To make glass, gas is important, it is chicken and egg situation.

5 Likes

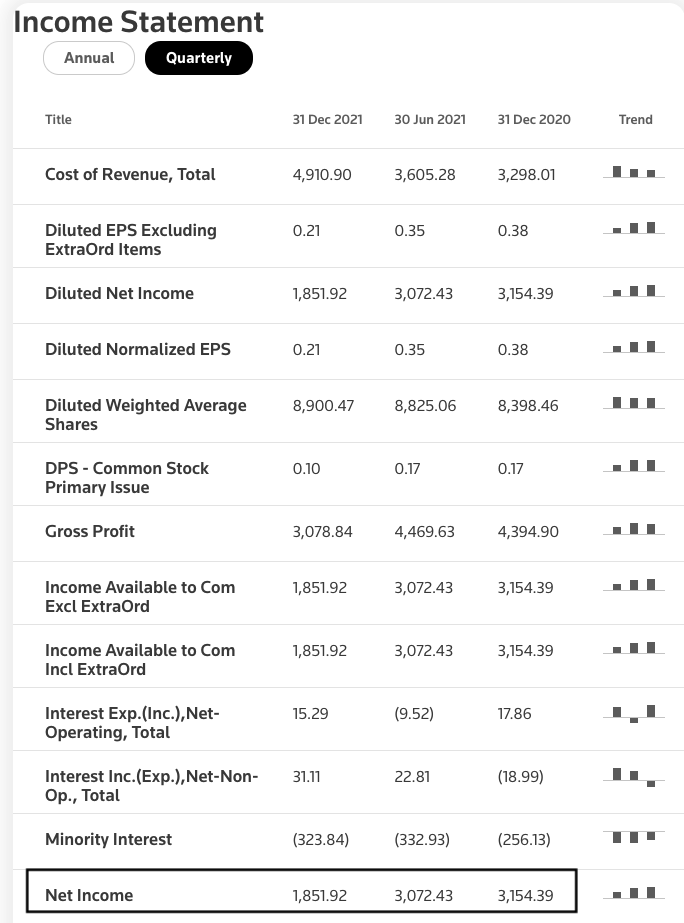

Xinyi : Net income was already down by 39.73% from H-1 to H-2 in last year due to 2 reasons :

- Rise in input and fuel costs

- Decline in solar glass prices

November to February (these 4 months) were the best for all the solar glass producers due to significant supply demand mismatch and China was fairly aggressive in adding solar capacities. No company might be able to record those numbers again (unless if there is any big supply demand mismatch which seems unlikely).

Now as far borosil renewables is concerned - we should not forget that there were no duties on glass imported from Malaysia (same time last year) but sea freight rates were high and now stabilising.

Impact might not be as much as we anticipate due to decline in prices - it would be because of higher rm and fuel prices. I am expecting margins (ebitda) to stay in 28-33% range as guided by the management.

Awaiting more details on Interfloat acquisition.

D - Invested.

9 Likes

No of updates

- 674 is price point for equity allocation in interfloat deal - fair to investors

- Production go live delayed to Oct 22, some cost escalation as well

- Final 1100 TPD merged as one project - cost revised upwards but supposedly Production will be higher as well

3 Likes

68.09% of the German entities bought by issuing 26.63 lacs of shares(@674 Rs.) in BR. Existing equity is approx. 13 crores so dilution is 2% or so. Rest is to be paid in cash…so that should be less than 90 crores .

EDIT: The share issuance is for Interfloat only. So 245 Crores in cash to be paid for the rest of Interfloat and entirety of GMB . Thanks @Amudha for pointing it out .

SG5 is scrapped and SG4 is to be double in capacity, so basically they are expanding at one go rather than in two stages.

SG3 is delayed for couple of months and will cost 688 crores instead of initial estimation of 600 crores “as a result of multiple factors including

rupee depreciation, exceptional increase in the prices of Commodities, electronic

products and ocean freight rates”

I have not much prior experience of studying mergers but compared to the GMM Pfaudler deal, this one looks much better .

Disc : Invested & staying put

2 Likes

Yesterday’s announcement mentions only the Interfloat corporation. The announcement in May, talked about acquisition of Interfloat and GMB companies for a consideration of 425 cr. through stock and cash. So other than the 26.63 lacs shares (@674 Rs) another 245Cr (80cr for Interfloat and 165cr for GMB) will have be paid either through stock or cash.

2 Likes

I have the same question. What happens after 300GW solar capacity is reached?

At PE~50x, the profits from SG3 and even some part of SG4 seems to be already priced in.

A large portion of the valuation of a business comes from its terminal value.

When the terminal value is in question, such high PE cannot sustain in my view.

I have invested a small portion (3% of portfolio) in BR.

It can at best go another 2x probably.

2 Likes

I have been trying to wrap my head around following questions. Feel free to add your inputs or correct mine.

Q1. Is demand really taken care of? What is the impact of aggressive chinese capacity expansion in recent years?

Q2. What are the most important variables for stock re-rating?

Acc to Mercom, Solar installed capacity can reach 3000 GW or 3 TW by 2030

link: Global Installed Solar Capacity Could Reach 3,000 GW by 2030: Report - Mercom India

World is currently at ~1000 GW.

This equates to roughly 3000-1000 =2000 GW in 8 years or 250 GW/year on average.

In FY23, 300 GW of renewables capacity is projected to be installed, out of which, ~60% or 180 GW can come from solar.

This implies world needs 200-250 GW of solar glass each year till 2030. The number can increase as we move towards 2030.

Lets look at existing global solar glass capacity now. Since bulk comes from China, lets focus on that.

Acc to PV magzine,

Link: Chinese PV Industry Brief: Solar glass capacity hits 64,000 MT per day – pv magazine International (pv-magazine.com)

China is at 64,000 MT/day out of which 59,000 MT/day is operational. Assuming 1000 TPD = 5 GW, this translates to roughly ~300 GW of existing solar glass supply power with Chinese.

There are some capex being taken worldwide that I am aware of. Couple of companies (non-indian) I came across are:

- Canadian Premium sands - they plan to come up with 4GW worth solar glass capacity by 2025 (phase 1). Attaching their investor presentation

- French company - Alliaverre - plans to make 600 MW. Link: Alliaverre to produce solar glass in France – pv magazine International (pv-magazine.com)

However, since these are minute in scheme of things, can be ignored for now.

Now, if we compare 300 GW of existing capacity with the 200-250 GW needed by 2030, it looks like supply > demand. In a world without duties or china+1 sentiment, china would keep dumping cheap solar glass on the world and local industry will not flourish. But thats not the case as we know.

Implication 1: Solar glass demand (vis-a-vis supply) can only be ignored as a key variable if duties uphold for extended timeframe. Without duties, the current valuation and profitability does not make any sense.

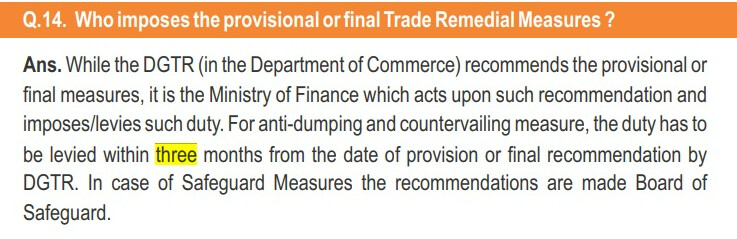

The duty as proposed by DGTR is impressive and applies to all imports (not just china). Has to be seen if it is implemented in full. AR says imports from Vietnam account for 60% imports. Finance ministry generally takes 2-3 months to act on DGTR recommendations (based on 2-3 past data points), which means we should see an announcement by Aug mid (if there is one)

Implication 2: since China only uses 20-25% of its solar glass production for domestic consumption and rest is export oriented, we may see either some of these companies lowering production or closing altogether. Remember there are 300+ solar glass producing companies in China alone. I can only guess that this will lead to solar glass prices going towards normal historical levels (2015-2020) of INR 97-105 / sqm / mm. Factor in commodity inflation, and the new base prices could be higher, no idea how much. But, I have doubts over mgmt. guidance of 30-35% ebitda margins as communicated in Q2 FY22 concall (page 18 of transcript). I say that because BRL was at 35% ebitda margin in Q4 FY22 when avg solar glass realizations were around INR 133 / sqm / mm. Add further inflationary pressure and lower glass prices, and even 30% ebitda margin looks thin. Expecting Q1 to be below 30% given the sky high fuel prices.

So, in short, extended import duty and low cost inflation are paramount for BRL to outperform the expectations baked in the current stock price. My valuation model suggests 35-40% EBITDA margins with 115-130 sqm/mm glass price levels should do the trick. Anything below that and we could be in rough waters.

A third variable (apart from duty extension and cost inflation) is aggressive capacity expansion. But, having seen mgmt delaying capex for SG3 by 2 months and increasing project cost from 600 to 688 cr, this also depends to an extent on level of duty extension and cost inflation in future. Therefore, I see this as an important but secondary variable in the thesis.

Look forward to hearing your views/counterviews.

Disc - invested, biggest position in pf

CPS-2022-MAY-Corporate-Presentation.pdf (1.8 MB)

16 Likes

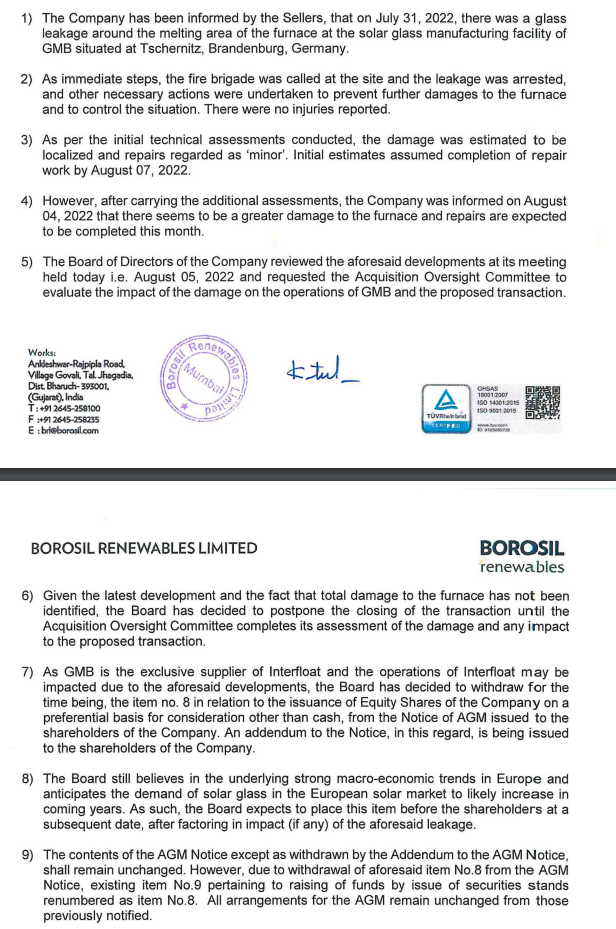

The Board has decided to postpone the closing of the transaction until the Acquisition Oversight Committee completes its assessment of the damage and any impact to the proposed transaction.

7 Likes

I believe this is the best decision in current circumstances. Apart from the damage to the furnace, there are several uncertainties:

- Availability of gas in Germany.

- Gas price in Germany, if available.

- Demand for new solar power projects in Europe, given the recessionary conditions.

The timing of the acquisition, IMO, was totally skewed.

5 Likes

looks like glass prices have come off + some power and fuel cost pressure = impacted margins. if interfloat is a success, then margins can be impacted for some quarters to come and can keep stock under pressure.

Key will be to see if QoQ was there any volume growth.

disc : not invested

While numbers look optically bad on quarterly level (due to high profits of earlier quarters), business is still quite profitable with 18% PAT and growing fast. With doubling of capacity from next quarter (excluding acquisition), company is set to go places. I would be happy if market gets disappointed by the results as it would provide rare opportunity to buy at lower level

Disclosure : Invested for last 3+ years (from Gujarat Borosil days) and strong believer of solar growth story for India

4 Likes

True, results are inline with expectations. Margins look worse but discounting for peak inflation and supposed fall in glass prices, these are decent numbers. Topline holding at ~170cr suggests either glass prices stayed around 132-135 levels or there was better volumes or better product mix. Coming quarters should see re-entry into mgmt guidance zone of 30-35% ebitda with sliding commodities.

However, the elephant in the room is ADD extension. Here’s a clip from a publicly available govt doc on duties.

“Duty has to be levied within three months from the date of provision or final recommendation by DGTR”…

We are 1 week away from that expiry date!!

2 Likes

Since there is no ADD on imports from Vietnam(same chinese producers) , and they have been dumping here already ,how much extra damage can happen if this extension does not take place ?

@Ghonarbochon I have tried to partly answer that in a previous post. To summarize it, my best guess is:

- This will be equivalent to no supply demand gap in the market

- Fall in solar glass prices to little above (adding for inflation) 2015-2020 levels due to flooding by chinese players. I guess anywhere between INR100-120 /sqmm. This in turn, should kill ebitda margins further. With current inflationary pressure on cost and assuming glass price of 110, my calc shows a sub 10% ebitda as against mgmt guidance of 30-35%. In short, it will be catastrophic for the stock price. Imagine the asteroid that destroyed dinosaurs

Inline with whose expectations? Yours? ![]()

Borosil Renewables is an expensive stock. With that kind of result the stock wont hold up.

The India capacity addition has also got delayed from 1qfy23 to 2qfy23 to 3qfy23.

Acquisition of interfloat also looks in doldrums which could be good for them.

If Russia turns off gas to Europe where will Interfloat get gas from. Maybe its a blessing in disguise and they should exit from the deal.

Outside India acquisitions always look good. But usually too many variables are beyond your control.

2 Likes

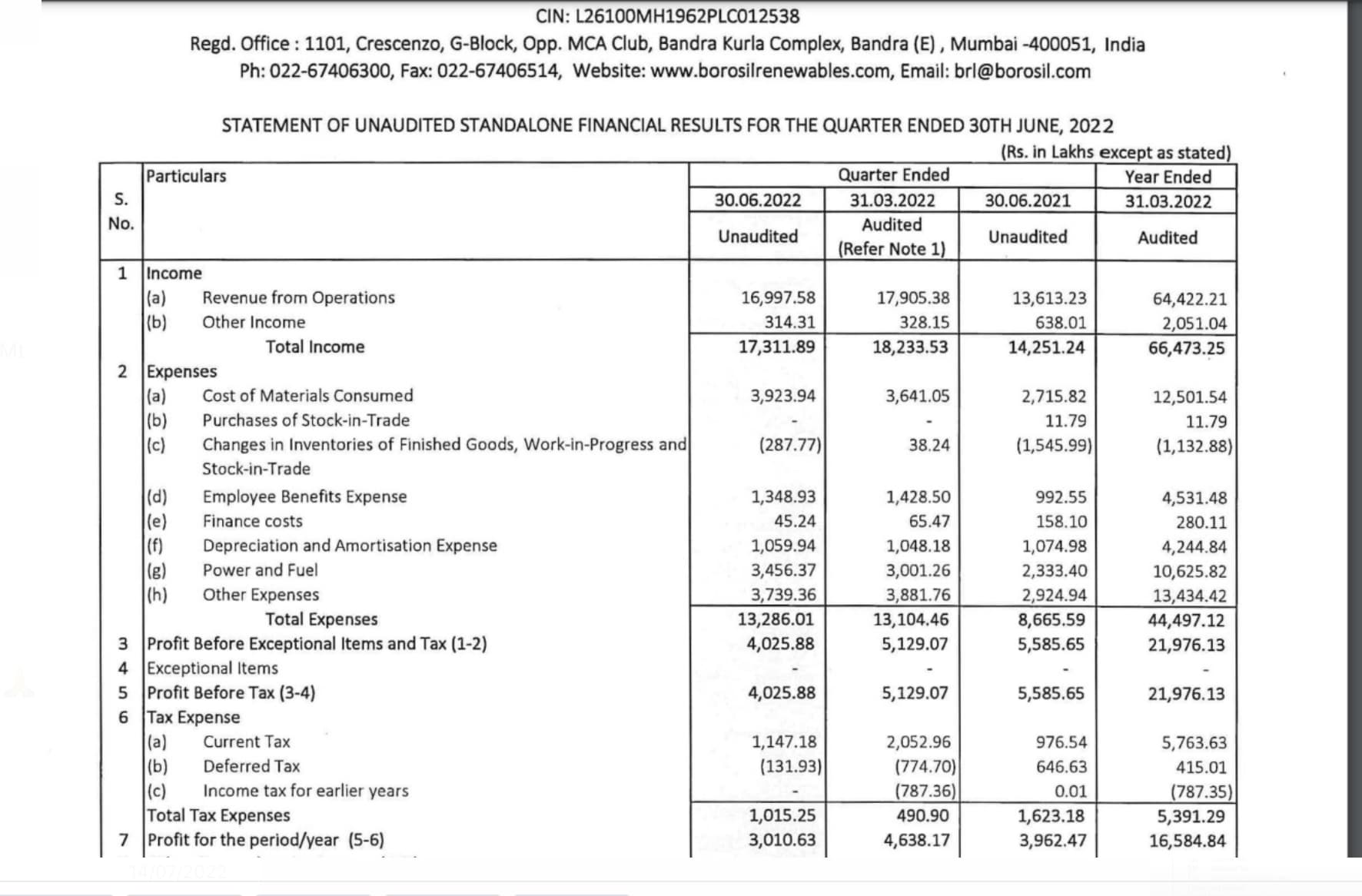

Management was pretty clear in Q3 concall i beleive that agreement with vendors on Soda ash prices would expire in Apr 22 and margins will not be same from next year, hence we could see pretty good numbers in Q3 and 4. With huge spike in soda ash prices + Rise in power n fuel added more pain to bottomline.

Regarding interfloat acquisition it won’t be just Borosil who will get impacted if there is a gas shortage. We are looking at Global company in making now with acquisition abroad. I agree the current valuation has baked in next capex.

Overall i have good conviction on management who has been walking the talk and conservative in guidance so far.

Disc - invested from 200 levels

1 Like

Whether Interfloat will get Gas or not will be depending on the German governments gas rationing and prioritization policy.Since Eurozone has ADD on chinese glass,domestic production is almost the only way for Germany. It depends on how they propose to reduce gas usage …they surely cant do so in the long run by stopping their domestic production .

Also,the BR management has been very conservative all along and are old hands . The aquisition may look risky now but one can be sure that a lot of thought has gone into the decision.

Disc. Invested from below 100 levels

1 Like

GAIL also thinking of entering into solar glass manufacturing

- Subtle hints on better matgins ahead per prevailing input cost scenario, better production than Q1( it had 9% production drop) and glass prices around 140, ofcourse with assumptions. Not to forget operating margin levers with 2.2X capacities in place by Q3.

- ADD cutting too close ( deadline 17th aug) is bound to keep overhang till its done. Risk to watch out for.

Invested

5 Likes