Thanks for inputs. Little disappointed that India capacity expansion got extended by 1 Qtr more. But I feel, this price is good time to accumulate with 1 year view , given BCD and Price hike

Nice update from Mr. Pradeep kheruka of borosil renewables :-

Pradeep Kheruka Of Borosil Renewables Speaks On The Firm's Q4FY22 Results | Bazaar Corporate Radar - YouTube

1 Like

Few other points that were discussed:

-

Solar accelerator program in Europe - similar to aatmanirbhar bharat, focus on local manufacturing - Idea is to go from current 3GW to 8-10GW in medium term. This will propel the need for solar glass, hence the acquisition

-

A key synergy from acquisition - current exports to Europe will start taking place from European subsidiary freeing up capacity for boro renew India to cater to domestic demand, which would bring in higher realizations. Also, supplying locally in Europe will allow for better realizations too since logistics cost will be taken care of. In Europe, costs are higher but prices are also higher, so net net its ok

-

On PLI scheme benefits → module mfgrs who buy glass from borosil renewables will get higher PLI from government since the amount of domestic products used in module making goes up…

-

25%+ of total production is from thinner (2mm, 2.5mm, 2.8mm) glass - will keep improving - higher average realization per sqmm when you go towards thinner glass

-

On anti-dumping duty getting expired in Aug → application has been filled, govt. is analyzing the information and processing it, a disclosure has been issued recently, will need to wait for final call → going in right direction

9 Likes

As per my varied calculations (which includes the Interfloat acquisition and SG-3 commercialization bySsep 2022), EPS for FY2023 comes to be ~Rs. 20 and for FY 2024 ~ Rs. 28.

Would love to hear from you guys if your calculations differ a lot from mine.

(i have not considered Interfloat expansion but included new shares to be issued to Interfloat on completion of acquisition).

1 Like

2600 TPD (Tons per Day) capacity by FY 25 for a company which had capacity of only 180 TPD in FY19, this is HUGE!!! I am quite impressed by measured expansion for past 3 years followed by planned aggressive expansion for next 3 years. This shows company see large growth runway for global solar demand for years to come.

I also love the fact that company is sticking to its core competency and continuing expansion in its area of expertise whereby it can compete on a global scale.

10 Likes

Can some body throw some light on whether technology upgradation in solar energy can render the present module obsolete.

2 Likes

Mr Kheruka’s timing couldn’t have been better on Acquisition, massive budget allocation to renewables as a fall out of Russia conflict

Last 5 qtrs per at 450 tons capacities, ebdita has moved between 50 to 70 cr broadly( barring one exceptional 100 cr+) , one can see potential at 2600 ton India + EU. As long as demand sustained ahead of supply, BR can have good run.

5 Likes

6 Likes

2 Likes

https://www.dgtr.gov.in/sites/default/files/TTG%20NCV.pdf

Sunset review of Anti Dumping duty on imported solar glass from China

7 Likes

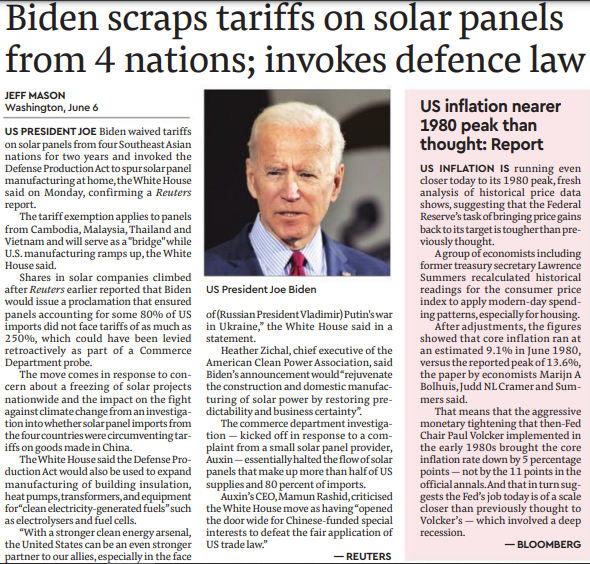

May be now competition to BOROSIL in European markets will reduce as all supplies from competitors will get diverted to USA

5 Likes

Good move.

4 Likes

5 Likes

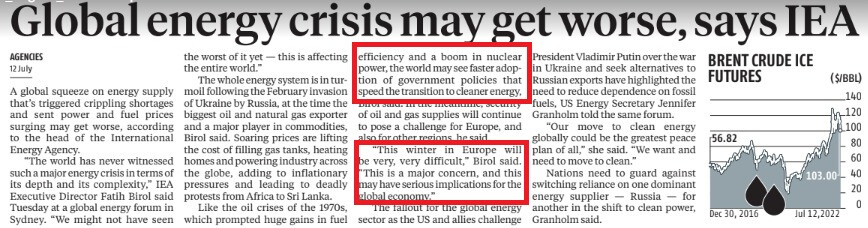

Near term headwinds on acquired entity, situation have worsen over last few days with Russia swithing off gas under maintenance. Under rationing glass industry will be much lower ranks in priorities. Challenge is glass plants need huge amounts of gas, though some electricity (10%) mix is there, Something to keep a close eye on, as well as german govt response of monetary/fiscal support to industry if worst scenario comes true.

Energy crisis response from govt innter s of stimulus for selective industries

European nations are forced to find different innovative methods to manage electricity demand…cash for clunkers program for old appliances like ACs, fridge etc…space to watch…

Not able to read the bloomberg article …but how sure are you that glassworks will be low in priority? As EU has huge antidumping duty on chinese glass,they pay more than international market to consume domstic glass. At a time when they need to find alternative sources for energy(move away from gas) , why would they hobble their solar industry ?? That would be counterproductive for their goal of getting free of the russian gas asap.

1 Like

Some margin pressure highlighted by Xinyi solar

Soda Ash prices continues to remain firm (highlighted even by tata chemical) also glass prices cannot increase continuously if the renewable trend has to continue…

5 Likes

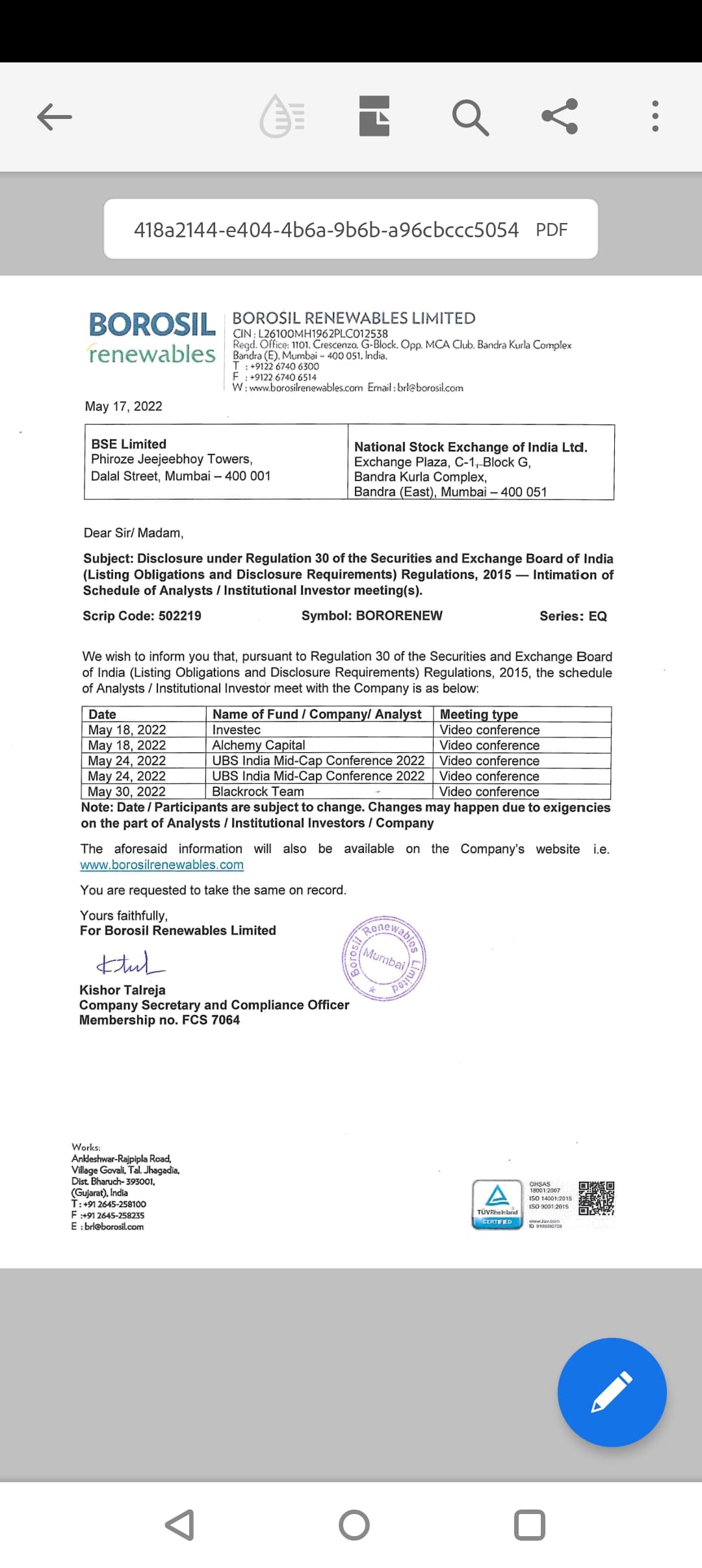

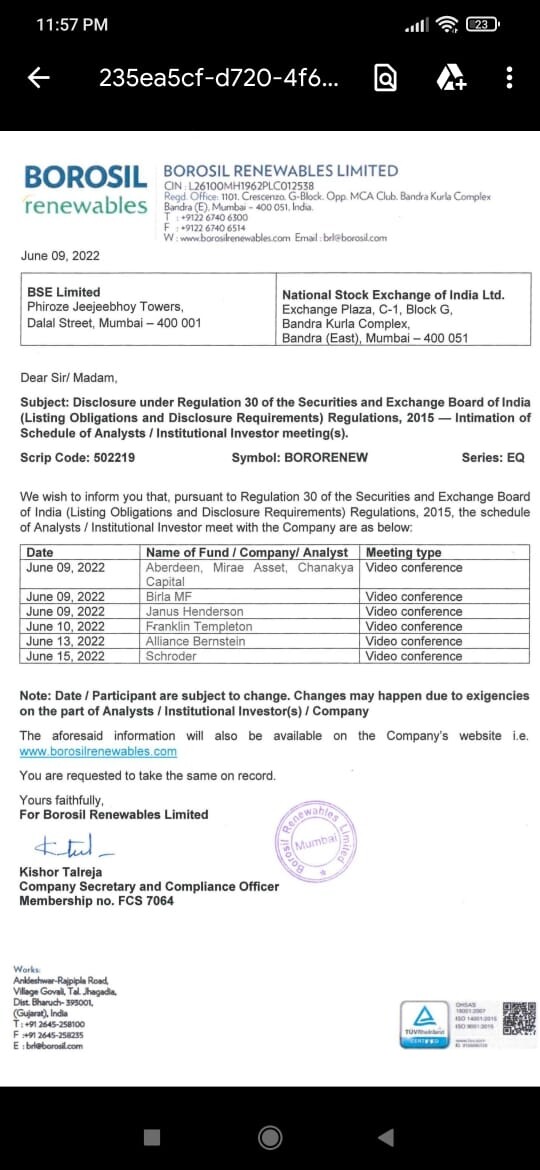

Fund raise board meeting on 14th July

1 Like