GNFC, Monthly - Has been on an uptrend after breaking out of 3 year downtrend and consolidation for 6 months.

Daily RSI is at support and probably good entry for getting on the uptrend.

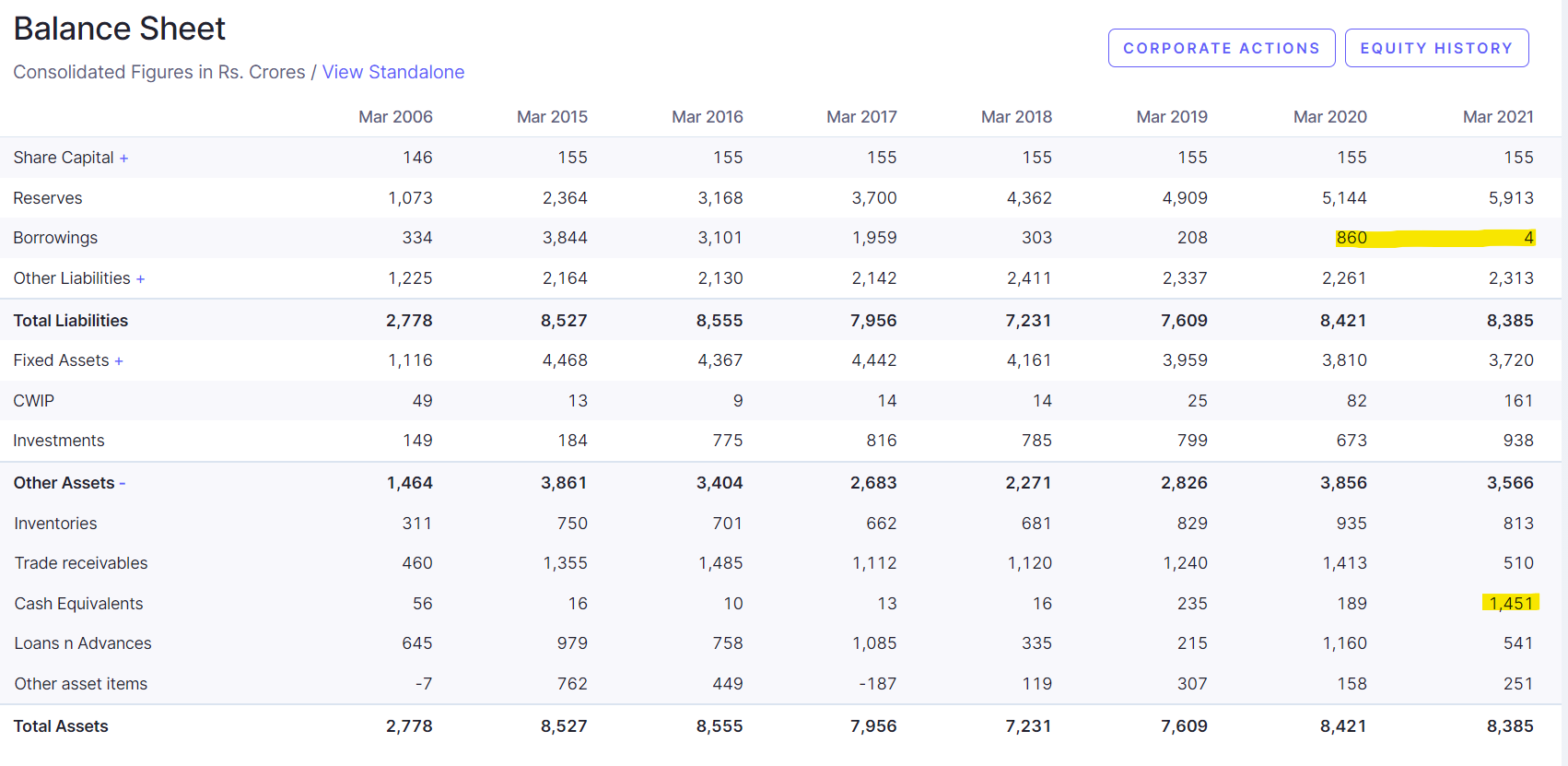

Fundamentally it appears to be at good value at 8x earnings (8 P/E) and below book value. With a market cap of 5700 Cr., the business has cash of 1450 Cr in its book making the EV around 4250 Cr (Trading around 4x EV/EBITDA). This is another business which is valued like a fertilizer company like Deepak Fertilizer when its deriving bulk of its numbers from Chemicals business. Nearly 70% of the revenues come from Chemicals (Acetic Acid, Aniline, Nitric Acid, Ammonium Nitrate, Formic acid etc.) and almost all its bottomline as the fertilizer business is barely breakeven.

Considerable improvement in the balance sheet, now becoming a debt-free company, with surplus cash to the tune of 1450 Cr.

OCF for FY21 is nearly 50% of its EV

Excellent improvement in Debtor days as the govt. cleared a lot of subsidies (1722 Cr subsidy payment to GNFC at one go last year) and is showing intent of doing so going ahead

The business is also embarking on a Capex plan in the chemicals space to expand its chemicals business (Ammonia, Ammonium Nitrate, Nitric Acid).

GNFC is a market leader in TDI (Toluene diisocyanate) and nearly 1000 Cr of revenues come from TDI. Also, govt. recently announced a anti-dumping duty on TDI which too augurs well for the business.

This appears to be a deep value investment on the surface with good improvement in cash flows, better balance sheet, capex plans and a good business outlook with chart on an uptrend as well.

Risks: This is still a commodity business run and a PSU. So may stay cheap forever.

Disc: Invested around current levels