IMO Domestic Player entering the industry is good sign. Main concern is Chinese players dumping glasses at cheaper price as Borosil doesn’t have level playing field with them as they have been granted subsidies and Power & fuel (one of the main cost) is cheaper there.

Domestic producer a) won’t have the expertise and b) will face the same high power & fuel charges.

Its good more players entering govt may start providing subsidies and protect domestic market.

That is indeed bad news. Borosil’s margins doubled from 7% in FY17 to 14% in FY18 only post imposition of ADD. I wonder if the ADD not getting extended is the begining of the end. I also wonder why the Government did not extend it even though DGTR recommended an extension. Isn’t RIL and Adani making their own solar glass. If not I wonder if they have influenced the Government to not impose duties to get glass cheaper from China?

You are probably right. These duties get influenced by every member of the supply chain. Currently, stakeholders who benefit from cheaper glass (all cell manufacturers) have a much stronger voice than stakeholders who benefit from costlier glass (Primarily Borosil at this point of time) and this is likely to remain so going forward. Maybe in future as more glass manufacturers come in and Borosil doesn’t remain a monopoly, MoF will take a different view.

Solar glass is essentially a commodity and this is a classic commodity risk playing out. I think the commodity nature of Borosil’s product somewhere got lost amidst the capacity expansion and Europe stories. Still very richly valued @ 48x TTM PE. Let’s how the story plays out.

Disc: Not invested. Watching from the sidelines though.

Management Team

There is no basic customs duty on the import of solar glass. Having said that, there is an anti

dumping duty on imports of solar glass from China, which is at the very least about 10% to 11%.

It goes up to 60% for different manufacturers. There is an import or there’s a countervailing duty

on import of solar glass from Malaysia, which is just under 10% at about 9.71%. There is no import

duty on import of solar glass from Vietnam.

Similar decision was taken in US few weeks back, akin to Borosil there was only one major local manufacturer there as well

Management has been vocal about this risk, played out as well. In any case Vietnam was playing the role that china can play as well.

It won’t be surprising if Management puts expansion plans on hold/ revists, given the uncertainties around erstwhile handsome returns and viability etc. In absence of protective duties.

Govt has likely seen protecting local glass as a limitation/choke point for sclaing overall solar ambitions.

Questions we need to ask is in absence of pricing power and protective sheild, energy challenges- how would the business model gets impacted.

Coincidentally 200 EMA suppprt is broken as well.

Disc - Exited, have been a good run over last 2 years. Respect Management and their credentials, they may as well surprise market by being competitive having factored this risk - time will tell.

I think expansion will not be put on hold because management had said that when new capacities come up they costs lesser ,as brownfield expansion and it also leads to better margins as scalability comes into picture. If they need to fight Chinese ,in this commodity game,scale will come into picture.

Few ways to look at the situation but we will only come to know for sure in the coming quarters -

Management has entered the business prior to ADD and has stated earlier that they are cost competitive against Chinese imports and the only difference is coming primarily from incentives given by Chinese government.

Management has guided earlier that is not such an easy product to master and that even internationally they have a superior product, also it took BoroRenew a few years to achieve production efficiency. Given the current changes it is possible that other domestic manufacturers that are coming up with capacities now will suffer more that BoroRenew.

They have stated that duty ranges from 10% to 60%, this is a huge range and suggests that they might be some imports that can be sold at half the price? If that is true then definitely this is doom and gloom situation for company.

Even currently the company is competing in export market possible against Chinese imports, they are holding their ground there, how?

Cost of freight is still exceedingly high globally, could this help mitigate the difference in production costs?

In hindsight it seems to have been a very weak investment on all our parts if the entire thesis was based on ADD continuing. I will wait for the management commentary and see what is happening. If anyone has any scuttlebutt opportunities to find out glass prices from module manufacturers and how this might impact the industry would be very useful info!

Disc - Invested and have been adding, but will hold further decision till situation is clearer…

Removal of ADD would impact prices max by 10-11% as most of the Chinese imports were coming from Chinse solar glass supplier having lowest ADD per recent concall except below

I guess Malaysian and Vietnamese imports would reduce and Chinese imports would go up due to removal of ADD on Chinese solar glass suppliers (No need to supply from Vietnam since chinese parent company can supply directly). But some module manufacturers have to buy solar glass from Borosil to take care of domestic content requirement.

Going forward, considering this as well as benefits of economies of scale post SG3 commissioning, I expect EBITDA margins around 28% and FY 23 EPS flat as compared to FY 22, even though much higher sales (due to additional capacity)

Discl : Reduced my exposure substantially post Friday’s announcement

With the ADD gone the company will find it very difficult to compete.

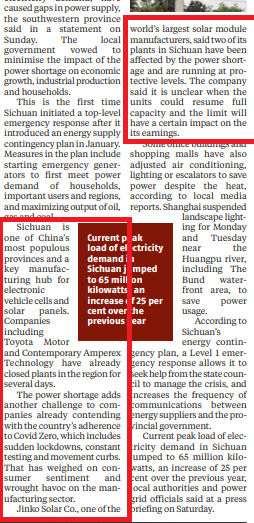

Management said that the chinese manufacturers get gas and elec at subsidised rates. Xinyi has announced a massive expansion of 16*1000 tpd lines from the current 11800tpd. The way I see it is that the Borosil has been in solar glass manufacturing for a long time but they didnt make money till govt. took protectionist steps. Now the direction is clear from the govt that they are looking at the larger picture and will not bother much about something that contributes 5-10% in the total value chain. The timing is especially bad for the company all raw materials are going up, shipping worries are easing. I dont think the company will be able to maintain the margins it saw in Q1 (which already is quite low).

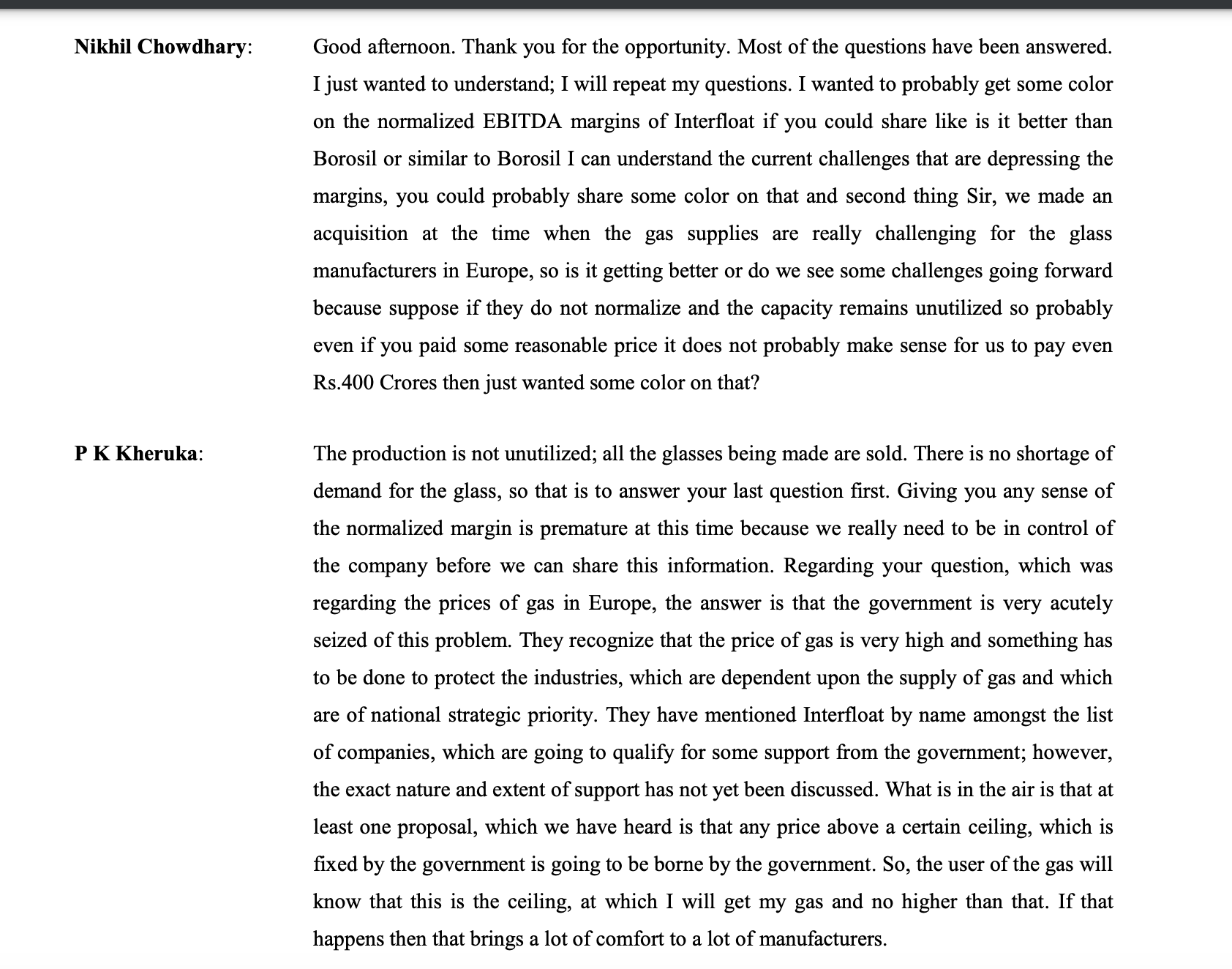

To the last question in the interview on interfloat, when i asked similar question in Q4 when situation was similar, europe was likely to see recession, gas prices were rising, Mr. Kheruka’s reply was different.

Yes agreed the management was very bullish on the acquisition prior to ADD being withdrawn, now suddenly they are backtracking claiming it is due to recession fears in europe but I feel it is more likely that the EBIDTA margin crunch will result in reduced cashflows to finance both internal expansions and acquisitions. Also the deal was meant to be part equity and if Q2 numbers are weak the stock might crash making any find raise activity via QIP or Preferential issue much harder…

The ADD of ~10% is no longer going to be applicable on China, so Chinese glass will be 10% cheaper. PK has consistently said that China determines the price and BR follows, so some amount of price depreciation is obvious. This will also have an impact on margins and realisations.

However, the impact may not be massive because a) a 10% reduction while negative is not the disaster that it may have been and b) BR was anyway competing with non ADD glass from Vietnam.

The above is assuming BCD of 10% is not imposed, we’ll have to wait till March 23 to understand the govts intentions. If it is, we’re back to where we were, if it’s not some margin erosion is absolutely necessary. How much of this will be offset by the increase in revenue is really the million dollar question.

In the interview he said that our plant has been depreciated out so out cost is low… something of that effect.

What kind of logic is that? his plant of 450tpd might be depreciated, what about the 550tpd thats coming on stream in october and 1100tpd yet to be announced? the stock trades such premium valuation and they are talking about the depreciation advantage is really absurd. On one hand he keeps saying that Chinese producers have various subsidies and we cant compete without import restrictions and when the duty is removed/not renewed he’s talking about advantages of his legacy plant.

In the end the valuations are depended on the margin profile of the business. Company has been counting on fund raise to set up 1100tpd plant. with margins under pressure the valuations will compress in the future. I don’t know how will the company fund its next leg of expansion. Now they are saying that the German acquisition is also on hold. This is not a very high asset turn business to begin with and because of that fact the margin profile of the company becomes very very crucial. I’d have been happier if the company tried to give a margin impact range instead of talking about march 2023.

Company has been trying to raise funds for the next leg of capex for a long time but they did not get much interest. Now lets see what they do with the 1100tpd capex.