Thanks @Meetkatrodiya . This doc is a treasure trove of information and helps a lot with the calculations and also understanding.

This post is going to be very information heavy, so let me put out the basic objectives first so its clear what I am going to be getting at.

- Unit economics

- Value addition across the value chain

- Capacity calculations by patient for BA and Intermediate (Revised from earlier)

- AHA guidelines

The reaction is in 4 stages as per the EC (page 2.45). I am attaching a labeled version here

One key thing that stood out for me is how the structure of intermediate resembles Bempedoic Acid - so intuition told me bulk of the value add is here where the basic carbon backbone is built (Stage 2)

Stage 3 appears to be a simpler reaction while Stage 4 is just purification with no Chemical changes. BlueJet has presence till Stage 2 only.

Also the molecular weights are interesting here - TosMIC M. Wt is 195.24, while the intermediate is 398.59 (or theoretically 1 kg of TosMIC can give 2 kgs of Intermediate) - of course its not produced out of thin air but rest of the weight comes from other components in the equation, like n-Heptane (primarily the Stage 1 which is produced in-house by BJ).

Ignoring Solvent and other basic chemicals, bulk of the cost comes from TosMIC here.

TosMIC is $130/kg. BJ sells intermediate for $450. Neuland sells BA API for $950. On the surface it looks like huge value addition from $450 to $900 (Stage-3 and Stage-4) but a closer look at the Mol Wt. shows Intermediate is 398.59 but BA is 344.49 which means the max conversion ratio we can expect is 86% (or 1kg of Intermediate can produce 0.86 kg of BA which means to produce 1 kg of BA, you need 1.16 kg of Intermediate. We were working with 1.3 as the conversion factor earlier which is a reasonable assumption)

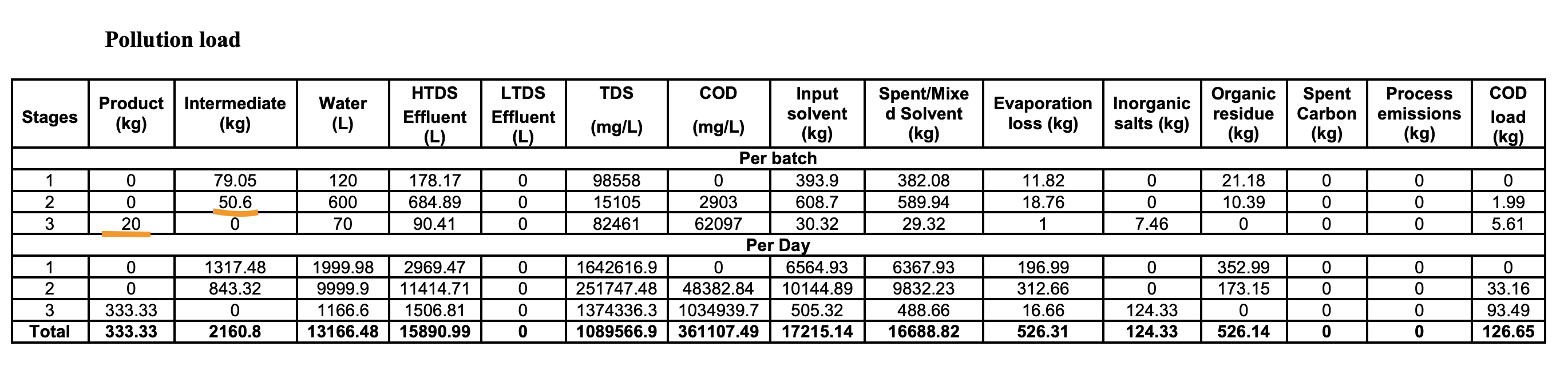

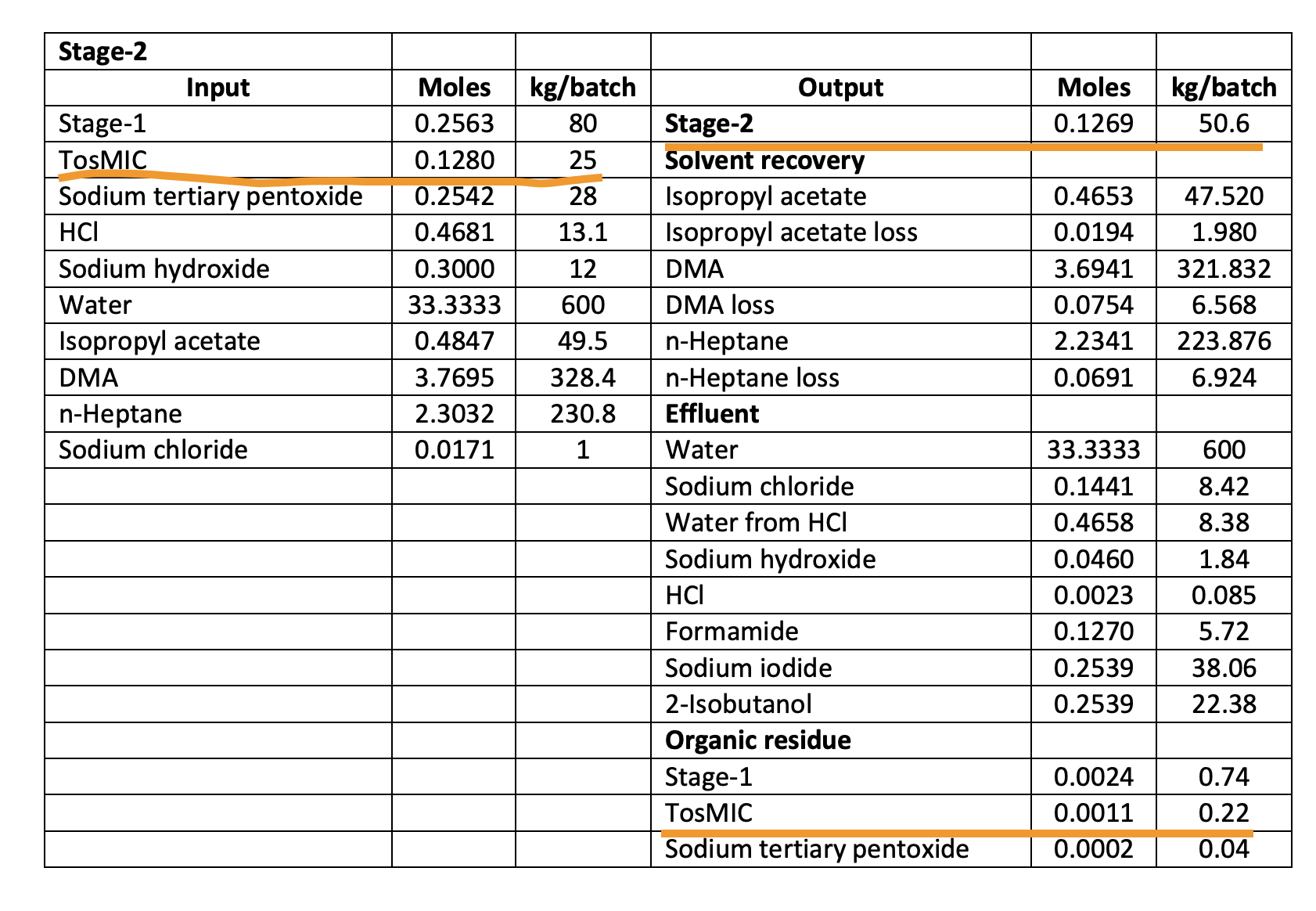

But, the EC also shows something else interesting - it says 50 kg of Intermediate from Stage 2 produces 20 kg of product per batch. This implies a conversion ratio of just 40% which implies that it takes 2.5 kg of intermediate for 1 kg of bempedoic acid unlike our earlier assumption of 1.3 (This tells us our earlier assumptions of patients was way off which we will revisit in a bit). Also notice that per batch produces just 20 kg of products and to produce 333 kg/day, 16-17 batches have to be run (maybe 30 mins per batch?)

The Stage-2 conversion into BA is actually more like 50% (40 kg/batch of intermediate produces 20 kg/batch of product). A whole lot of intermediate that BlueJet makes is lost in the process of producing BA as “Organic Residue”

The natural question that arises is if this is reusable. This doesn’t seem to be the case as Organic Residue here is marked as Solid Waste.

So we can safely, conservatively assume 2kg of BlueJet intermediate makes 1kg of BA API.

Now lets address the question of value addition in Stage-3. If it takes 2kg of Intermediate - that adds up to $450x2 = $900 of Intermediate to produce $950 of BA API which on the surface makes no sense but if you think about it, Neuland is backward integrated and so can produce BA API for somewhat cheaper and we are comparing it with shipped cost of Intermediate by BlueJet. Piramal Pharma buys BA API from Esperion for a whopping $1300 - this is because of the above intermediate cost of $900 that goes into it.

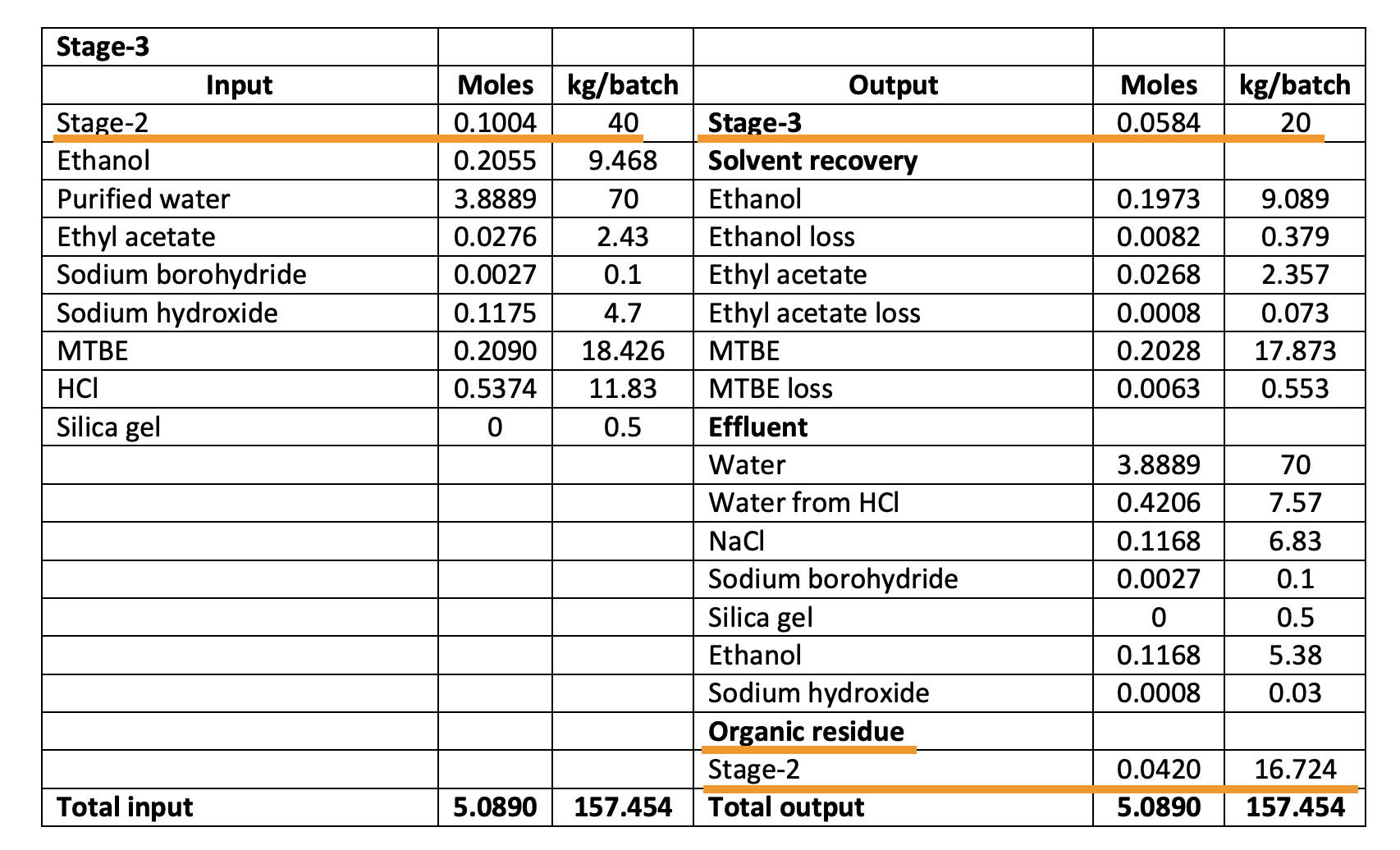

Now let’s look at value addition in Stage-2 which I was guessing was the big money step. The Mol Wt. of TosMIC and Intermediate told us there’s a possibility of 1kg of TosMIC ($130) yielding 2kg of Intermediate (2x$450 = $900). What’s it like in reality as per Neuland’s EC?

25 kg of TosMIC produces 50.6 kg of Intermediate! This is a super-efficient step and you can see TosMIC lost as organic residue is very, very small. So the conclusion is clearly that BlueJet captures almost all the value with the intermediate production.

What does this do to our patients per MTPA calculations? It remains same for BA API at 15,220 patients/MT as earlier. But at 50% conversion, it reduces it to 7600 patients/MT for intermediate and to 6000 patients/MT at 40% conversion ratio (which the first table seems to imply when it says 50kg of intermediate produces 20kg of BA). This would put the 180 MTPA capacity of BlueJet at roughly 1M patients (6000 x 180 MTPA) because this can effectively cater to a BA API capacity of only 72 MTPA (0.4 x 180 MTPA).

Continuing with the unit economics, we know from Esperion’s sales that the revenue for US per patient/month works out to $55 (Take Sept '24 - $31.1m for 190k patients per quarter works out to $163 for 3 months or $55/patient per month). We know 1 MT of BA API caters to 15,220 patients - that’s $950x1000 worth of API per year - so per month it works out to $5.2 per patient per month. So ESPR markup is roughly 10x on the API which is understandable since they are the innovator. This also tells us there’s no point for them to squeeze BlueJet or Neuland as their cost in API is just 10%. The retail price of this without insurance goes up to $500 - another 10x markup! No wonder there are discounts available to buy at $220 or so online in the US without insurance. With insurance, it seems to work out to around $35 or so per month.

In India (there’s no patent here, so generics are available), the tablets sell for Rs. 240 for 10, so its roughly $9 for a month. The amount of API in this, assuming they follow the same stringent manufacturing standards remains at $5.20, so there’s still a good margin for the generic guys. It is fascinating to see how overvalued meds are in the US when you work out unit economics this way (Even if there’s a crackdown by RFK, this base price of API should remain protected as its such a small part of the price to customer)

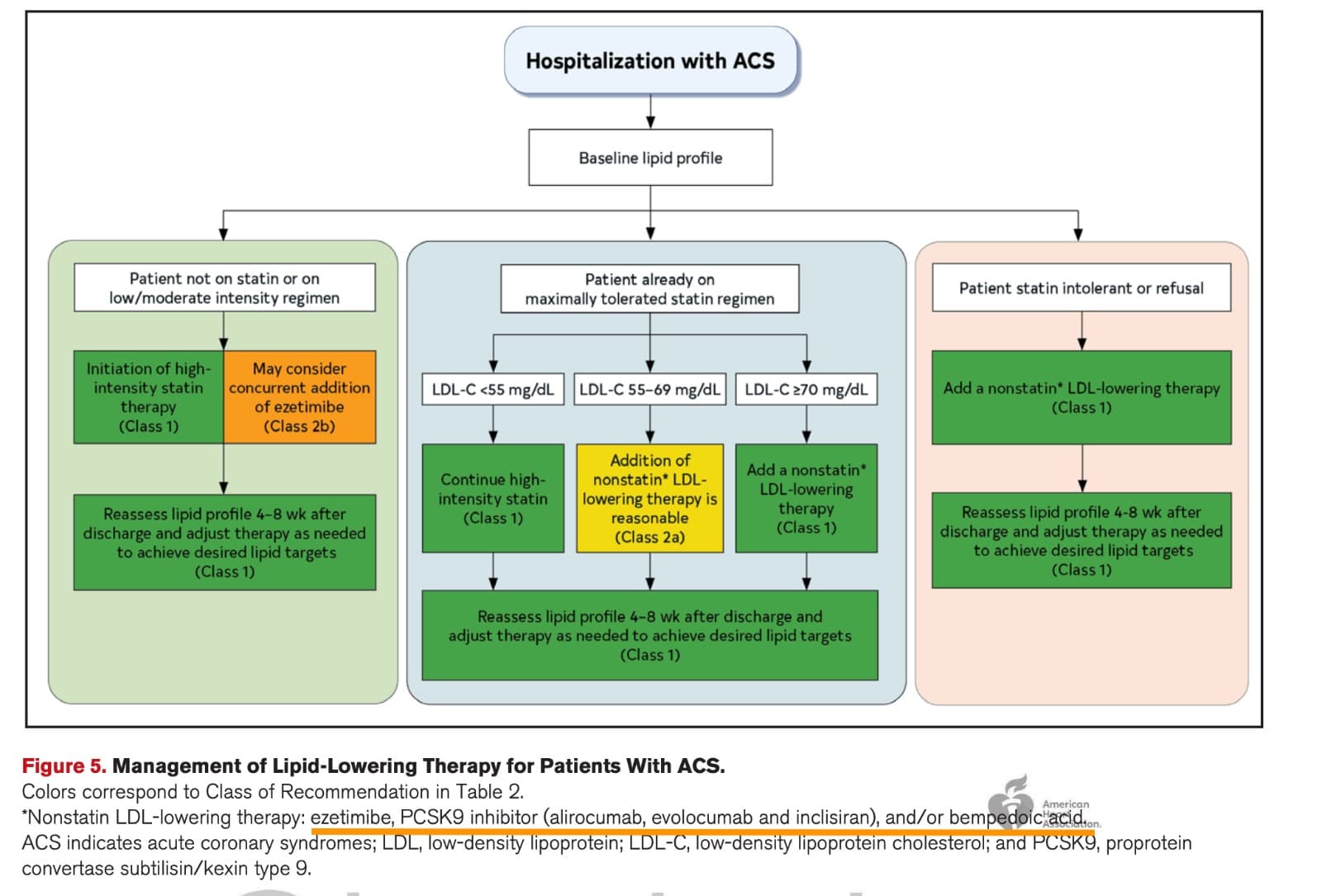

There’s another interesting development that has happened last week. The American Heart Association has finally revised its guidelines for ACS after 6 years.

2025 Guideline for the Management of Patients With Acute Coronary Syndromes.pdf (1.4 MB)

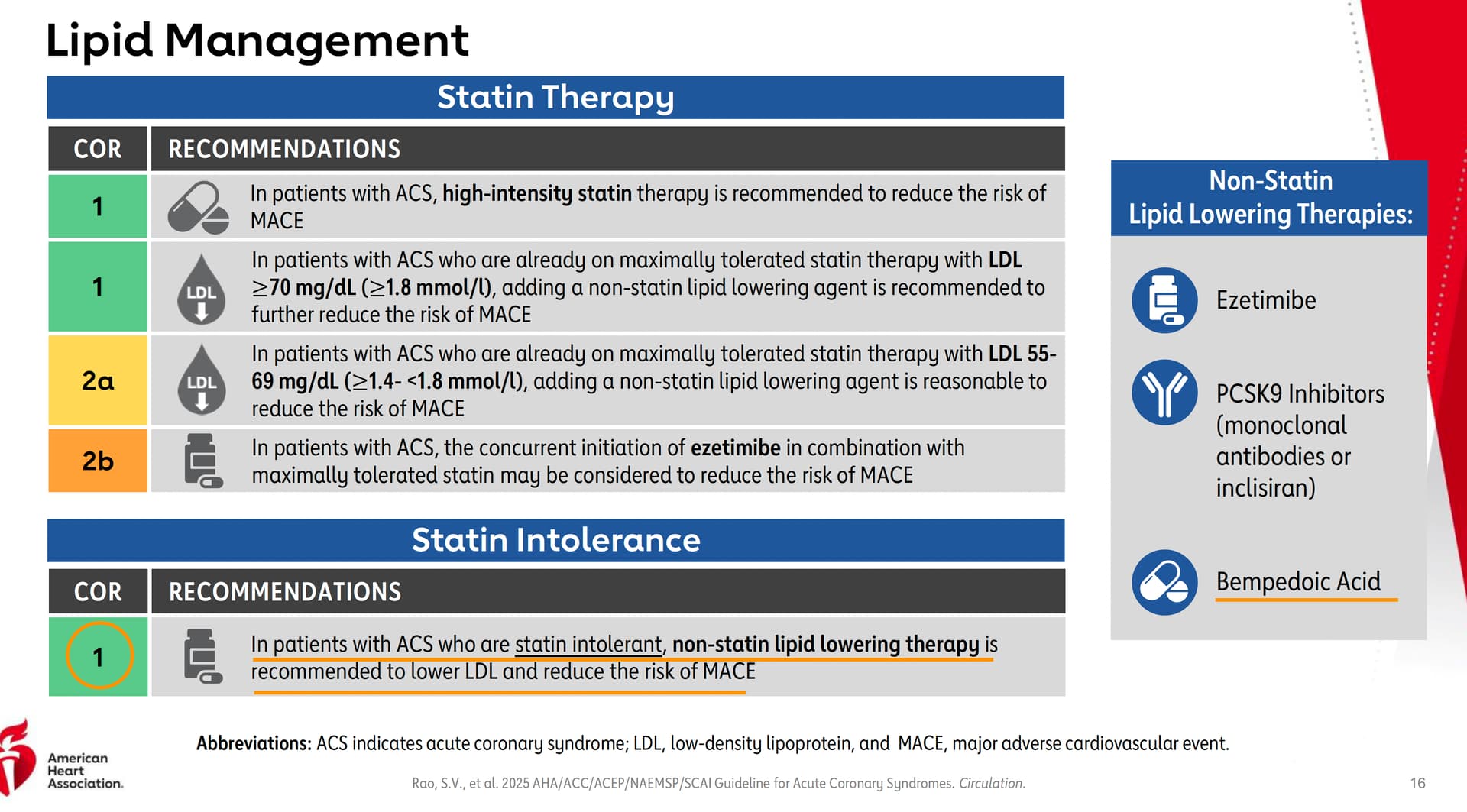

It has recommended Bempedoic Acid as part of the non-statin treatments.

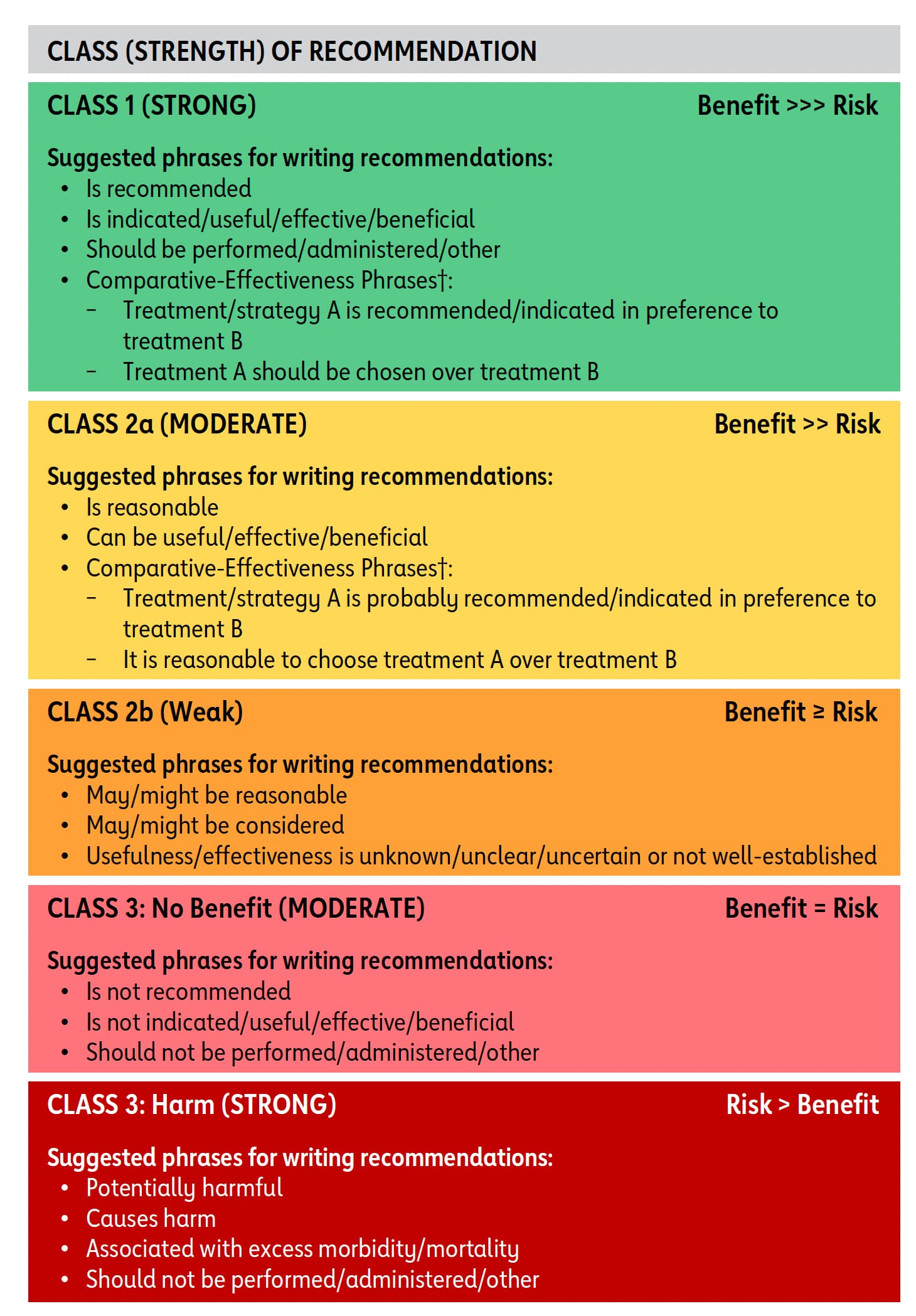

Class-I implies that Benefits far outweigh Risk

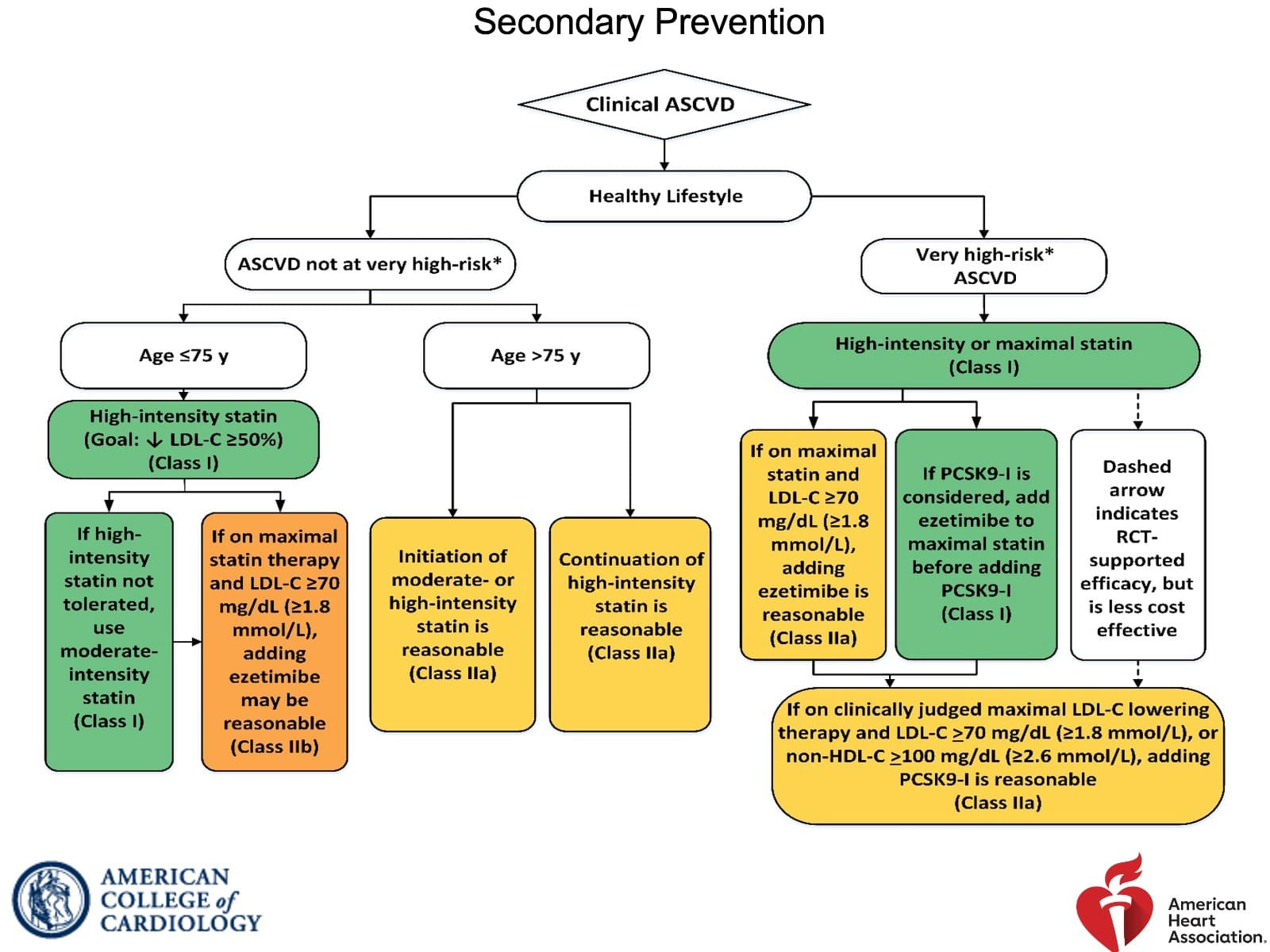

To put it in perspective, this is guideline from 2018. Back then there was no category for statin-intolerant or statin refusal (this seems more common now as people see negative reviews for statins online which is in stage-3 of Seige cycle). Also note how only PCSK9 is Class-I for already on maximally tolerated statin but needs further reduction category

Guideline from 2025. The last box for statin intolerant or refusal is new and the recommendation is Class-I directly! Also note how the maximally tolerated has changed from just PCSK9 in green to whole Non-statin therapy as Class-I

PCSK9 is not covered by insurance, so there’s good chance for Nexlizet/Nexletol being preferred options here. Also notice the and/or in the footnote, which implies the Ezetimibe+BA combination can be recommended as well.

This has more potential than the label expansion from last year to accelerate sales, as it can become a pull product (doctors go by the AHA guidelines) than a push product (solely MR driven).

It feels almost like a crime to be bullish on anything in current market conditions, but working on fundamentals is essential to maintain sanity.

Disc: Invested in BlueJet and have recent buy transactions