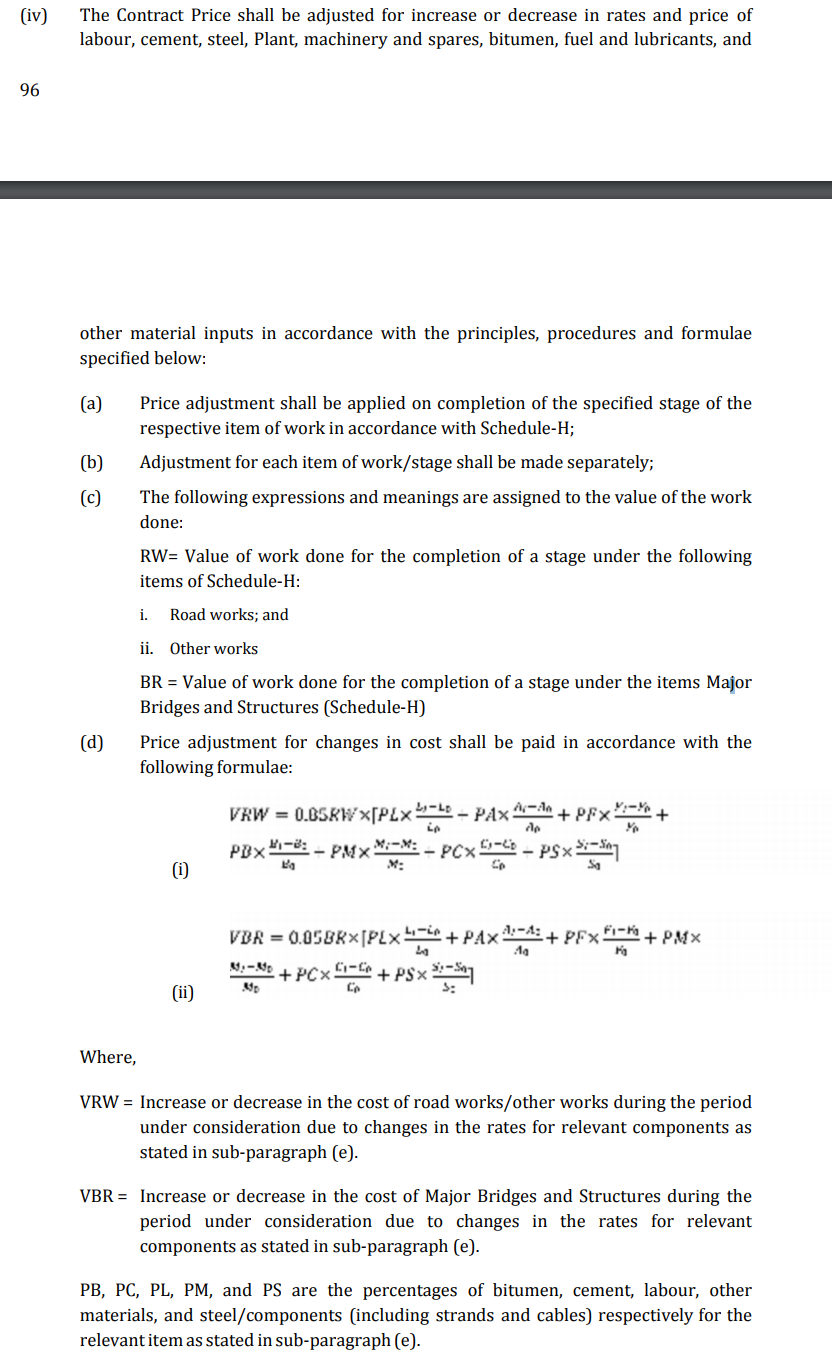

Also the margin risk due to commodity price inflation I was worried about in the last post is most likely immaterial because there are well-defined clauses for escalation based on inflation of commodity prices

And this cost itself will vary based on roads vs flyovers etc. So the business should be covered for inflation on Cement, Steel, Bitumen and even on labour

Credit to @saintsat for figuring this out the cost escalations

On the SHP front, looks like MFs have increased stake and are now close to 33% while retail is only about 6%. It seems to be widely held across lot of reputed MFs

There doesn’t seem to be a fundamental thread for KNR so adding this info here.

Disc: Invested

15 Likes

This sector is also gaining lot of tailwinds due to the thrust of the government and the ministry as a whole.

With a lot of liquidity access this becomes a nice sink for the government to spend on

With an aim of building 60000kms of road by 2024.

Recent address by the Minister on “Road Development in India”

One can watch the above video  to gauge how the govt envisions road infra in the country

to gauge how the govt envisions road infra in the country

The minister also hughlights how the govt believes that a rupee spent on road infra adds 2.5 to the economy.

KNR seems well poised to reap the benefits of this govt spending.

Disclosure : Long term holding

5 Likes

USHA Martin: repeating 2007 pattern, broken from 47-55 range with volume…

On fundamental front, Promoter issues resolved as one brother out now. Sold loss making Steel biz and focusing on high margin customized wire ropes, reduced debt significantly…

revival of infra/capex can be +ve for company…

2 Likes

They make 10-15k Ebitda per tonne vs 3500-4000 for converters like App Apollo. Only problem here is the 400crore+ contingent liabilities. Can be a good proxy for Infra/capex revival in Oil and gas& wider economy. They have tied up with Tata steel till FY24 for RM sourcing and sold off their plant too which caused the pain in last cycle as they backwards integrated for making steel. These steel wires need to be customised for the end customer. Very few companies globally and they have the largest single manufacturing facility for this in the world.

2 key triggers to watch out:

-

Any dividend announcement will be a catalyst after 8 years.

-

Completely deleveraging by the end of this fiscal.

Current markets are very efficient in discounting, could be an interesting play.

Disclosure: Tracking the developments closely. Coming out of a long slumber. This business can do do 15-20% Roce+ and value added mix might improve.

7 Likes

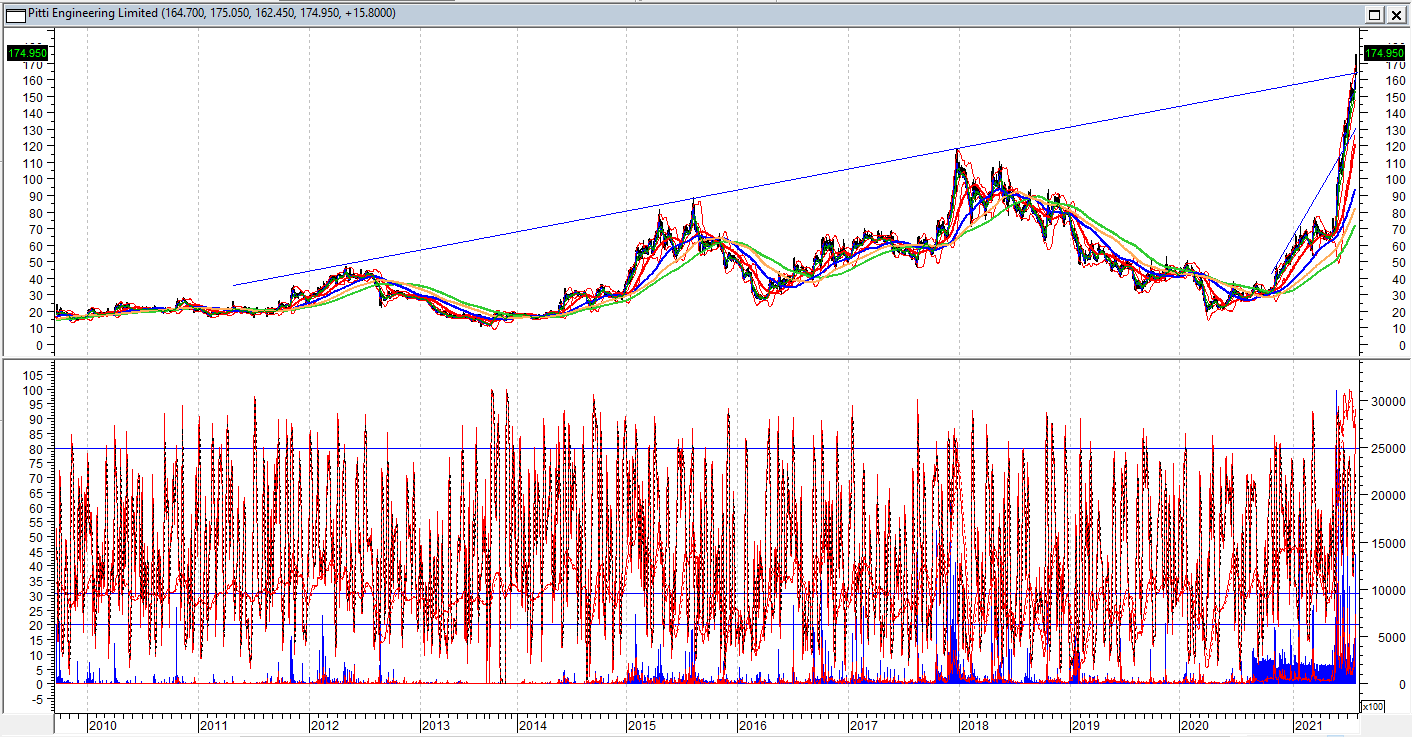

Pitti Engineering Limited breaks a decade long trendline with heavy volume

Over three decade old company is in the field of electrical motors, producing Sheet Metal, Die-cast Rotors & Assemblies, Stator Core Assemblies, Fabricated Machined Components, Pole Assemblies, and Machined Components for varied industries. It has international presence. Presently it is looking for expansion.

Today the prices have broken upward a decade long trendline with heavy volume.

Disclosure: invested at lower levels.

What indicator is that red & green line??

Double bottom breakout happens when the stock moves above the peak between the two bottoms. This chart is misleading.

9 Likes