The disclosure regarding the acquisition came through on Monday morning. The stock was up ~ 14% on Friday. This seems extremely suspicious, and doesn’t lend to a professional, clean company. Does anyone else share these concerns?

Thanks, this is very helpful. Takes care of insider trading concerns, though it’s still curious how the agenda was for issuance of equity and the resolution passed is for an acquisition.

Not a concern regarding governance, but a curious development.

When the indian markets offers so good potential and organically the growth is very robut, they shouldn’t have looked overseas at the moment.

The Multiple paid Sales of target looks cheap, need to see if it is profitable.

Since european market can have some issues surrounding gas supplies, the existing facilities may not be utilized to the maximum. If they ultimately end up supplying from India like others do, they would have been better by strengthening their Sales team by making some good hires from the european market and growing the customer base organically.

Just some high level thoughts till more details come when management holds the concall.

Agree. This would be a high-cost location (labor & energy costs), right next to Russia’s border. Yes, will provide greater access to clients in Europe, but would love to hear from management on how exactly they plan to leverage it.

From quick overview, it seems interfloat and GMB are connected at the hip ie. GMB is manufacturing arm of Interfloat and Interfloat does all engineering, R&D ,business development and sales for GMB produced glass.

Money to be paid as per the moneycontrol news above is 25M Euro for GMB and 5M Euro for Interfloat in addition to 22.5M Euro worth of Boro Renew shares ( not considering performance bonuses for next 3 years). So it comes to around 52.5M Euros (440Cr with current exchange rate). Since GMB would be exclusively selling to Interfloat, we need to consider Interfloat sales only which is 59M Euros (490Cr).

In nutshell, Boro Renew purchased 300TPD solar glass company in Germany having sales of 59M Euros by paying around 53M Euros. Knowing how conservative Kheruka’s are, I guess it must be a good bargain for them to consider it.

They have been careful in articulating efficiency improvements for acquired entity - wouldn’t be surprising if they are making much lower profit margins/ even could be insignificant. Also supported by various duties on Chinese imports. Market reaction seems on similar lines. Valuations also reflect low profitability.

Mr Khureka is more than capable of turning around performance, but will need time. India biz will always look better margin profile ( new machines, low labour cost, operating leverage of scale) and there will be diverse views on participants as to why acquisition when local mkt is v high margins.

Postive side - Truly Global footprint and reach, geo de risk, and again local non Chinese supply major player situation in EU. As long as local duties support, they can do well.

450 TPD to near 2600+ TPD - that’s a 6X growth in 5 years., big question will be margins trajectory in this journey. One good part is In overall scheme of things EU is still small % of overall capacity.

With prolonged lockdown disruptions in China, glass supply to remain challenging, augers well in near term for both India numbers and acquired biz. However consol numbers modeling will need a rebook.

Healthy for long term, short term may have its own challenges.

Invested - minor profit booking in pre acquisition news run up

As per my limited understanding, the moment BRL starts supplying its European customers through Interfloat, the amount of glass exported would reduce and the same can be used to cater for local demand in India.

It would be a win win situation for BRL as they de risk themselves from a single manufacturing location risk and also from any kind of ban like the Chinese are facing in Europe.

Also the major advantage would be the savings on transportation cost which is huge these days.

Fair point, ain’t denying but presently the issues around europe’s resource availability (gas is one of the main RM for Glass) are more prominent (which is highlighted even in the press release and highlighted in my point above).

If acquiring facility remains underutilized even if available cheap, no pointing risking a 400 crore towards it.

i will wait for more clarity on the operating metrics of the target too. Looks it will dilute the OPMs too (entity has 300 Employees similar number of per TPD basis like borosil and has similar sales per TPD as borosil, means targets OPM looks to be lower considering Europe has higher wage bill, correct me if i am wrong).

6x in 3 years. Not accounting for op lev and assuming current efficiency levels, 3 yr fwd PE of ~10-12.

On lower profitability from the 500 TPD german plant (~20%) of targetted 2600 TPD - should be still value accretive for the investors since ROCE more or less remains intact at group level - since they are spending less to buy the capacity

I’m still figuring out how GMB makes money? would it be double counting if we add both company’s revenue?

At consol level how much revenue do you think would BRL be making at current capacities after incorporating both subsidiaries? Domestic units make roughly 500-550 crs from 450TPD capacity.

GMB may be selling to Interfloat on cost plus basis and then Interfloat’s selling price would be based on market prices. So GMB sales would be intercompany sales to Interfloat and hence would get eliminated in consolidation. So for all practical purposes, we have to take Interfloat’s sales (to external customers) which is 59M Euros, which would be around 490 Cr for 300TPD capacity.

What BRL would add value would be improving margins (and maybe productivity) of that plant. So post acquisition, I don’t expect much change in sales of Interfloat but its margin profile can improve.

Thanks for the clarity.

Another very interesting thing to note is tax rate in Germany is just 15%!

So ebitda margins might not reflect the true profitability of the company.

EBIDTA stands for earnings before interest, taxes, depreciation, and amortization. So, it is before taxes, so the tax rate does not come into the picture. It is used precisely for this reason that one can understand the true operating nature of the business without getting bogged down into the financial management details.

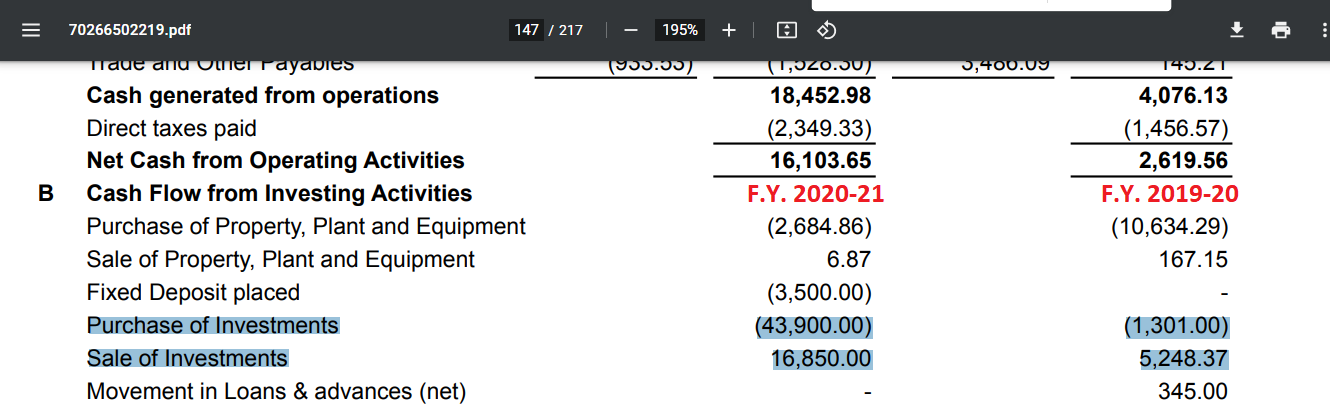

In F.Y. 2020-21, as per cash flow from investing activities, company purchased investments worth Rs.439 crs. Company got around 200 cr from QIP. Now i am unable to tally source of the balance 239 crs. Net CFO was around Rs. 161 Crs. Also borrowings reduced. Then from where the funds came?

Company did not mention anywhere about the sale of investments woth Rs. 168 Crs. What were those investments?

FY 22 Solar glass prices - Rs 133 /mm/Sq mt as compared to 112 /mm/sq m fro FY 21 - 12% jump for the year

Recd 9.7 Cr from Gujarat govt subsidy

extra modules ordered by solar guys in Q4 FY22 to avoid BCD from 1st April 22

Actual production - 443 Tonnes/day - against capacity of 450 T/day

European acquisition - 425 Cr acquisition cost + performance based bonus (525 Cr sales)

Margin at GMB - not shared. But it was very good. Margins reduced due to input cost increases. Wait for 2-3 months for transaction to complete then will share details.

Capacity utilization - 100%.

Gas requirement - no spot buying. 1/3rd under APM

20GW annual addition in Europe. Local solar module production is less than 3GW.

In Germany, localization - Local accelerator program - local module production can grow to 8-10GW modules - so will increase solar glass demand

Solar glass price - Q4 realization lower by 14% as compared Q4 FY21. Solar glass price Rs 134/mm/Sq m Solar glass prices started to go up. Up by 14-15% already

Europe has anti dumping duty 55-60% on Chinese goods. Local prices are fairly high

Direct exports are 20%, SEZ exports 7%. Will continue post expansion

European acquisition - Sellers are financial investors. So they were looking at Capex reqmt, impressed with Boro Renew’s numbers and skill sets and experience

First they wanted to sell 85% and then decided to sell 100%, visited Boro Renew plant, indian market very fast growing so they got stakes in Boro Renew

Funding of acquisition - Will take loan in target company, subsidy from german state and internal accrual

mix of debt and equity for SG4 financing

Cost of operation in Europe - inputs are internationally benchmarked. Manpower and Gas cost is very high. Local production so prices are higher

Interfloat Market share - 2/3rd of Europe. 1/3rd requirement is imported into Europe

650 Cr for 550 TPD

27% thinner glass (2, 2.5 and 2.8mm) - higher margin sales

Europe - Big guys don’t look at landed cost. They favor local suppliers even at higher price. More on higher quality and consistent supply

No competition for buying interfloat. It was mutual discussion

Prices of gas in Europe are high. Govt is working hard. Interfloat will get supported by Govt as strategically important company

Germany is thinking of a support scheme where any gas price above ceiling will be paid by govt

New furnace SG3 is getting delayed to Sept from July

Adani solar glass plant will start production from early next year. Reliance would have solar glass plant for captive consumption.

Triveni and Gold plus, Saint Gobain are looking to start solar glass mfg.

Total Debt - 50 Cr - SG2 and 200Cr - SG3